An Interesting Cross-Asset Class Analysis of Risk Premiums

Author: Ebner

Title: Risk and Risk Premia: A Cross-Asset Class Analysis

Link: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2711624

Abstract:

The existence of risk premia has been widely documented in the academic literature over the past decades. Until now they have typically been handled as separate phenomena for specific markets or asset classes and thus examined independently. This study analyses risk premia across a variety of asset classes and risk styles to uncover their common performance characteristics, underlying risk sources and return’s sensitivity to economic factors. Based on a set of 16 risk premia over a 22 year sample period we were able to illustrate that risk premia’s expected returns are significantly influenced by their volatility and their sensitivity to funding liquidity and market volatility. Furthermore we show that macroeconomic factors such as industrial production and inflation have a significant effect on the expected returns of the entire set of risk premia. Finally, analysing the link between premia and the global market portfolio shows that premia with unfavourable comoments possess superior expected returns.

Notable quotations from the academic research paper:

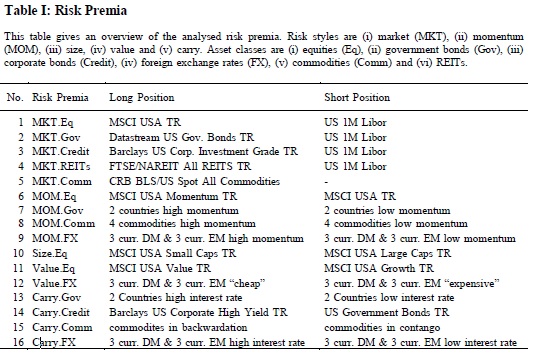

"This study initiates with the analysis of return characteristics for 16 risk premia over a 22 year sample period.

We show that the expected return of a risk premium is significantly affected by its volatility. In other words, higher risk premia volatilities go hand in hand with higher expected returns. However, the analysis of risk premia’s skewnesses and kurtoses does not provide significant results. Subsequently, we build a global cross-asset market portfolio and analyse how risk premia comoments determine their expected returns. The idea behind this is that investors are not compensated for diversifiable risk in equilibrium, but for their systematic risk exposure. The results are in line with the efficient market hypothesis and show that risk premia when adding positive cokurtosis or negative coskewness to a diversified market portfolio have significantly higher expected returns. However, we do not find significant results for a risk premium’s beta exposure to the global cross-asset market portfolio. The second part of the analysis studies the relevance of economic conditions affecting risk premia returns. Considered factors are change in industrial production and inflation, market volatility and market- and funding liquidity. We start with a regime analysis which documents considerable differences in a risk premia’s return given subject to economic conditions.

Comparing risk premia over different regime classifications, this analysis shows the intuitive result that the risk premium “government market” generates attractive returns during unfavourable market regimes and serves as a “safe haven” investment. However, it is not the only risk premium with higher returns during unfavourable periods. For example “commodity momentum” and “FX value” also generate attractive returns during unfavourable market conditions. Afterwards we analyse the expected return of risk premia contingent on each of the economic conditions. We see that during periods of high industrial production changes and low inflation changes, risk premia per se possess higher expected returns. This is also true during periods of high funding liquidity. This study concludes with an analysis of how risk premia’s expected returns are linked to their sensitivities to economic factors. We show that risk premia with higher sensitivities to funding liquidity and market volatility possess significantly higher expected returns."

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see performance of trading systems we described? Check http://quantpedia.com/Chart/Performance

Do you want to know more about us? Check http://quantpedia.com/Home/About