Quantifying Global Real Estate Returns Over Centuries

In the realm of quantitative finance, understanding the dynamics of real estate returns over extended periods is often overlooked, which is not good, as real estate constitutes a significant portion of investors’ portfolios. The article titled Global Housing Returns, Discount Rates, and the Emergence of the Safe Asset, 1465-2024 fills the gap and provides a comprehensive historical overview of real estate yields, offering a chronological overview of real estate returns not just over a few decades but over several centuries.

What the paper does?

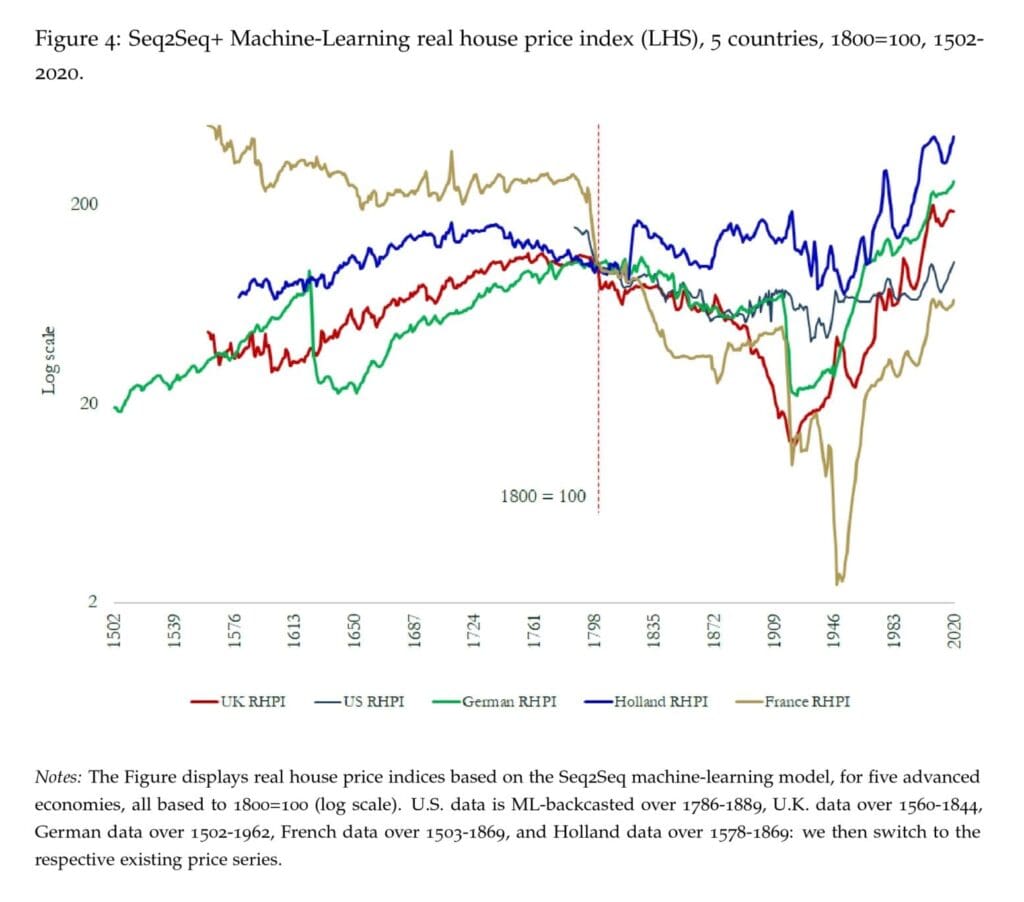

- It constructs a primary-source repeat-sales real house price index (RHPI) for Germany, 1465–2020, from archival property records (Häuserbücher / cadaster).

- Then uses machine-learning backcasting trained on modern data (c. 1845–2020) and long-run covariates (e.g., building-cost indices, mortgage rates) to reconstruct multi-century house-price and return series for the U.S., U.K., France, and the Netherlands, then aggregates to global indices.

Models include modern non-parametric time-series learners (e.g., TiDE, Seq2Seq+, Random Forest). - Finally, reconstructs long-run housing total returns (rental yield + capital gains) in nominal and real terms, and studies their dynamics, predictability, and structural breaks.

And what are the main findings?

- Housing has been far more dynamic over the very long run than the modern-era consensus suggests – The paper shows secular increases in real prices and (excess) total returns, with notable accelerations from the late 18th century onward (e.g., an inflection around the Thirty Years’ War in the German series).

- Total returns are historically dominated by rental yield; capital gains are smaller on average – In the German primary series, long-run real total returns are ~6% p.a. with ~5½% from rental yield and ~0.4% from capital gains; ML-based global reconstructions display similar decompositions over long horizons.

- Discount rates trend down secularly – Multiple constructions point to a clear multi-century decline in housing discount rates, consistent with rising valuations.

- The sovereign “safe asset” premium emerges in the late 17th century – From the late 1600s, rental yields exceed sovereign yields on a sustained basis: sovereign bonds begin to command a positive safety premium relative to housing. (The paper also documents structural breaks consistent with this re-alignment.)

What can we take away from the paper as quants? There were significant shifts in the perception of real estate as a safe asset over the centuries. Historically, real estate has been associated with stable returns; however, the analysis reveals that the expected returns have diminished in recent decades, leading to a reevaluation of its status as a reliable investment vehicle. Housing is becoming more like a bond-like, low-yielding asset rather than a high-return investment. Therefore, investors should temper expectations for capital appreciation and, for long-term investors, income-generating real estate (rental housing, REITs focused on cash flow) is more reliable than speculation on rising home values. It’s a good idea to benchmark real estate vs. government yields, and when spreads are unusually tight, future housing returns are likely unattractive. However, even with lower expected returns, housing remains a useful diversifier in multi-asset portfolios.

Authors: Paul Schmelzing

Title: Global Housing Returns, Discount Rates, and the Emergence of the Safe Asset, 1465-2024

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5269749

Abstract:

This paper reconstructs global housing returns over centuries and presents new stylized facts and inflection points for the asset class, by combining new historical archival data with a novel backcasting machine learning approach. Contrary to consensus, housing markets and valuations have been highly dynamic over the long-horizon — and patterns over recent decades fit in with multi-century trends of rising (excess) returns and real prices. Housing lends itself elegantly to a reconstruction of plausible ranges of discount rates over time: I show that long-horizon discount rates exhibit a clear downward trend, and argue that rising housing valuations — including those over the 20th century — are perfectly consistent with a prolonged fall in discount rates. The counterpart is a “safety premium” that shows an upwards slope over time, the emergence of which I attempt to pinpoint chronologically.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“The first contribution of this paper is therefore to make key empirical progress, and offer new very long-horizon real estate time series that replicate modern methodologies. Property-level repeat sales sources are introduced that allow the reconstruction of house price indices consistent with modern benchmark methodologies (Case-Shiller repeat sales index). In addition, I introduce primary data for a number of covariates of house prices and returns over the very long run, including a new annual series for (real) German mortgage rates, and building cost indices for key advanced economies. Armed with these and other long-run time series, the empirical environment lends itself almost ideally to a novel machine learning (ML) exercise, which will comprise the second key contribution of this paper. Nonparametric machine learning approaches are already widely used for forward-looking predictive approaches in the finance literature – but their potential for backward reconstructions (“backcasting”) of financial time series has so far not been realized. Machine learning trained on modern data can achieve very high out-of-sample predictive power and help more generally to reconstruct financial trends over past centuries: I demonstrate this on the basis of house price reconstructions for the U.S., the U.K., France, and the Netherlands – yielding new multi-century “global” price and return indices.

I […] reconstruct various plausible definitions of discount rates over time. This includes a new primary-sourced multi-century data set for mortgage rates – arguably the most relevant discount rate for housing markets. This new data – together with the fact that rent growth is a stationary variable – allows me to compare implied present values of housing with actual realized prices, over the multi-century horizon. The data echoes the continuities of the current low discount rate environment – suggesting that discount rates are secularly falling, and therefore constitute a plausible prime driver of rising housing valuations – as opposed to explanations that center around rising rent growth expectations. Importantly, comparing implied present values in housing with realized prices does not confirm the existence of a “housing boom” in recent decades. Relative to the trend fall in discount rates, instead, housing in advanced economies tended to be valued at a discount. Across plausible definitions, the fall in discount rates was flatter than the fall in sovereign rates: I identify an important cross-over with sovereign rates that occurred around the late 1600s, and show that the counterpart of falling discount rates are secularly rising “safety premia” for sovereign assets.

This paper argued that recent leaps in both primary source availability and machine learning models now allow us to seriously advance. In the first contribution of this paper, I took advantage of German primary data innovations, which now allow a granular “bottom up” reconstruction of house prices and total returns: using Häuserbücher and newly digitized data, we can construct a new multi-century repeat sales index. Combining such data with machine learning models in a second step – for which I utilize long-run covariates reconstructions, including sourcing new building cost indices –, I provided the first housing price and total (ex post and excess) return series for housing markets covering a substantial share of global aggregate GDP over centuries.

Mechanically, the counterpart of falling discount rates are rising risk premia. Abstracting from particular assumptions in the PV approach, I closed with new raw long-horizon data that confirms that, initially, in the early modern period sovereign interest rates recorded positive yield spreads over rental yields for the same set of key countries, but then dropped more aggressively with time, with an important cross-over occurring around the mid-17th century. Mechanically, this results in a “safety premium” (as defined in this paper) emerging for sovereign assets at this point, with most finance literature simply assuming this measure to be positive by 1700. I argued that the new data also suggests that this safety premium exhibits clear time trends and is secularly increasing for advanced economies, a new stylized fact relevant not least for the vibrant recent finance literature.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend