Size, Value and Equity Premium Waves

A new financial research paper has been published and is related to:

#25 – Small Capitalization Stocks (Size) Premium

#26 – Value (Book-to-Market) Anomaly

Author: Herskovic, Kind, Kung

Title: Size Premium Waves

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3220825

Abstract:

This paper examines the link between microeconomic uncertainty and the size premium across different frequencies in an investment model with heterogeneous firms. We document that the observed time-varying dispersion in firm-specific productivity can account for a large size premium in the 1960's and 1970's, the disappearance in the 1980's and 1990's, and reemergence in the 2000's. Periods with a large (small) size premium coincide with high (low) microeconomic uncertainty. During episodes of high productivity dispersion, small firms increase their exposure to macroeconomic risks. Our model can also explain the strong positive low-frequency co-movement between size and value factors, but a negative relation with the market factor.

Notable quotations from the academic research paper:

"The relation between firm size and expected stock returns has varied signifi cantly over time in waves. Banz (1981) documented a size premium whereby firms with small market capitalizations earn higher expected returns than large ones before 1975, and that this size e ffect cannot be explained by market betas. The size e ffect subsequently vanished starting in the early 1980s to the late 1990s, before reemerging after 2000.

We also observe that measures of microeconomic uncertainty, such as the cross-sectional dispersion in plant- and firm-level total factor productivity (TFP), sales, and payouts, exhibit similar low-frequency patterns as the size premium.

Figure 1 illustrates that microeconomic uncertainty is strongly positively correlated with the size premium. In this paper, we demonstrate how persistent variation in microeconomic uncertainty can potentially rationalize the observed size premium waves.

To this end, we build a dynamic partial equilibrium production model with heterogeneous firms. The model has several distinguishing features. First, firms are subject to persistent idiosyncratic and aggregate TFP shocks with time-varying second moments. The second moment shocks to the idiosyncratic component capture time-varying cross-sectional dispersion in idiosyncratic productivity (microeconomic uncertainty) while the second moment shocks to the aggregate component capture fluctuations in macroeconomic uncertainty. Second, firms face quadratic adjustment costs and operating costs. Third, the representative household has recursive utility de fined over aggregate streams of consumption.

We find that our calibrated model produces a realistic size premium and captures the salient dynamics of the size premium across diff erent frequencies. Namely, the model generates a countercyclical size premium and reproduces the low-frequency wave patterns, including a large spread during 1960-1980, a disappearance between 1980-2000, and resurgence post-2000. The mean-reverting idiosyncratic TFP shocks helps to generate a negative relation between firm market capitalization and expected returns in the stationary distribution.

Small firms are those that have received a recent history of negative idiosyncratic shocks. Due to mean reversion, the shorter-term payouts of small fi rms therefore constitute a smaller share of aggregate payouts relative to their longer-term payouts. With a similar logic, the payout shares of large firms have the opposite pattern. Consequently, small firms are more exposed to aggregate long-run risks than large firms, which gives rise to a quantitatively signi ficant size premium.

The low-frequency fluctuations of the size premium in the model are driven by the persistent volatility process for idiosyncratic TFP shocks. When TFP dispersion is high, small fi rms are subjected to a larger history of negative idiosyncratic shocks that increases their exposure to longrun risks relative to periods with low TFP dispersion. As a result, the size premium is larger during periods of higher TFP dispersion. In the data, we find a very strong association between TFP dispersion and the size premium at low frequencies, consistent with the model predictions. Calibrating the idiosyncratic volatility process to our empirical measure, we show that our model can provide a quantitatively relevant account of the observed size premium waves.

The equity premium is strongly correlated with macroeconomic uncertainty, as measured by the realized volatility of consumption growth, output growth, and TFP, but negatively related to microeconomic uncertainty at low frequencies. The correlation between the equity premium and macroeconomic uncertainty is 0.76, while the correlation between the equity premium and microeconomic uncertainty is -0.64 (See Figures 3 & 4).

The model also generates signifi cant equity and value premia, inline with the observed magnitudes in the data. Persistent shocks to aggregate productivity growth are a source of long-run risk that help to generate a sizable equity premium when coupled with recursive preferences. Persistent second moment shocks to aggregate productivity growth generate a countercyclical equity premium.

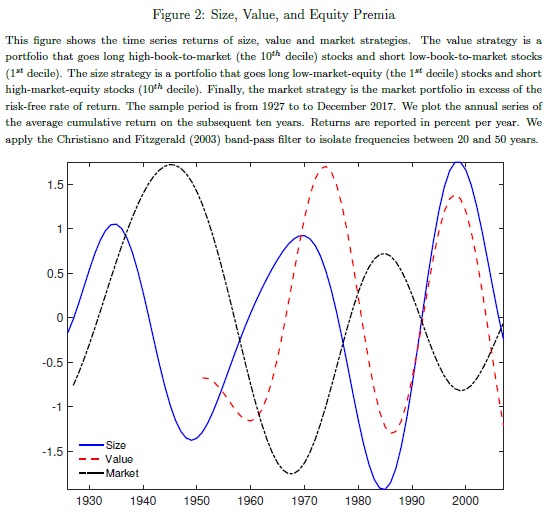

The size an value premia are strongly positively related at low frequencies (i.e., correlation of 0.66), but they are both negatively related with the equity premium at low frequencies (correlation between the size premium and the equity premium is -0.62 and the correlation between the value premium and the equity premium is -0.50). Figure 2 provides a visual depiction of these relations.

A value premium arises due to the combination of the asymmetric capital adjustment costs and operating costs, in a similar spirit as Zhang (2005). Firms with high book-to-market ratios have large stocks of capital, but have experienced a recent history of negative idiosyncratic shocks. Therefore, such firms have strong incentives to disinvest due to the low marginal product of capital and high operating costs, but the presence of capital adjustment costs prevents them from selling off their unproductive capital rapidly, which exposes high book-to-market (value) fi rms more to adverse aggregate shocks than low book-to-market (growth) firms. In particular, discouraging aggressive disinvestment policies prevents fi rms with large capital stocks from increasing payouts financed through capital sales in response to negative idiosyncratic shocks. The operating costs that are proportional to the capital stock of the firm reduce the funds available for payouts, especially for large fi rms. Therefore, these investment frictions imply that high book-to-market fi rms have low payout shares today, but higher payout shares at longer horizons due to mean reversion. Therefore, value firms are more exposed to long-run risks than growth firms, thereby generating a sizable value premium. The low-frequency fluctuations of the value premium are driven by the persistent idiosyncratic volatility process."

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia