Directors, board members, and large shareholders are just some of those who might have non-public material information about their firm. Even though this information could be easily used to profit by trading their own stocks (stocks of the company they hold information about), this behavior is strictly prohibited. This is but one aspect of insider trading.

There are two different possible understandings of the term insider trading. Illegal and legal. Illegal is the one just described – when non-public, material information is used to gain an unfair advantage on the market. Such trading is strictly prohibited and is punishable by both fines and jail time. On the other hand, despite its negative connotation, insider trading does not have to be only illegal. After all, company insiders have the right to trade their company’s stocks too. However, to avoid the aforementioned unfairness in regard to the market, such trading is regulated. The U.S Securities and Exchange Commission has set rules, which mainly include filling out appropriate forms within a given time period to publicly disclose such trades.

Both academic researchers and ‘outsider’ traders often take interest in these form fillings. There exist multiple trading strategies utilizing this information and other aspects of insider trading into a profitable market strategy. These include things like trying to identify good or bad market news based on the insiders’ disclosed trades, for example. Thanks to the SEC regulation of the market, the number of illegal insider trades surely has decreased. By how much, however, is a different question. Neither can we know, how profitable these illegal insider trades are, as successfully identified is only an uncertain part of them.

So Mathijs Cosemans and Rik Frehen in their study “How harmful is insider trading for outsiders? Evidence from the eighteenth century” from January 2022 take up a novel approach to this problem. They study insider trading in the time when it wasn’t regulated at all – in the early 1700s. Their 300 hundred-year-old dataset consists of data recovered from original handwritten ledger books and transfer files of the 3 largest companies in the London stock market at the time. Then they study the trading activities of the insiders and groups including potential insiders to identify if there is present any overperformance relative to the market.

Let’s first, however, consider how did the London stock market look at the time. Most of the trades were decided in the coffee houses near the Exchange. If someone wanted to sell or buy a stock, they had to find a broker, who would fix the price for you and execute the transaction. This had to be recorded in the company’s ledger and transfer books, which were located in the transaction offices – another possible place to meet the other traders. If one, for whatever reasons – maybe living far from the Exchange, or maybe being an insider who wanted to keep his identity concealed – didn’t want to do the transactions in person, they could mandate someone to execute their transactions for them.

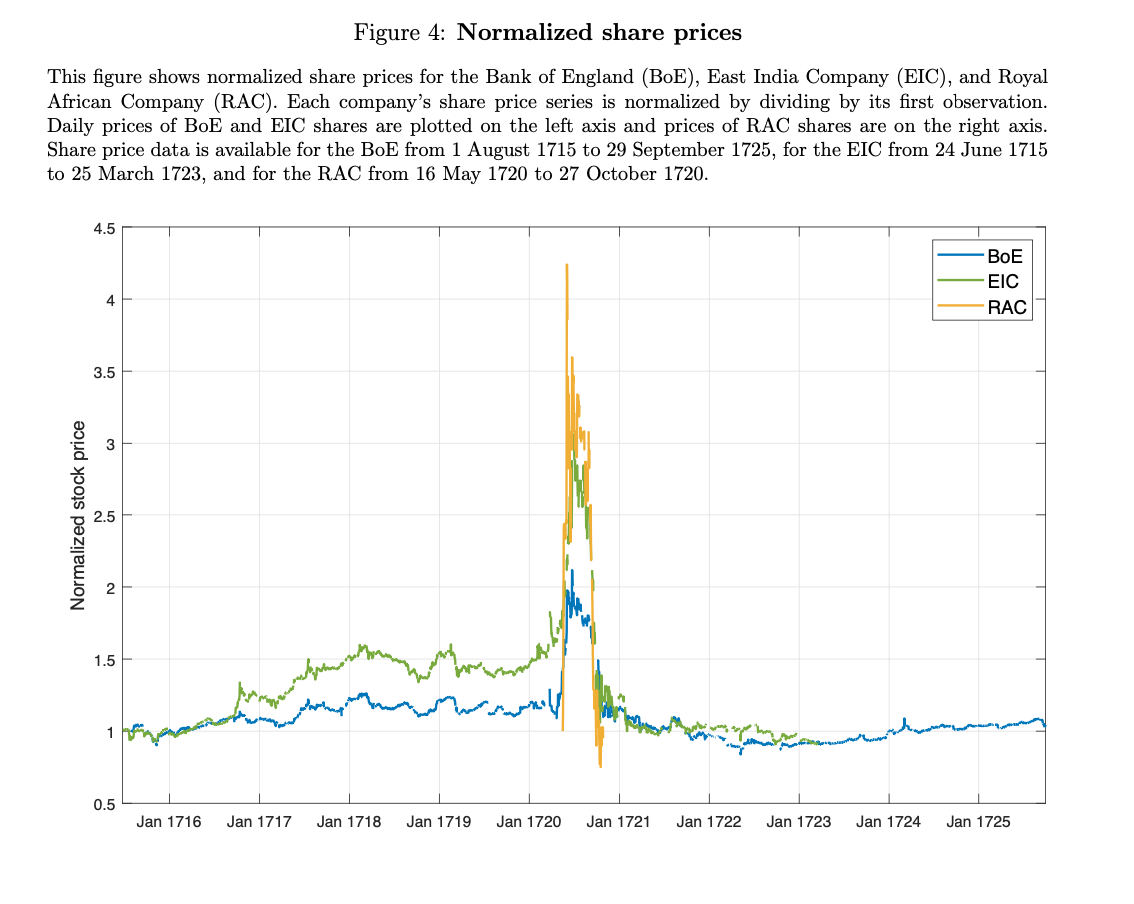

Regarding the market, at the time there were 3 major companies, whose samples the authors consider. Those were the Bank of England, the East Asia Company, and the Royal African company. Their share prices were announced daily in the newspaper. The time period of the sample starts in 1715 and lasts 10 and 8 years respectively, and unfortunately, the ledger books of Royal African Company weren’t preserved, so there’s only half a year of data (from the year 1720) available, which has been reconstructed from the transfer files. This means the sample period is in all 3 cases influenced by what is known as the South Sea bubble.

The South Sea bubble is named by a company with the same name, the South Sea Company. It was founded in 1711 and two years later it received the exclusive right to transport slaves to plantations in South America. This monopoly, however, didn’t have much to do with the cause of the bubble, which first extremely inflated the prices of the whole market, and then burst around the year 1720 leaving many investors ruined. What the company did, was purchasing illiquid government annuities from investors, and in turn selling the more liquid South Sea shares in their place. They had a closed deal with the government to do that for a fixed fee, and the government allowed them to issue new shares in exchange. The South Sea share price quickly rose, actually so much as from £100 to £1000 within a single year. This caused crowd purchasing of the stocks, of the South Sea and also of all the other companies, until the bubble burst shortly after and many lost their life savings in the process.

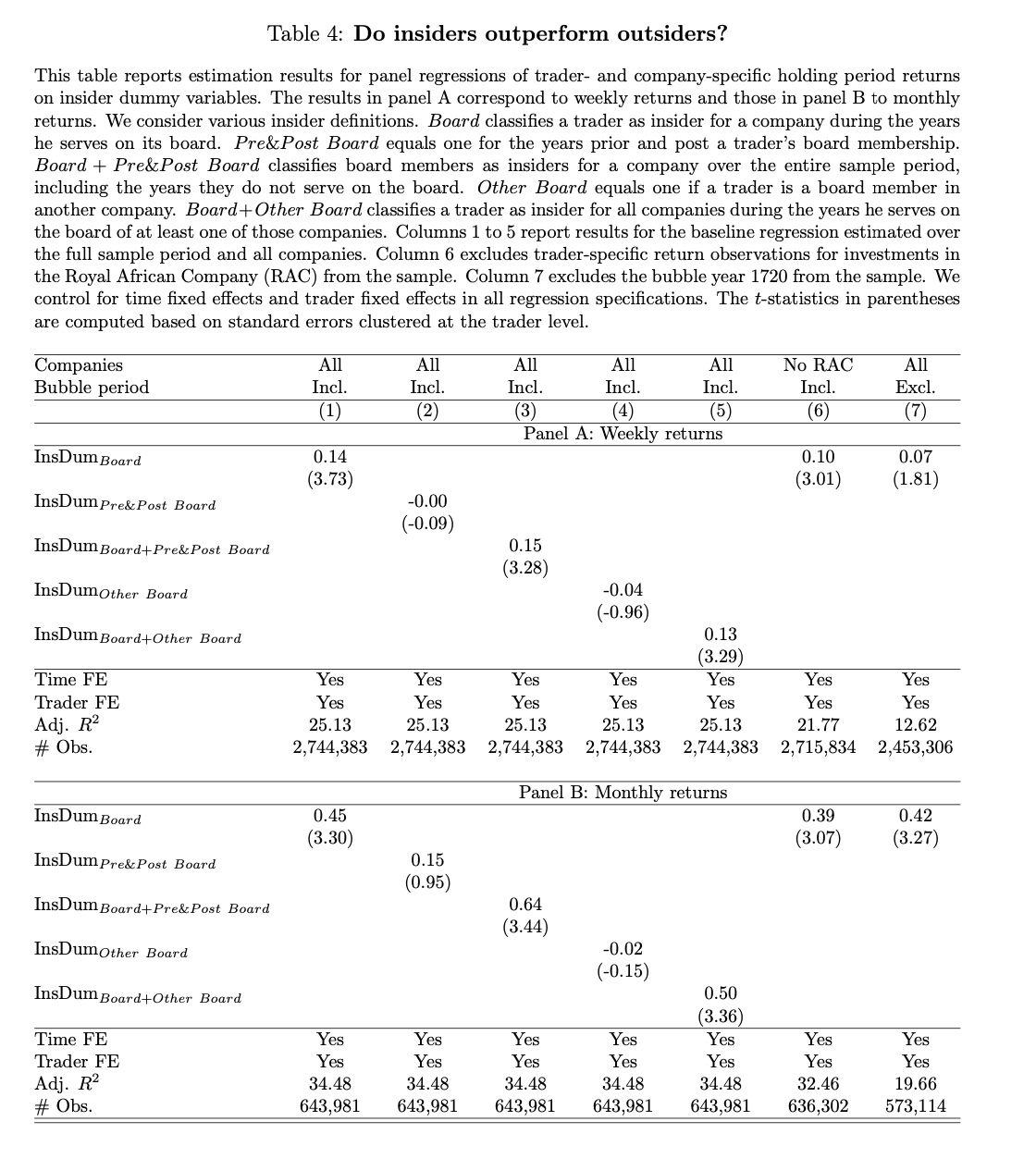

Let’s now take a look at the new findings of the study. The sample consisted of over 14 000 outsiders and only 123 insiders. This means that encountering and trading with a company’s insider wasn’t very likely – the unconditional probability of such trade according to the paper was only 2%. The predictive power of the insider trades is only present in years they are part of the board, and in the company in which they hold a position. The authors calculated their outperformance to 7% per year. Due to the large difference in the number of insiders and outsiders (even if considering direct insiders plus their friends/neighbors/politicians) the losses caused to the outsiders are almost minimal. The authors propose, that the calculated loss for the outsider after trading with an insider (5bps per 1 transaction over one-month period of the trade) could be regarded as the upper bound for such loss in the modern markets, since nowadays is insider trading strictly regulated, the number of outsiders is much larger, while the number of insiders didn’t change drastically.

To conclude, insider trading is a phenomenon tied with stock trading from the very beginning of the markets. While nowadays it’s well regulated by SEC, which tries to keep the fair market for everyone, there was a time when there were no rules. In this study, the authors Mathijs Cosemans and Rik Frehen take a look at how did the market look at the beginning of the 18th century. You can take a look at some interesting figures from their research below.

Authors: Mathijs Cosemans and Rik Frehen

Title: How harmful is insider trading for outsiders? Evidence from the eighteenth century

Link: https://ssrn.com/abstract=3902504

Abstract: This paper provides evidence on the financial consequences of insider trading for outsiders. We collect a novel data set that contains all equity trades of all corporate insiders and outsiders in an era without restrictions on informed trading. These data features allow us to study the profitability of insider trades and the expected loss outsiders incur due to insider trading. We show that access to private information creates a performance gap of 7% per year between insiders and outsiders. Nonetheless, outsiders’ unconditional expected losses from insider trading are small because the probability of trading with an insider is low.

As always we present some interesting figures:

Notable quotations from the academic research paper:

“First, because there are no restrictions on insider trading during our sample period, we can measure the price informativeness of insiders’ trades in an unregulated setting. Second, because we observe the identity of each trader and the exact timing of their buy and sell transactions in each stock, we can measure trader performance accurately and quantify the return gap between insiders and outsiders. Prior studies only observe a non-random subset of each insider’s trades (i.e., detected illegal trades or self-reported trades) and cannot compare the performance of insiders to that of outsiders because they do not observe outsiders’ trades and realized returns. Third, because we observe all transactions of all insiders and outsiders, we can measure the unconditional probability that an outsider trades with an insider and the expected loss for outsiders due to insider trading.

Consistent with prior work, we find that insider trading activity has strong predictive power for future stock returns, both at a one-week and one-month horizon.

We find that directors’ predictive power vanishes when they no longer serve on the board. In addition, their trades do not predict returns on other companies. This evidence suggests that board membership improves a trader’s access to valuable private information.

We analyze if insiders outperform outsiders by exploiting their private information. We account for trader fixed effects to rule out that any return differences between insiders and outsiders are driven by unobserved trader characteristics such as IQ, education, and investment skill. We find that due to their superior timing ability, insiders outperform outsiders by 7% per year on average when investing in the company on whose board they sit.

In fact, 90% of outsiders never trade with an insider during our sample period and 5% encounter an insider only once. The unconditional probability of an outsider selling (buying) stocks to (from) an insider is 1.72% (1.53%) per trade.

The three companies for which we were able to collect all share transactions, i.e., the Bank of England, East India Company, and Royal African Company, collectively represented more than 40% of the market in terms of pre-bubble capitalization (see Anderson (1801)).

In the early 18th century, the British government had a large amount of high-interest rate debt outstanding.A substantial part of the debt was in the form of annuities that were tied to the life expectancy of the annuity holder and therefore hardly tradeable. Due to this market illiquidity and the poor financial condition of the state, the annuities were unattractive for debt holders and traded against sharp discounts. The government itself also disliked the annuities because they offered few opportunities to redeem debt or defer interest and principal payments.

The South Sea Company came to the rescue by offering annuity holders the option to convert their illiquid annuities into liquid South Sea shares. The Company paid the government a fixed fee and received in return the interest payments on the annuities and the right to issue a fixed number of new South Sea shares to investors.10 The government gained because it paid a lower interest rate to the Company and got the opportunity to defer payments. The profitability of the deal for the South Sea Company relied on both legs of the deal: (i) between the Company and the government; and (ii) between the Company and the annuity holders.

The main advantages of the ledger and transfer file data are their completeness and high level of detail. We observe all daily holdings and buy and sell transactions for every shareholder of a company.

We find that many traders live close to the stock exchange: in Westminster, St. James’, Holborn, or the city of London. Among the foreign traders, the Dutch and Swiss are the largest groups with 810 traders from Holland and 145 from Switzerland. The table further shows that merchant, draper, and goldsmith are the most popular occupations among shareholders. Temin and Voth (2004) point out that goldsmiths often acted as early 18th century bankers.

Approximately 2% of the traders carry a title, most commonly Baron(et), Knight, and Earl, but higher nobility is also active in the London stock market (Dukes, Viscounts, and Marquises).

Table 1 further shows that the total number of trades over the sample period is 54,140 for outsiders and 3,350 for insiders. For days with positive trading volume, the average total trans- action volume per day is £34,540 for the group of outsiders and £5,373 for the group of insiders. Interestingly, average holdings per trader are much larger for insiders (£13,381) than for outsiders (£2,639), which indicates that insiders tend to hold larger portfolios than outsiders.

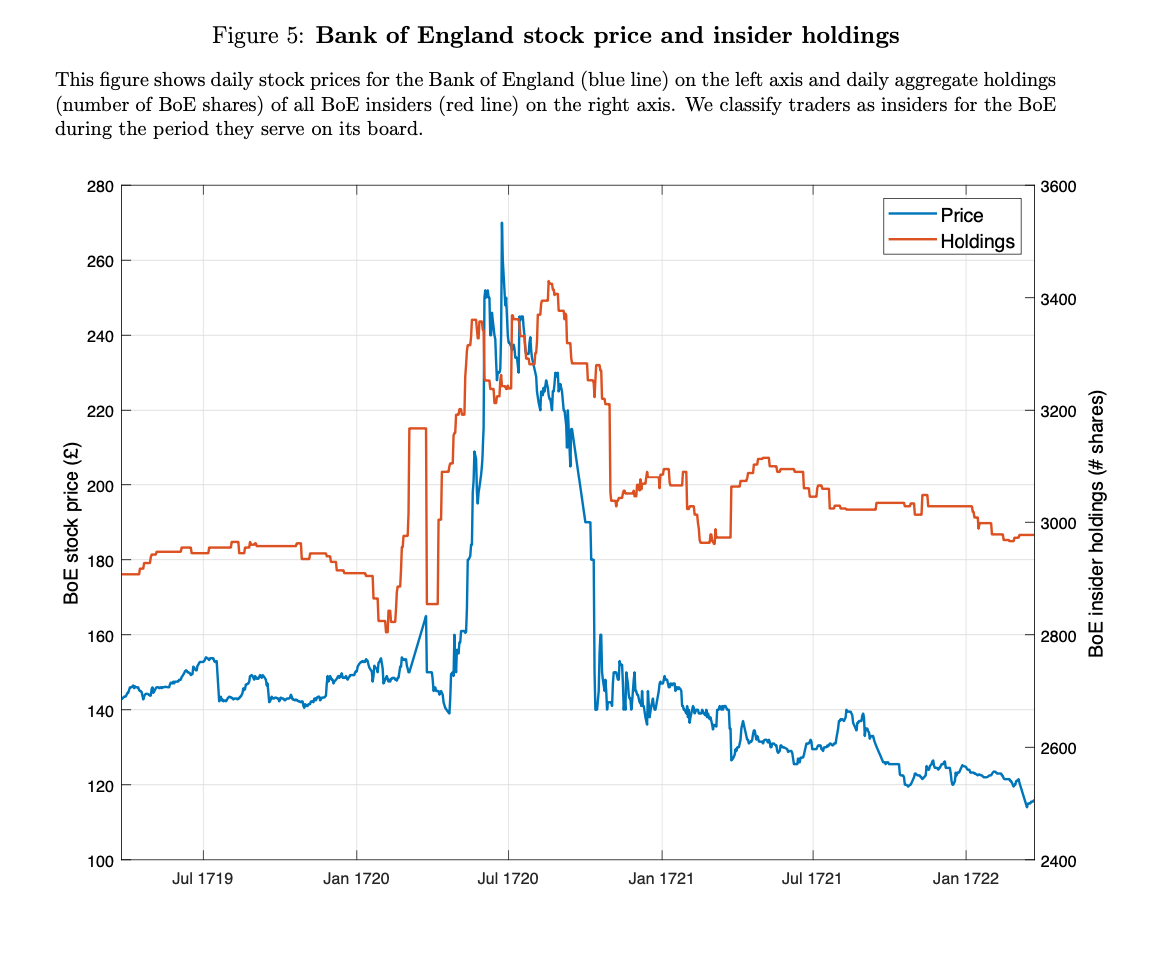

We observe that net trading activity by insiders significantly increases in the month prior to the launch of the loan facility. In contrast, net trading activity of outsiders significantly decreases in that month.

In particular, we observe 28 insider purchases in April 1720, compared to an average of 3.4 buy trades in other months. Insiders purchase a total of 347.5 shares, up from an average of 47.5 in other months. The number of BoE insiders buying Bank shares increases from an average of 2.6 in normal times to 13 in April 1720 (i.e., half of the board).

Temin and Voth (2004, p. 1657) argue that trading in forward markets was also not very prevalent in the early 18th century London financial market. They note that “transfers in England were normally neither particularly time-consuming nor costly; consequently, most trading took place in the spot maket, not in the form of forward contracts.” Moreover, traders in forward contracts were also exposed to counter party credit risk, which limited forward trading to a small group of traders and further reduced market liquidity.

We argue that the expected losses that we report based on historical data serve as an upper bound on the expected losses outsiders face due to insider trading in modern stock markets.

Although our evidence shows that outsiders’ expected losses due to insider trading are small, we do not claim that informed insider trading is innocuous and does not need to be regulated. For instance, illegal insider trading can be harmful for companies and investors by reducing market liquidity and by undermining investors’ confidence in the fairness of financial markets.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend