A Few Thoughts on Pragmatic Asset Allocation

One of the main reasons why the Pragmatic Asset Allocation Model was designed is to give investors a tax-efficient possibility to invest in a global equity portfolio with a lower risk than the passive buy&hold approach. Therefore, the PAA model is not the “absolute return” model but rather the tactical model that prefers to invest in the equity risk premium and move to the hedging portfolio (gold, treasuries, or cash), only for short periods and only when it’s absolutely necessary. We use price trend+momentum indicators and yield curve inversion as signals for such situations when (based on the past data) there is a higher probability of recessions and equity bear markets.

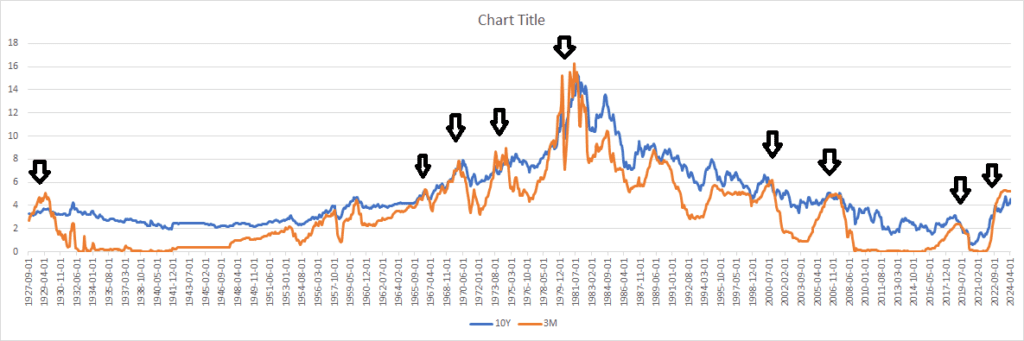

The yield curve inversion signal has an important position in the whole model and last such signal for avoiding equities occured at the end of the 2022 and when the 3-month yields jumped significantly over the 10-year yield. Such situations are not uncommon and happened a lot of the time over the last 100 years.

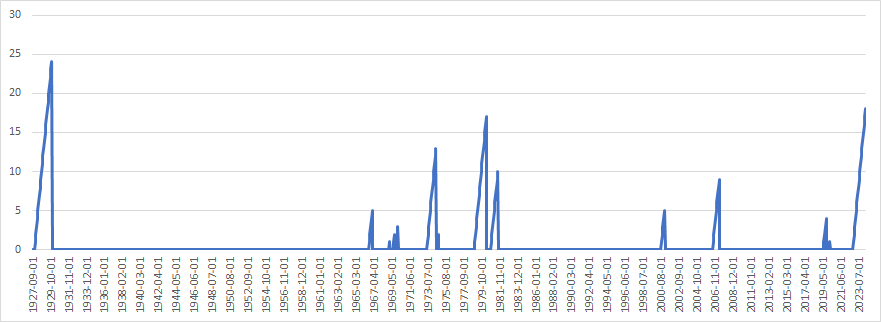

What is unusual in the current situation is the length of the time that the YC is inverted (19 months at the moment), which makes it the 2nd longest YC inversion in the last 100 years (the longer was only the inversion in the 1920s).

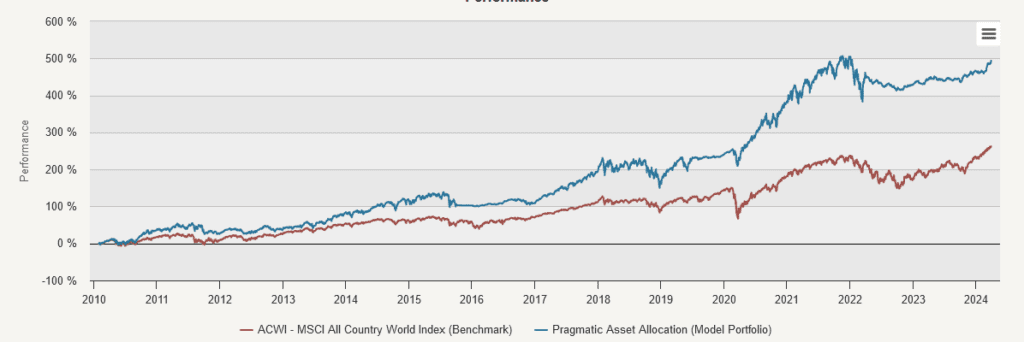

In the current situation, the FED is not very inclined to lower the short-term rates, and it seems that the YC will stay inverted for a significantly longer period. This year, we will break the record from the 1920s in the length of the YC inversion. As we mentioned before, the PAA model’s intention is to hold mainly the equity portfolio; however, in the current situation, the portfolio consists of gold (37.5%) and cash. The long-term performance of the model is not impacted significantly by omitting the equities in the last 1.5 years, as the chart shows (comparison of the performance of the PAA model and ACWI benchmark).

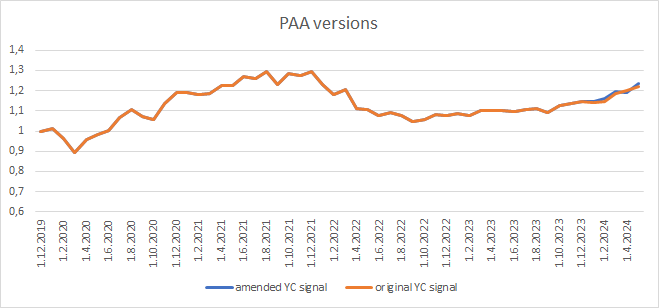

However, there still can be investors, that can feel uncomfortably by not holding equities for a long period of time due to YC inversion when price/momentum signals already turned positive. We received request to explore YC signal amendment for this situation. So, what is the solution?

We can amend the YC signal in a way, that if the yield curve inverts, then we will switch current tranche from risky assets to the hedging portfolio (or cash), but the YC signal switch is valid only for 12 months. So after the 12 months, if the YC signal still signals the recession but MA signal is positive, then we do not take YC signal into the consideration.

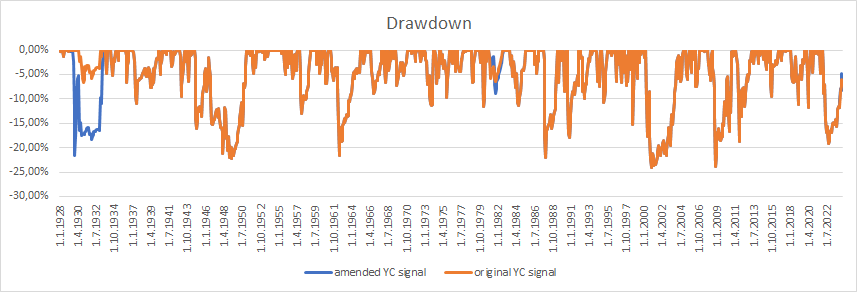

What’s the result of such an amendment? The long-term results show no big difference. The performance of the original model (without any changes to the YC signal) is 10.73%, volatility 11.48%, and max drawdown -23.98%, which gives a Sharpe ratio of 0.93 and Sortino 0.45. A strategy with an amended YC signal has a performance of 10.62%, volatility of 11.68%, and max drawdown -of 23.98%, which gives a Sharpe ratio of 0.91 and a Sortino ratio of 0.44. As we can see, the results are negligible. The main difference occurred in the 1920s when the model with an amended YC signal bought stocks too soon in 1929 and experienced some drawdown at that time. On the other hand, PAA, which uses the original YC signal, didn’t have this drawdown in 1929.

And what about current times? What’s the difference between both versions? The original PAA is invested mainly in cash (62.5%) and gold (37.5%). The PAA, with an amended YC signal, started to invest in equities at the end of January 2024 and currently has 32.5% in cash, 25% position in Nasdaq, 25% in world stocks, and 12.5% in gold. The total performance difference over the last four years is approximately 3%. The amended PAA version outperforms the original PAA a little, as Nasdaq outperformed gold over the previous six months, but the total difference isn’t anything that stands out as extraordinary.

Of course, the question is: What version is better – the original YC signal or the amended YC signal? There isn’t a definitive answer to that. By amending the YC signal, the amended PAA allows for the sooner investment in equities. However, we would have to base our current decision on one data point; we do not have enough data to say that’s the right thing to do, as the only time the amended model ignored inverted YC was in 1929 (and it definitely wasn’t a good idea). In the last few months, risky assets have outperformed hedging portfolio, but will the outperformance persist? Nobody knows. But if our experience with trading taught us something, then it’s to remain flexible.

So, in this case, the answer probably lies in each individual’s tolerance for risk and FOMO feeling. For growth-oriented individuals, it’s probably better to amend the YC signal and gradually go into equities, even if it increases risk. For the individuals who prefer defense, it’s probably better to still hold cash (which still offers interesting yield) and gold. In the short term, the performance of both versions will slightly differ; in the long term (decades), both versions will probably perform approximately the same.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend