What Is an Optimal Allocation to Cryptocurrencies?

Cryptocurrencies are a very controversial asset class. Some people may hate it, others may glorify it, and a significant part may ignore it. But what’s the opportunity cost of complete ignorance? Are we able to numerically calculate it? That’s a hard question that Duchin, Solomon, Tu, and Wang tried to answer in their recent paper, and we will take a look at some of their findings and discuss it.

—

Cryptocurrencies are unique in that they have no underlying cashflows and no prospect of them, which seems not to be resolved by many standard modeling tools used by a significant part of the asset pricing models. Models of behavioral finance are a bit better in case of understanding this since the human psyche is, in some situations, predictable. Seeing the absolute returns of some of the cryptocurrencies (even the most prevalent Bitcoin) raises the question of whether investors should consider investing in them and what size of the portfolio they should allocate to them. Fundamentalists are strict: these assets make no sense, and so only naive or confused investors purchase them. But what if we are a little more flexible?

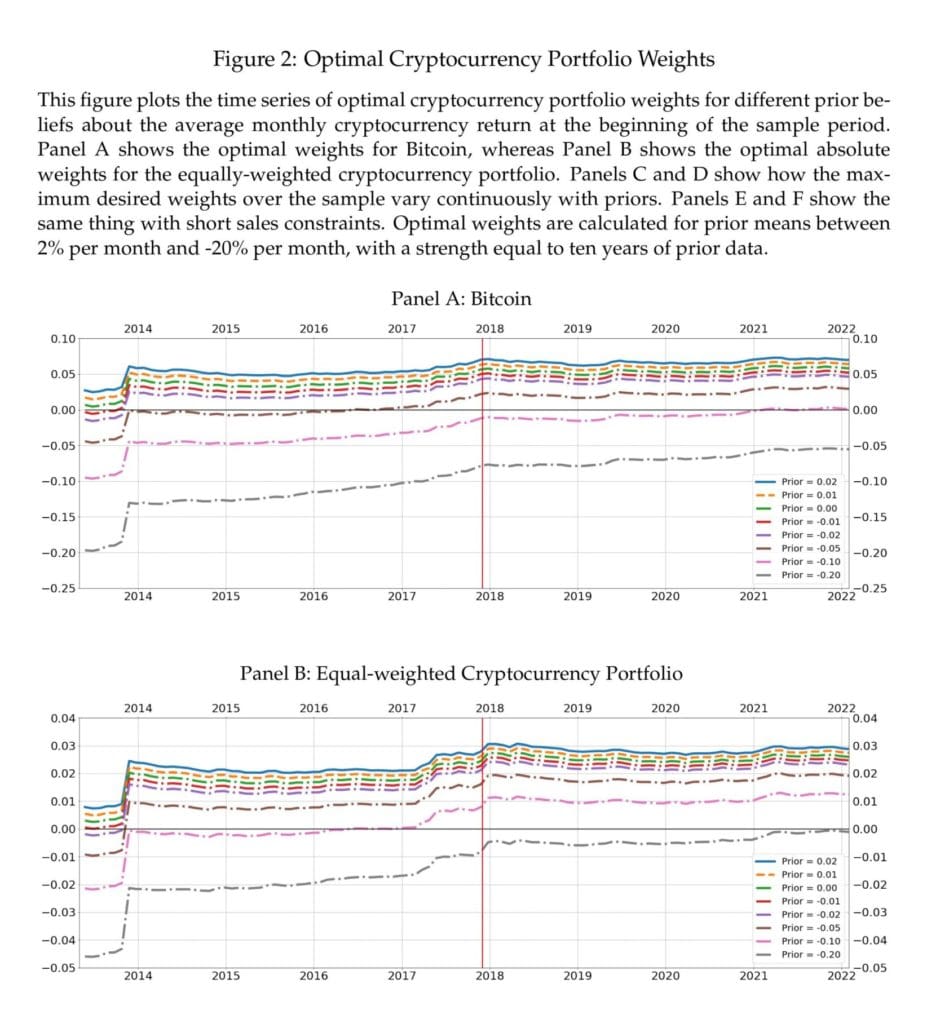

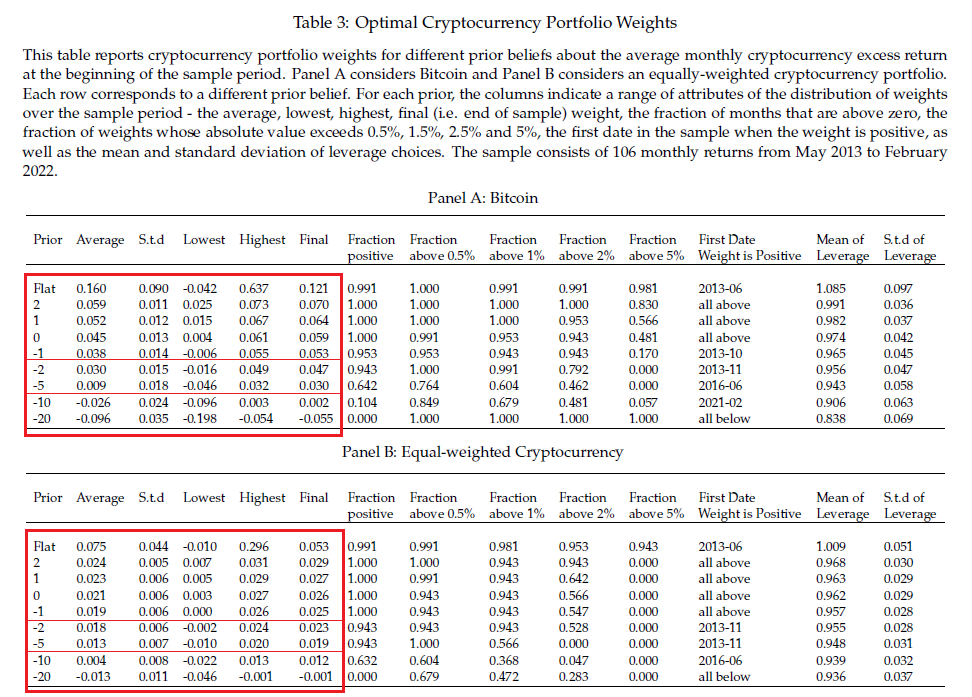

The philosophical approach of Bayesian Portfolio Theory in a novel paper by Duchin, Solomon, Tu, and Wang (December 2022) discusses the place (position) and size of cryptocurrencies (long, zero [flat], short) in traditional portfolios based on prior and changing beliefs. The papers’ main point revolves around the main problem of allocation weights that are consistent with one’s belief in accordance with BPT. The authors use rich historical and actual data from 2013 to 2022. Figure 2 shows that despite cryptocurrencies volatility, optimal weights changed relatively smoothly for all the priors (expressions of investor’s belief before some evidence is taken into account). The result is that while cryptocurrency monthly returns are volatile, posteriors (beliefs updated after the event via Bayes’ rule) about means change relatively slowly once an informative prior is imposed, even more so additional data has been observed. As long as the volatility of returns is reasonably stable (and understood), the optimal actions of investors do not change rapidly.

Column 2 in Table 3 analyzes what should be the average optimal weight of cryptocurrencies in the portfolio. We can see that even for pessimistic prior beliefs (-2% or -5% monthly returns), the optimal weight in Bitcoin is positive (Panel A, rows 6 & 7, 3.0% or 0.9% weights). The same is true for cryptocurrencies in general (Panel B, rows 6 & 7, 1.8% or 1.3% weights). The reason for the non-zero optimal investment in cryptocurrencies is that cryptocurrencies tend to surprise on the upside and outperform even when we have significantly negative prior beliefs (as can be seen in the columns 7-11, which shows the fractions of the time that cryptocurrencies outperform certain threshold).

Both cryptocurrency boosters and skeptics tend to agree on the asset’s high volatility, and second moments are generally easier to estimate than first moments. Being correctly calibrated on cryptocurrency volatility (as investors are here) prevents investors from “blowing themselves up”. The high volatility of cryptocurrency is a strong reason only to take small positions, but this is not the same as taking zero positions. Even if one believes that cryptos have inherent zero value, it does not mean that they would collapse overnight. Very pessimistic priors can justify a zero allocation to cryptocurrencies, but once we set our beliefs more realistically, we can reconsider optimal allocation even for the such a risky asset class.

Authors: Ran Duchin, David H. Solomon, Jun Tu, Xi Wang

Title: The Cryptocurrency Participation Puzzle

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4258515

Abstract:

We show that ongoing zero portfolio weights in cryptocurrency are surprisingly difficult to generate in a standard Bayesian portfolio theory framework. With ten years of prior data, equity market investors would need very pessimistic priors on mean returns to justify never having bought cryptocurrency: -10.6% per month for Bitcoin, and -19.6% per month for a diversified portfolio of cryptocurrencies. Moreover, most priors that involve never purchasing cryptocurrency imply that investors should short cryptocurrency. Optimal absolute weights are generally small but non-trivial (1-5%), frequently positive, and fairly smooth despite returns being volatile. Under a wide range of priors, the certainty equivalent gains from cryptocurrency are comparable to international diversification and exceed the size anomaly. Costs (ambiguity aversion, storage, fees) would need to be enormous to justify never trading, over 21% per year for Bitcoin and 39% for a diversified cryptocurrency portfolio.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

Notable quotations from the academic research paper:“The view that cryptocurrencies are worthless because they cannot produce cash flows is based on venerable discounted cash flow models. But even if one believes that cryptocurrencies ought to be priced at zero, this does not necessarily mean they will end up there. The positive aspect of discounted cash flow models can be represented as priors about the distribution of expected returns. In this framework, saying that Bitcoin is a scam or a bubble implies that it has negative expected returns over some future horizon, which we dub “pessimistic priors”. While these priors may be based on compelling economic logic, they are amenable to quantification and updating via Bayes’ rule.

Our main finding is that an allocation of precisely zero to cryptocurrencies, year after year, is hard to generate by most pessimistic Bayesian priors. One can either believe that cryptocurrency is a bubble with large negative expected returns, or have zero portfolio allocation to cryptocurrency every period, but it is surprisingly difficult to do both. And while there are good reasons to avoid a large allocation to cryptocurrency, it is much more difficult to justify avoiding small positive or negative portfolio weights.

In our baseline specifications, we focus on the effect of different prior beliefs about mean cryptocurrency returns, and assume that investors are approximately well-calibrated about volatility and correlations. To capture investors’ level of certainty in these priors, we assume that they have observed ten equivalent years of data before the series began. We assume that investors initially hold the US market portfolio, and choose an optimal portfolio that combines positions in cryptocurrency, subject to reasonable levels of risk aversion. In subsequent analyses, we consider different beliefs about volatility and correlations, different levels of certainty about prior beliefs, and alternative initial portfolios. We find that investors’ prior beliefs about mean Bitcoin returns would need to be lower than -10.3% per month to justify non-investment at the end of the sample period (February 2022), and lower than -10.6% to justify never investing during the sample period. For the equally-weighted cryptocurrency portfolio, the results are even more extreme: priors would need to be lower than -19.2% for end-of-sample non-investment, and -19.6% for never investing. These estimates, however, understate the puzzle since large negative priors generally imply negative portfolio weights.

We also investigate investors’ ex-post satisfaction with their cryptocurrency investments in two ways. First, were they happy with the ex-post realized return distribution of their chosen portfolio? Second, would they have continued to invest in cryptocurrency? These are separate questions one could continue with a trade (thinking it will produce good returns) despite being unhappy with the returns so far. Unsurprisingly, a wide range of optimistic priors lead to ex-post happiness, although at extreme levels of optimism (above 25.1% mean excess returns), investors are ex-post unhappy due to the large volatility that their beliefs expose them to. More strikingly, even initially pessimistic priors above -3.4% eventually lead to long positions and ex-post happiness, whereas more pessimistic priors lead to ex-post unhappiness. These results confirm the common intuition that acting on highly pessimistic beliefs was ex-post unsatisfactory.

We assume that the investor starts with the CRSP value-weighted market portfolio as his risky asset. This captures someone following the frequently-dispensed advice to hold diversified equity index funds. We consider three cryptocurrency portfolios: Bitcoin-only, as well as equal-weighted and value-weighted portfolios of coins (with a prior market capitalization greater than $100m). For the strength of beliefs, we assume that an investor updates as if he observed ten years of monthly data with the parameters in question, and adds each new month’s returns to work out the posterior values. We assume beliefs about variance that roughly correspond to ex-post sample outcomes, with Bitcoin having a variance 150 times the market (ex-post was 143), the value-weighted cryptocurrency portfolio having a variance 170 times the market (ex-post was 166), and the equal-weighted portfolio having a variance 625 times the market (ex-post was 612). Lastly, we assume that the investor believes cryptocurrency to be uncorrelated with the market.

We find that most pessimistic regions ended up ex-post unhappy (i.e. unshaded). Among initial pessimists, only the mildly pessimistic ended up ex-post happy, due to switching to positive weights early in the sample period. All investors who were on average short at the end of the sample period were ex-post unhappy, even those that had switched to long holdings by the end (the yellow bars). Some of the “on average long” priors (green bars) still were ex-post unhappy (unshaded), primarily those who switched to long positions relatively late. Extremely pessimistic investors stayed short the whole time, but ended up even more unhappy ex-post. Finally, the most extremely optimistic priors were ex-post unhappy, but only for enormously optimistic beliefs. Panel B [Figure 5] shows that for the equal-weighted cryptocurrency portfolio, a wider range of priors resulted in investors being long (on average) and ex-post happy by the end of the sample period.

Finally, while our paper has an explicitly normative focus on the actions implied by various beliefs, we do not take a stand over why investors have the priors they do, nor whether such priors are reasonable. Much of the public debate attempts to convince others that their priors are wrong, mostly to little effect. While we seek to avoid debating priors, some readers may have heuristics to not invest without a clear economic theory of the asset. In the Appendix we suggest an economic basis for at least agnosticism about cryptocurrency returns. However, none of our analysis depends on this component, and we assume that everyone is entitled to their priors.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend