Portfolio Weighting Schemes for Commodity Futures Risk Premia

Related to commodity trading strategies, mainly to:

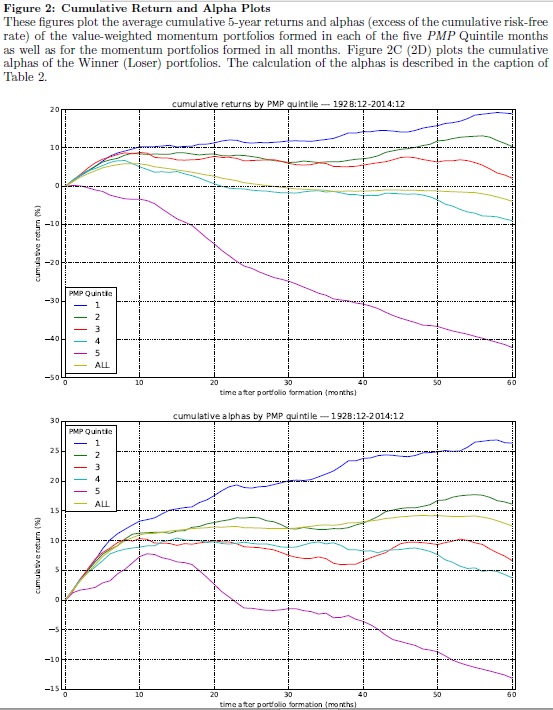

#21 – Momentum Effect in Commodities

#22 – Term Structure Effect in Commodities

Authors: Rad, Yew Low, Miffre, Faff

Title: How Do Portfolio Weighting Schemes Affect Commodity Futures Risk Premia?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2977710

Abstract:

We examine whether and to what extent successful equities investment strategies are transferrable to the commodities futures market. We investigate a total of 7 investment strategies that involve optimization and mean-variance timing techniques. To account for the unique characteristics of the commodity futures market, we propose a novel method of classification based on momentum or term structure properties in the formation of long-short portfolios in conjunction with the quantitative strategies from the equities literature. Our strategies generate significant excess returns and risk-adjusted performances as measured by the Sharpe and Sortino ratios and the maximum drawdown. We find no significant correlation between the strategies’ excess returns and common risk factors. There is no evidence that excess returns are a compensation for liquidity risk. The strategies are robust to transaction costs and choice of model parameters and exhibit stable performance across various market environments including times of financial crises.

Notable quotations from the academic research paper:

"There are theoretical and empirical reasons to believe that commodity futures investments command positive risk premia. The theoretical considerations relate either to the theory of storage where the risk premium depends on inventory levels, and thus on the slope of the forward curve, or to the hedging pressure where the risk premium is a function of hedgers’ and speculators’ net positions. These theories have been empirically validated in numerous empirical studies, all of which highlight that futures returns depend on the fundamentals of backwardation and contango.

In all of the empirical studies, the scheme employed to weight commodities within a portfolio is equal-weighting. The rationale for this choice comes from the fact that unlike in equity markets, there is no natural value-weighting that can easily be applied; its equivalent (production and consumption weighting) is hard to implement given how difficult it is to collect reliable inventory data. This paper proposes to relax the assumption of equal weights and to test whether weighting schemes emanating from the equity literature could be more profitable. These weighting schemes pertain to mean-variance optimization and volatility timing.

Our first contribution is to apply the weighting schemes of the equity literature to the commodity markets. In total, eight weighting schemes are considered; these can be split into an equal-weighting scheme, two optimization schemes, and five timing schemes. The equally weighted scheme is standard in the commodity pricing literature. The optimization strategies follow Markowitz (1952) and are based on mean-variance (MV) and minimum variance (MIN). When it comes to the timing strategies, three approaches follow Kirby and Ostdiek (2012) and define portfolio weights based on volatility timing (VT), beta timing (BT), and reward-to-risk timing (RRT); the other two are novel and based on tail risk as modeled via Value-at-Risk (VaR) and conditional Value-at-Risk (CVaR).

Our second contribution is to amend the aforementioned weighting algorithms so as to consider the specificities of backwardation and contango that prevail in commodity futures markets. We do that by adding a novel step to the weighting procedure that considers either past performance or the slope of the term structure of commodity futures prices as a buy or sell signal for each of the commodities present in the cross section at the time of portfolio formation. This method allows for the possibility of being either long or short while mitigating common issues such as extreme weights or artificial inflation of returns due to the self-financing nature of long-short positions.

Our findings indicate that the optimization-based and timing strategies perform well, as measured by a range of risk-adjusted return metrics (Sharpe and Sortino ratios, Maximum Drawdown, and VaR and CVaR). We find no evidence that returns from the investment strategies are compensation for liquidity risk. Our investment strategies are robust to transaction costs and the the choice of model parameters. We show two alternative methods of classifications, that nominate commodity futures for long or short positions based on momentum and term structure, exhibit similarly strong performance. We also show that our strategies are stable in various market conditions, from crisis to high growth periods. we document that these strategies are amongst the most profitable in the literature and show that common risk factors in the commodity futures market are unable to account for their positive and significant excess returns."

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

"

"