Why Did Trend-Following Underperform Last Decade?

Trend-following funds and strategies were extremely popular after the 2008/2009 crisis. They offered attractive performance, and diversification properties made them a nice addition to investor’s portfolios. Ten years later, “trend-following strategy” is not such a popular word. Strategies didn’t blow-up, but their performance was far from spectacular. What are the main reasons for that? Is it an increased correlation among markets? Are trend rules inefficient? An important recent academic study written by Babu, Hoffman, Levine, Ooi, Schroeder, and Stamelos (all from AQR Capital Management) analyzes trend-following performance for each decade in the last 140 years and uses three distinct factors: the magnitude of market moves, the efficacy of trend-following strategies at capturing profitability from market moves, and the degree of diversification across trends in a trend-following portfolio. They show that it’s the first factor (a lack of large risk-adjusted market moves, positive or negative) that had the biggest impact in the last decade. This suggests that trend-following strategies should be able to deliver better performance in the future if the size of the market moves reverts to levels more consistent with the long-term historical distribution of returns…

Authors: Babu, Hoffman, Levine, Ooi, Schroeder, and Stamelos

Title: You Can’t Always Trend When You Want

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3487134

Abstract:

We present a novel framework to decompose the drivers of trend-following performance into (i) the magnitude of market moves, (ii) the strategy’s ability to profit from those market moves, and (iii) the degree of diversification across markets. This framework allows us to examine why trend performance has been below the strategy’s long-term average return during the current decade. We find that the lower performance of the strategy is neither explained by (ii) nor (iii): trend following has continued to profit from market moves and benefit from diversification. Instead, the primary explanatory factor is (i), namely that the average size of global market moves has been more muted than usual in the current decade. The fact that trend-following strategies continue to translate market moves into profits in a diversified manner suggests that trend-following investing may see stronger performance in market environments characterized by more pronounced movements in markets going forward. .

Notable quotations from the academic research paper:

“Our approach builds on the trend-following strategy as defined in Hurst et al. (2013, 2017) and uses data from the late 1800s through 2018. The markets considered include: 29 commodities, 11 equity indices, 15 bond markets, and 12 currency pairs. For each of the markets described above we construct 1-month, 3-month and 12-month time series momentum signals. The three signals are then equally weighted. Positions are sized according to their expected volatilities and then scaled in aggregate such that the portfolio maintains a 10% ex-ante annualized volatility target.

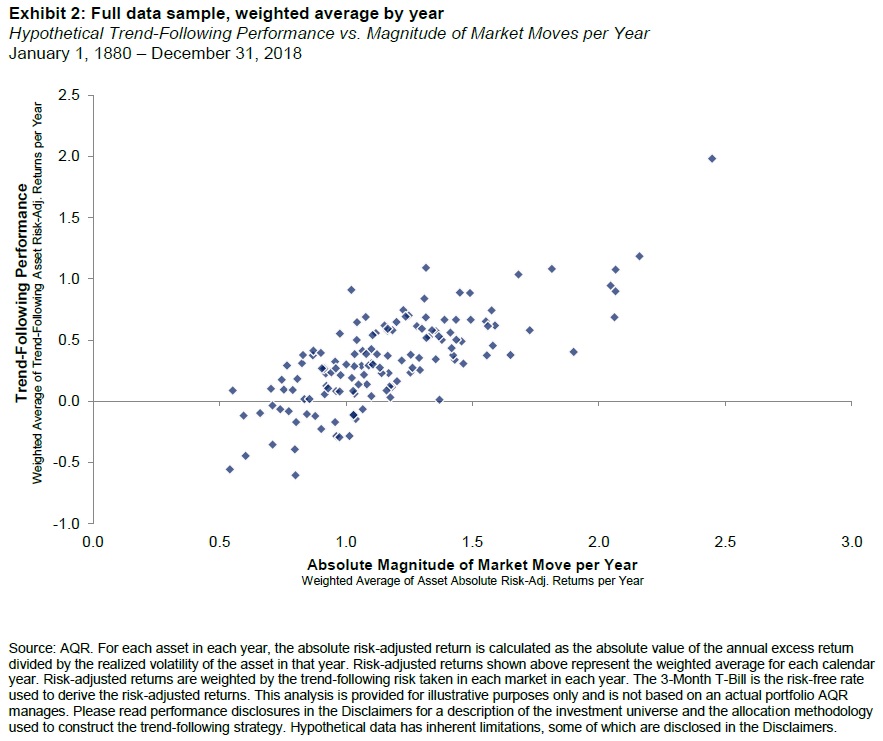

Exhibits 1 and 2 show there is a clear historical positive relationship between the absolute magnitude of moves in individual markets and the risk-adjusted returns of a hypothetical trend-following strategy.

Exhibit 4 depicts the model fit over the current decade of 2010 – 2018 versus the full sample average of rolling decades. (Remember that this reflects hundreds of underlying data points averaged together for the purposes of visual simplicity.) We observe that the magnitude of market moves in the current decade falls closer to the left of the x-axis, indicating that indeed market moves have been small. This effect is replicated in Exhibit 5, which shows the distribution of the magnitude of market moves over the current decade against the distribution using data points from the full sample exclusive of the current decade.

Next we consider whether trend-following performance at the portfolio level has been hindered in recent years by a lack of diversification. There have been many anecdotal assertions that markets may have become more correlated after the Global Financial Crisis due to the heavy-handedness of central bank monetary policies affecting markets. However, the data do not bear this out. Exhibit 6 shows the full sample average diversification multiplier 𝐷𝑇 ̅̅̅̅ for all rolling decades against the current decade 𝐷𝑇. The diversification multiplier for the trend-following strategy has not been materially different in recent history than in the full sample. We can therefore conclude that an unusual lack of diversification does not appear to explain trend-following’s recent underperformance relative to history.

In Exhibit 7, we summarize the impact of the three factors for each decade in our sample. We do not observe any clear and persistent pattern in the impact of any of the factors over time. In the decades where trend following exhibited the strongest performance relative to the full sample, the magnitude of market moves carried a favorable impact. In the 1970s, the decade with the strongest trend performance, all three factors were favorable.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend