Insights from the Geopolitical Sentiment Index made with Google Trends

Introduction

Throughout history, geopolitical stress and tension has been ever-present. From ancient civilizations to today’s world, global dynamics have been largely shaped by wars, terrorism, and trade disputes. Financial markets, as always, have keenly observed and been significantly influenced as a result.

Our article delves into understanding this relation between geopolitical stress and financial markets, particularly the equity market. To briefly explain our approach, we seek to quantify geopolitical stress through an observable Geopolitical Stress Index (GSI). Using this index, we can explore the relation between geopolitical sentiment, good and bad, and instruments available on financial market. Lastly, we seek to see if geopolitical sentiment is something that can be used to impact trading decisions and develop profitable trading strategies.

Literature Review

Our research is largely inspired by and a generalisation of similar work carried out in a variety of other papers available at Quantpedia. Specifically, we refer to an article titled “Can Google Trends Sentiment be Useful as a Predictor for Cryptocurrency Returns?” in which we explored the impact of sentiment on the cryptocurrency market, a theme we also investigate in our own analysis of the equity market.

Additionally, an article The Worst One-Day Shocks and the Biggest Geopolitical Events of the Past Century investigates the impact the ‘worst one-day shocks and the biggest geopolitical events of the past century’ had on financial markets. While there is overlap in this work with ours, we aim to expand on this work carried out in this research by understanding the relation between the stock market and geopolitical sentiment holistically.

Furthermore, another work from Quantpedia Military Expenditures and Performance of the Stock Markets closely aligns with our research objectives. This study examines the relationship between military expenditures and equity markets, touching upon aspects of geopolitical sentiment. In contrast, our study aims to generalise this to geopolitical risks beyond just military spending.

Outside of Quantpedia, a paper Geopolitical Threat, Market Capitalization, and Portfolio Return explores concepts similar to ours, albeit focusing on just the market; therefore, the focus of the study is different from that in our study. Notably, their use of regime switching models offers an extension that could enhance our own analysis, providing insights into different dynamics within our research.

Methodology

We developed the GSI from Google Trends to measure public interest in geopolitical issues because it provides free real-time data and is simple to build. This allows us to gauge shifts in sentiment based on how often people search for terms related to geopolitical tensions. Since Google Trends data is presented as a percentage relative to the highest point of interest over time, we have to rescale each month’s interest level to the maximum observed interest within the data up to that date. This adjustment was done iteratively, month by month, ensuring that each month’s data was normalized against the peak interest observed to that point. For more detailed methodology for rescaling, refer to our previous work on the Crypto Sentiment Index. Finally, we averaged the normalized values across all keywords to produce the final GSI.

The keywords used for Geopolitical Sentiment index include War, Conflict, Military, Nuke, Weapons, Missile, Enemy, Threat, Bomb, Army, Terrorist, Terrorism, Warfare, Killed, Invasion. Data collection began in January 2008 and extends through July 2023. For each keyword, we recalculated Google Trends’ “relative measure of interest” at the end of the sample period to the “relative measure of interest in each month” and averaged individual sentiment numbers.

GSI (Geopolitical Sentiment Index) average of all words (percentile)

Results

To evaluate the potential impact of the Geopolitical Sentiment Index (GSI) on financial markets, we began by testing the hypothesis that changes in the GSI would affect the spread between a defense-focused ETF and a global stock ETF. This hypothesis was grounded in the assumption that increased geopolitical stress would drive up defense spending, thereby benefiting companies within the defense sector and widening the spread between these ETFs. However, our empirical analysis did not confirm a significant relationship. We believe the primary reason for this result lies in the composition of most “defense” ETFs, which typically combine defense and aerospace companies. The inclusion of aerospace firms, which are less directly tied to defense budgets and geopolitical stress, likely diluted the impact of geopolitical events, making these ETFs less sensitive to changes in the GSI.

Given the inconclusive results from the defense ETF analysis, we explored alternative avenues to apply the GSI. A particularly promising direction emerged when we examined the relationship between geopolitical stress and the risk premium associated with small-cap stocks. It is well-documented in financial literature that small-cap stocks carry higher risk relative to their large-cap counterparts (Zakamulin, 2011; Hameed, Lof, Suominen, 2022). This higher risk often translates into underperformance following periods of elevated uncertainty or risk, such as those indicated by rising geopolitical stress. On the other hand, large-cap stocks, which are generally perceived as safer investments, tend to perform better during economic downturns or in environments characterized by geopolitical tension (Ali, 2024).

The differential impact of geopolitical stress on small-cap versus large-cap stocks suggests a nuanced mechanism at play. During periods of increased geopolitical stress, the heightened uncertainty may prompt investors to demand a higher risk premium for holding small-cap stocks, which are more vulnerable to economic disruptions. Conversely, large-cap stocks, with their more established market positions and greater financial stability, may attract investors seeking safety, thus explaining their relatively stronger performance in such periods. This dynamic provides a compelling explanation for the varying performance patterns of small-cap and large-cap stocks in response to fluctuations in geopolitical sentiment, as captured by the GSI.

To assess the predictive power of the GSI on financial markets, we implemented a reversal trading strategy focused on the spread between two key ETFs: the iShares Russell 2000 ETF (IWM), which represents small-cap stocks, and the SPDR S&P 500 ETF Trust (SPY), which tracks large-cap stocks. The IWM-SPY spread serves as a measure of relative performance between these two segments of the equity market, with IWM representing riskier small-cap stocks and SPY representing the more stable large-cap stocks. The reversal strategy was employed because equity markets typically price in information, including geopolitical risks, almost immediately. Consequently, predicting these risks is challenging. However, by observing the immediate market reactions, we can capitalize on the eventual return to a normal state, thus exploiting the reversal in the IWM-SPY spread.

Our strategy was based on the percentage change in the GSI on a monthly basis. Specifically, when the GSI was rising, instead of expecting large-cap stocks to continue outperforming small-caps, the strategy involved taking a short position in SPY and a long position in IWM, anticipating that the initial market reaction would reverse as the situation stabilized. Conversely, when the GSI was declining, the strategy involved going short on IWM and long on SPY, expecting that any initial outperformance of small-cap stocks would revert as the geopolitical tension dissipated. The portfolio was rebalanced monthly to reflect changes in the GSI.

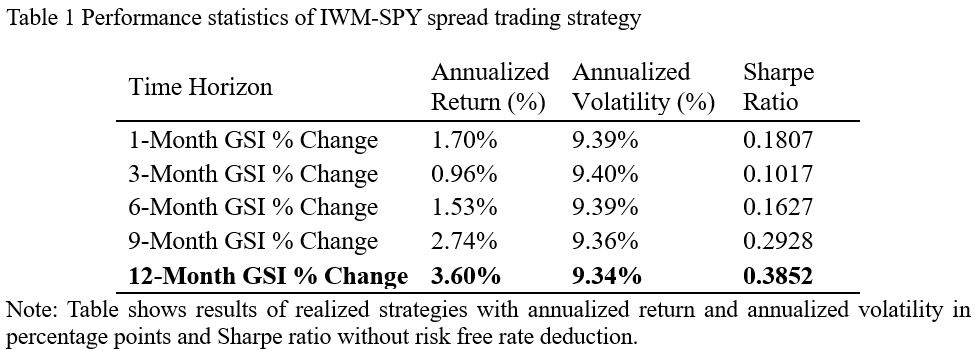

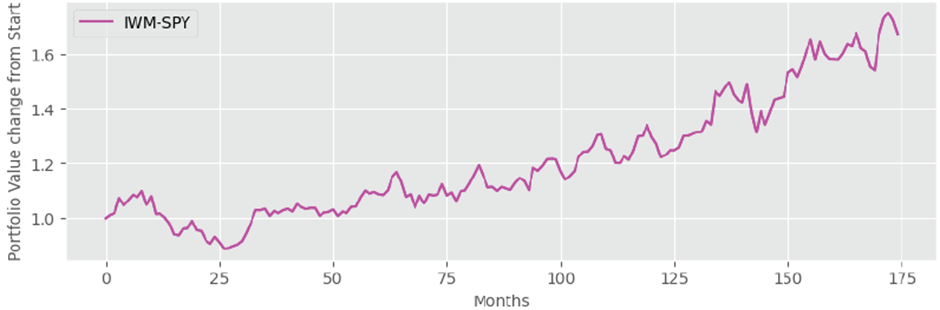

We assessed the effectiveness of using GSI percentage changes over different time horizons—1, 3, 6, 9, and 12 months—to capture different formation periods of the index changes. Among these, the 12-month GSI percentage change had the most significant results, achieving a risk-adjusted return, as measured by the Sharpe ratio, of 0.38. Table 1 presents the performance metrics of the strategy across the selected time horizons of GSI changes. The results suggest that longer-term changes in geopolitical sentiment more effectively explains the relative performance of small-cap versus large-cap stocks.

Equity curve of 12-Month GSI % Change IWM-SPY spread trading strategy

Conclusion

In this study, we set out to explore the relationship between geopolitical sentiment and financial markets by developing the Geopolitical Sentiment Index (GSI). Our primary objective was to determine whether changes in the GSI could serve as a reliable predictor for asset returns within the equity market. Initially, we hypothesized that geopolitical stress would directly influence the spread between defense-related ETFs and global stock ETFs. However, our empirical analysis did not reveal a significant relationship, a result likely attributed to the composition of defense ETFs, which often include both defense and aerospace companies, thereby diminishing their sensitivity to geopolitical events.

Recognizing the limitations of this approach, we redirected our focus towards a potentially more impactful application of the GSI—the influence of geopolitical risk on the performance differential between small-cap and large-cap stocks. This dynamic drives the relative performance of small-cap stocks compared to their large-cap counterparts, aligning with established financial theories.

To validate this insight, we implemented a reversal trading strategy based on the GSI’s monthly percentage change, targeting the spread between the IWM, representing small-cap stocks, and the SPY, representing large-cap stocks. The analysis demonstrated that the 12-month GSI percentage change was the most effective, achieving a Sharpe ratio of 0.38. This finding underscores the potential utility of the GSI as a tool for informing investment decisions, particularly in understanding the relative performance dynamics between small-cap and large-cap equities.

In conclusion, while our initial hypothesis regarding the defense ETF spread did not yield significant findings, this study highlights the value of exploring alternative approaches when investigating complex relationships, such as those between geopolitical sentiment and market behavior. The Geopolitical Sentiment Index has shown promise used with the relative performance between small-cap and large-cap stocks, offering investors a nuanced perspective for navigating the uncertainties inherent in global markets. Future research could enhance this approach by incorporating additional factors or more granular data, thereby potentially improving the predictive power and applicability of the GSI.

Authors:

Shaun Desai, Junior Quant Analyst, Quantpedia

Dominik Cisar, Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend