An Extensive Test of Market Timing Strategies in the Gold Market

Authors: Bartsch, Baur, Dichtl, Drobetz

Title: Investing in the Gold Market: Market Timing or Buy-and-Hold?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3202658

Abstract:

While the literature on gold is dominated by studies on its diversification, hedging, and safe haven properties, the question “When to invest in gold?” is generally not analyzed in much detail. We test more than 4,000 seasonal, technical, and fundamental timing strategies for gold. While we find large gains in economic terms relative to the buy-and-hold benchmark for several strategies, the results are robust to data-snooping biases only for selected technical trading strategies. These superior technical trading strategies outperform the buy-and-hold benchmark because they shift out of the gold market following a prolonged trend of negative gold market returns. We verify that the outperformance is not driven by a systematic reaction to the broader market environment and conclude that our results point to the presence of behavioral biases inducing gold market trends.

Notable quotations from the academic research paper:

"The question when to invest in gold has received remarkably little attention, while most research focuses on the diversification, hedging, and safe haven properties of gold. This study aims to close this gap by analyzing if an active investor can beat a passive buy-and-hold strategy by timing the gold market. For our evaluation period from January 1990 to December 2015, our back-test results for more than 4,000 different seasonal, technical, and fundamental trading strategies reveal that significant excess returns were possible.

To construct a comprehensive collection of market timing strategies, we build either on the economic properties of gold or incorporate the findings regarding previously surveyed anomalies in gold prices. In this section, we describe the strategies, rules, and variables used to predict gold returns.

Seasonal trading strategies:

Baur (2013) provides evidence for monthly seasonality in the gold market, with positive and statistically significant gold returns limited to the months September and November. Similar results are shown by Qi and Wang (2013) for the Chinese gold market and Naylor, Wongchoti, and Ith (2015) for U.S. gold ETF returns. To exploit this monthly anomaly, an investor could follow a simple strategy that invests in gold in September and November and reverts to holding cash in the remaining months. Although this strategy is supported by economic intuition, e.g., by the increased wedding season gold jewelry demand in India, the strategy itself is merely mechanic. Therefore, to address the concern that this strategy has simply been ‘mined’ from the data, we follow Dichtl and Drobetz (2014) and implement a more comprehensive approach: Each month, an investor can either be invested 100% in the gold market, or 100% in cash. In this vein, we obtain 212 = 4,096 different monthly seasonal allocation strategies, labeled from SEA0 to SEA4095, where SEA stands for seasonal.

Technical trading strategies:

Moskowitz, Ooi, and Pedersen (2012) find time series momentum in monthly returns of several liquid instruments, including gold futures. Therefore, we include monthly technical trading strategies based on moving average and momentum indicators in our empirical analyses. We invest in the gold market if the short moving average is above the long moving average and revert to holding cash otherwise. The short index for the moving average is set to = 1, 2, 3 and the long index to = 9, 12, which results in six moving average strategies. We also set = 1 and = 10, 24, 36, 48 to cover some other parameterizations that are popular in the literature and among investors. Overall, we employ ten different moving average strategies. We invest in gold if the gold market exhibits positive time series momentum. Otherwise, an allocation is taken in the cash market. Following Moskowitz, Ooi, and Pedersen (2012), we set = 1, 3, 6, 9, 12, 24, 36, 48 months.

Fundamental trading strategies:

Building on the economic properties of gold, a lot of researchers identify several fundamental factors that serve as predictors of future gold returns by affecting either the demand and supply of gold or market participants’ expectations thereof. To construct tradeable strategies based on these fundamental factors, we first estimate a simple linear regression model for each predictor variable (11 predictors in total) for forecasts of the spot price of gold. We also exploit the simple mean of all individual forecasts ( ) as another potential market timing strategy. We also consider a “kitchen sink” forecast ( ), which incorporates all available predictor variables simultaneously in a multivariate regression model.

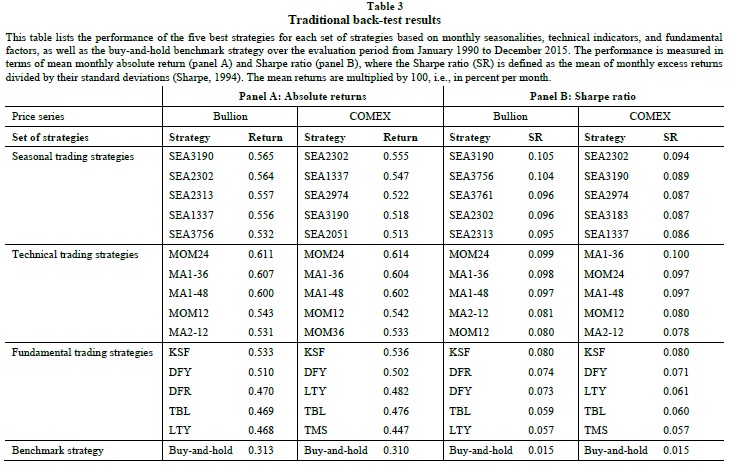

We measure the performance of our market timing strategies in terms of mean absolute returns and mean risk-adjusted excess returns, or Sharpe ratios (Sharpe, 1994), over the evaluation period. Table 3 lists the five best market timing strategies for each of the three strategy groups, i.e., seasonal trading strategies, technical trading strategies, and fundamental trading strategies.

Overall, while the results in Table 3 already provide a first indication which strategies perform well compared to the buy-and-hold strategy, these analyses neither test for statistical significance nor account for the data-snooping problem.

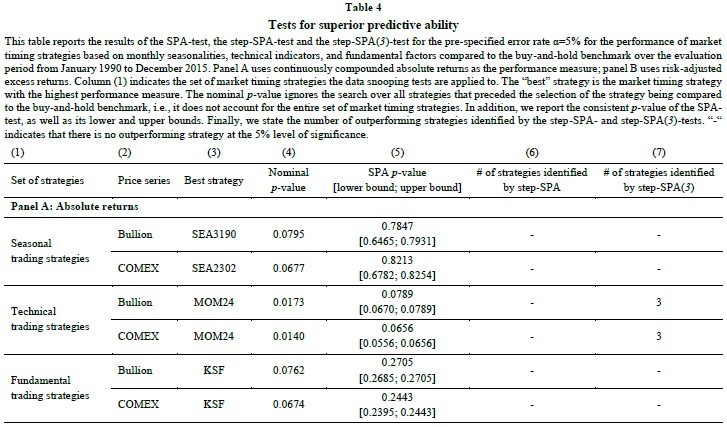

However, because all timing strategies are tested on the same data set, the observed outperformance may simply result from chance and not due to any robust relationship. To account for this data snooping bias, we apply a multiple testing framework and find that only a limited number of technical trading strategies show a statistically significant outperformance relative to the buy-and-hold strategy.

To assess the statistical significance of performance relative to buy-and-hold, while controlling for data snooping, we use Hansen’s (2005) SPA-test to all three types of strategies. In each test, the strategies are compared with the performance of the buy-and-hold benchmark. Accordingly, the first test considers all 4,095 different monthly seasonal trading strategies,12 the second test all 18 technical trading strategies, and the third test all 15 fundamental trading strategies. The SPA-test results are presented in Table 4.

To further examine the characteristics of these superior technical trading strategies, we verify their long-term market timing ability using a conditional market model and preclude that their excess returns are compensation for crash risk, i.e. periods of persistent negative returns. Moreover, we find that the outperformance of these strategies is not driven by different economic and financial regimes. We thus conclude that the superiority of those timing strategies comes from the presence of behavioral biases in the gold market. As pointed out by Hurst, Ooi, and Pedersen (2013), trends emerge if market participants initially underreact to new information, possibly due to anchoring or conservatism. Trend-following strategies, such as time series momentum or moving-average rules, capitalize on the subsequent price changes, since the market price only gradually incorporates the full effect of the news. Once a trend has started, a delayed over-reaction may even exacerbate the trend, e.g., due to herding behavior, feedback trading, or biased self-attribution."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend