When Crypto Stopped Diversifying: The ETF Regime Shift

Can crypto still help diversify an equity portfolio—or has that edge disappeared? That’s the practical question behind Crypto Contagion. The paper looks at how shocks move between crypto and U.S. equities, and more importantly, how that relationship changed after the launch of crypto ETFs. Instead of relying on simple correlations, the authors use a combination of jump detection (to isolate real stress events) and machine learning techniques to identify actual spillovers. By comparing periods before and after ETFs, they effectively show how the market structure—and with it, the behavior of crypto—has shifted .

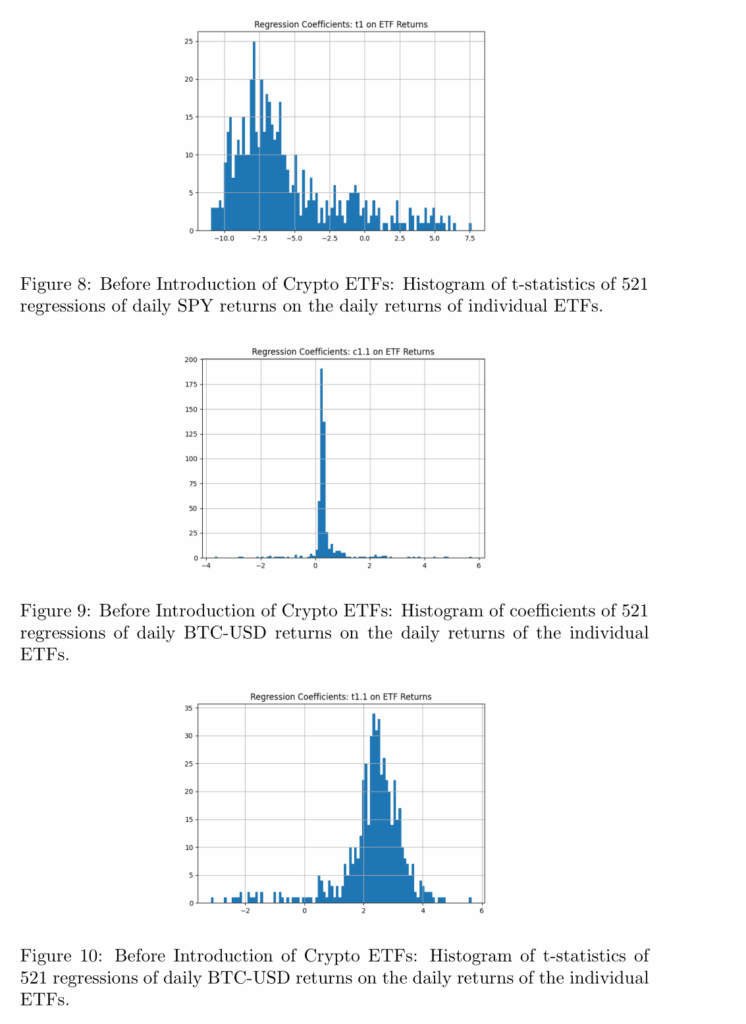

Before ETFs, crypto behaved much more like a standalone asset class. Figures 8–10 highlight that while equity ETFs were tightly linked with each other, Bitcoin’s relationship to them looked different—there was connection, but not true integration. More importantly for portfolio construction, crypto moves tended to offset equity moves. The paper estimates that a 1% move in BTC or ETH corresponded to about a −0.07% move in the S&P 500, which is exactly the kind of behavior you want from a diversifier. In practice, this meant crypto could act as a partial hedge during certain market conditions, especially when crypto-specific factors were driving returns .

After the arrival of crypto ETFs, that story changes. Crypto starts behaving much more like a risk-on asset, moving in the same direction as equities and losing most of its diversification value. At the same time, ETFs become the main channel through which information and flows enter the market. That has an interesting side effect: while correlations go up, the direct “shock transmission” from crypto into equities actually weakens, because ETFs absorb a lot of the rebalancing pressure. For traders and portfolio managers, the implication is straightforward—crypto is no longer a clean diversifier. It should be treated more like a high-beta extension of equities, driven by the same underlying risk sentiment and institutional flows.

Authors: Travis Dyer and Nicholas Guest

Title: Crypto Contagion

Link: https://ssrn.com/abstract=5630550

Abstract:

We propose a risk-sharing model of crypto contagion. Crypto contagion is an economic event in which crypto currency crashes spread across multiple financial instruments or even entire asset classes. Accurate measurement of contagion facilitates prediction and risk management: proactive implementation of measures that can stop contagion once it is triggered.

To measure contagion, we combine jump diffusion with double machine learning. We document significant, yet changing, links between cryptocurrency markets and US equity markets. Before the introduction of crypto ETFs, the main cryptocurrencies BTC-USD or ETH-USD moved in the opposite direction from the US market returns, adjusted for other factors. However, since the introduction of ETFs, crypto returns now move in tandem with the US market returns, eliminating the original benefits to crypto diversification. However, the impact of crypto returns on SPY returns is declining, possibly due to the popularity of crypto ETFs.

The changing cryptocurrency dependency structure suggests that crypto ETFs aggregate focussed information pertaining to cryptocurrency innovations. This means that investors choose ETFs over cryptocurrencies as a venue for information sharing, enjoying the protections of the US markets. The cryptocurrencies themselves are possibly evolving into entities comparable to other corporations, where crypto ETFs serve as a proxy of investor sentiment about crypto innovation. These findings are consistent with the recent work that posited that investors bullish on crypto are betting on crypto adoption, much like investors in the 1990s bet on the adoption of, say, online shopping. These changes make US markets less susceptible to crypto swings and less prone to market-wide contagion.

As ever, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Cryptocurrency markets are built diametrically opposite to traditional markets. The markets are global. The market participants are anonymous. Small ”meme” coins can only be issued on the existing large coin infrastructure. In this sense, large cryptocurrencies like Bitcoin and Ethereum act as aggregators and de-factor exchanges for the entire meme coin volume. However, we find that ETH-USD and BTC-USD show no dependency on the changes in the smaller coins. This finding further supports our conclusion that ETH-USD and BTC-USD are becoming increasingly similar to US corporate entities facilitating smaller meme coin issuance as BTC and ETH clients. In other words, Ethereum and Bitcoin are increasingly viewed as other innovative companies, and investors bet on their adoption, just as they did on the adoption of the ”.com” companies in the late 1990s. This finding echoes recent work by Kogan et al. (2024), Cong et al. (2021) and Sockin and Xiong (2023).

SPY returns themselves showed highly persistent negative relationships with the SPY daily returns. Figures 7 and 8 show the distribution of regression coefficients and t-statistics, respectively, from 521 regressions of daily returns of individual ETFs on contemporaneous daily returns of SPY.

Regressions of Bitcoin (BTC-USD) daily returns on individual ETFs also showed very strong, yet positive, statistical dependencies. Figures 9 and 10 summarize the distributions of the regression coefficients and the t-statistics, respectively.

Our first sample period spans October 19, 2021, and lasts through July 22, 2024, the day before the formal introduction of ETHA and ETHV, the first Ethereum ETFs. We show that during this period, Bitcoin’s relationship with most US ETFs has lost statistical significance, while the Ethereum ETF still showed a strong negative relationship between its returns and those on US ETFs. As Figure 18 shows, the t-statistics of the regressions of the daily returns of ETH-USD on those of US ETFs often reached -2 to -4, indicating 99.99% statistical significance of the importance of the SPY-ETH relationship.

Once debiased by the returns on U.S. ETFs, the regression of SPY returns on the debiased BTC-USD and ETH-USD generated significant positive results for both cryptocurrencies. When either ETH-USD or BTC-USD went up by 1%, the S&P 500 went up by 0.1% on average. This is in contrast with the pre-crypto ETF period, when the S&P 500 and crypto returns were negatively correlated.

As this paper shows, crypto currency markets are increasingly intertwined with traditional equity markets. The diversification benefits of crypto observed before the launch of crypto ETFs have mostly disappeared.

At the same time, the introduction of crypto ETFs appears to have created boundaries on the shock transmission between the two domains, with ETFs serving as proxies for crypto pricing, just like traditional stocks do for companies. Crypto ETFs essentially control the negative information spillovers from the cryptocurrency markets onto the broader US markets, the phenomenon known as contagion. In this respect, crypto truly is the new innovative technology, not a new way of the world, and Ethereum and Bitcoin are like firms represented in the US markets by crypto ETFs.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend