Combining Gold, Bonds and Low Volatility Stocks

Even though gold is generally a volatile asset, it is often considered a key diversifier, hedging against inflation or protecting during economic uncertainties. According to the authors (Pim van Vliet and Harald Lohre), in times of extreme macroeconomic events, including war, hyperinflation, or major economic recessions, gold investing is widely regarded as a safe haven. However, using gold as a hedge comes at the cost of lower returns. The authors explored the importance of gold in investment portfolios and its ability to reduce the risk of losses combined with bonds and stocks. Compared to many existing studies, they also consider a longer timeframe and the impact of inflation.

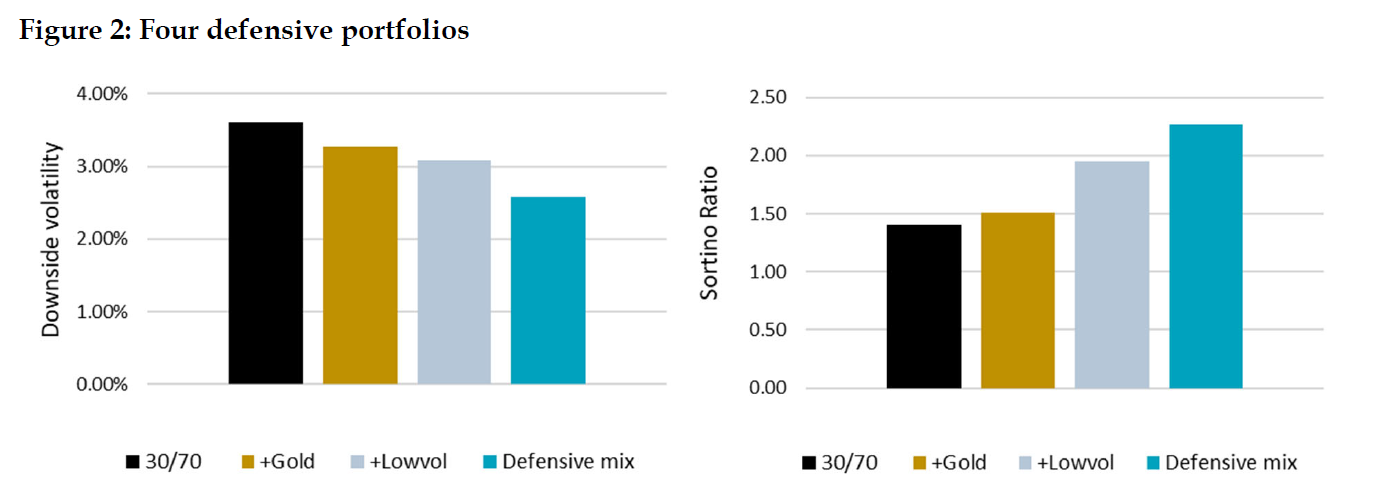

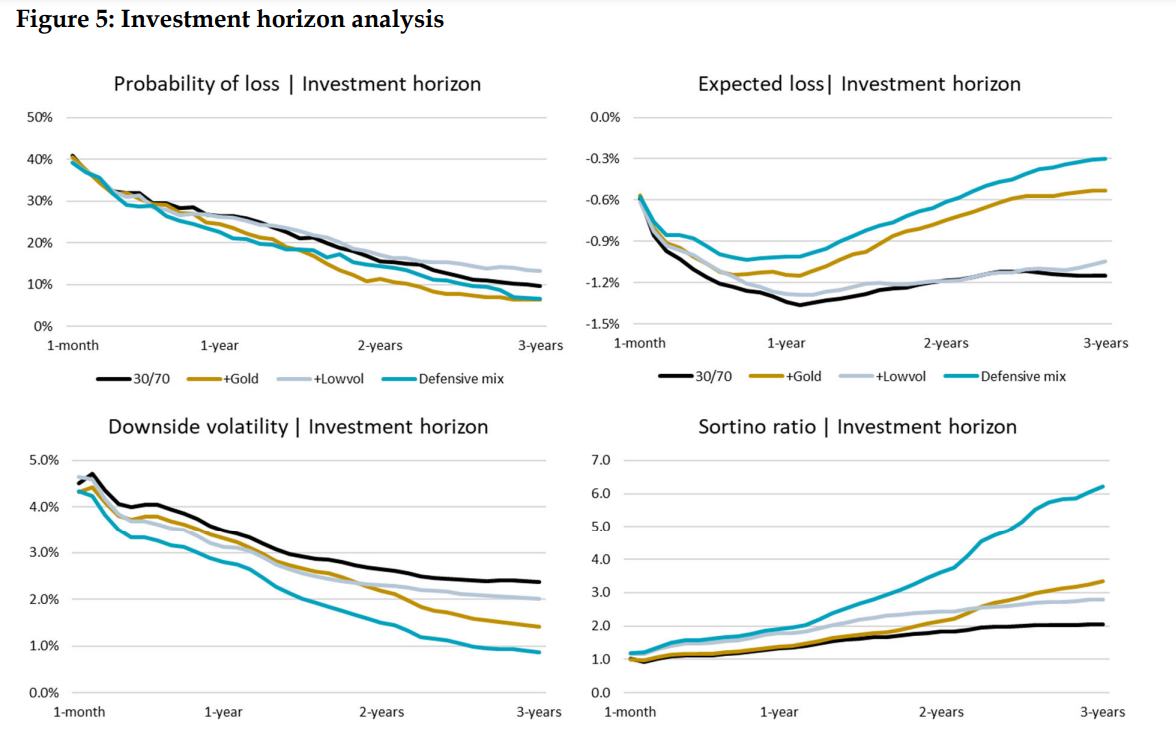

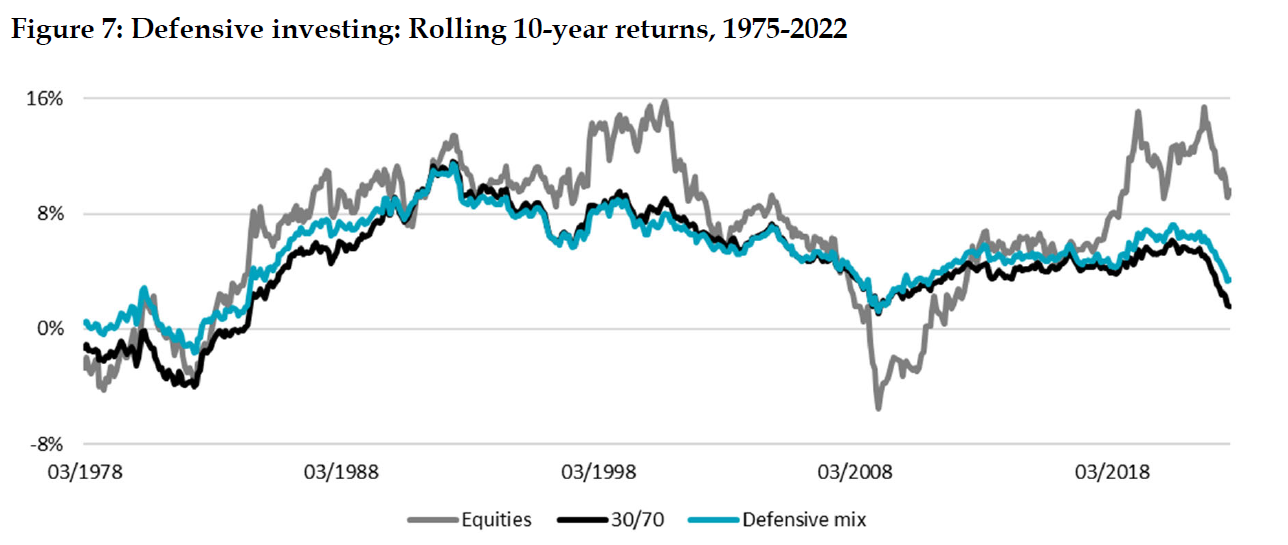

Firstly, they started with a 50/50 stock-bond portfolio, gradually increasing the allocation to gold by 5 percent. They discovered that the minimum risk portfolio comprises 45% equities, 45% bonds, and 10% gold. This portfolio reduces the downside volatility to 3.7%, compared to the original 50/50 stock-bond portfolio with downside volatility of 3.9%. Secondly, the authors replaced the equity market with defensive low-volatility stocks. They created a Defensive mix portfolio, allocating 45% to low-volatility equities, 45% to bonds, and 10% to gold, reducing the downside volatility to 2.6%. This change significantly enhanced defensiveness without giving up returns. To summarize, finding the perfect combination of safe havens is challenging. Nevertheless, a mix of low-volatility stocks, bonds, and a small allocation to gold can be beneficial in minimizing potential capital losses.

Authors: Pim van Vliet and Harald Lohre

Title: The Golden Rule of Investing

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4404688

Abstract:

While gold is a volatile asset, it is often considered a safe haven that offers protection during bear markets. We study this safe haven hypothesis by analyzing a strategic allocation to gold for a loss averse investor with a 1-year evaluation horizon. A modest allocation to gold indeed helps to reduce downside risk of traditional stock-bond allocations, yet such risk reduction comes at the cost of return. Conversely, low-volatility stocks are more effective in reducing losses without giving up returns. As a result, a stock-bond-gold allocation considerably benefits from embracing low-volatility stocks, and allows for increasing the equity allocation at the expense of bonds. Notably, the effectiveness of this defensive multi-asset portfolio increases with the investment horizon.

As always we present several interesting figures:

Notable quotations from the academic research paper:

„The key findings of our empirical study starting in 1975 using 1-year real returns are summarized in Figure 2. A modest gold allocation in a traditional mix of equities and bonds reduces the risk of capital losses by around 10 percent across a wide range of equity-bond allocations. Still, adding gold also reduces the return leading to a small increase in the Sortino ratio, which measures the return per unit of downside volatility. Importantly, the downside risk can be reduced even more by adopting a low volatility style in the equity investment and letting this defensive equity allocation replace part of the bond allocation. This defensive equity allocation at the expense of bonds increases the return leading to a significantly higher return/risk ratio when compared to adding gold. Still, a defensive mix which augments the latter portfolio a modest allocation to gold has significantly lower downside risk than a traditional equity-bond portfolio, with higher returns leading to the largest increase in the Sortino ratio. Thus, this defensive strategy is effective in adhering to the golden rule of investing, while still delivering long-term capital growth.

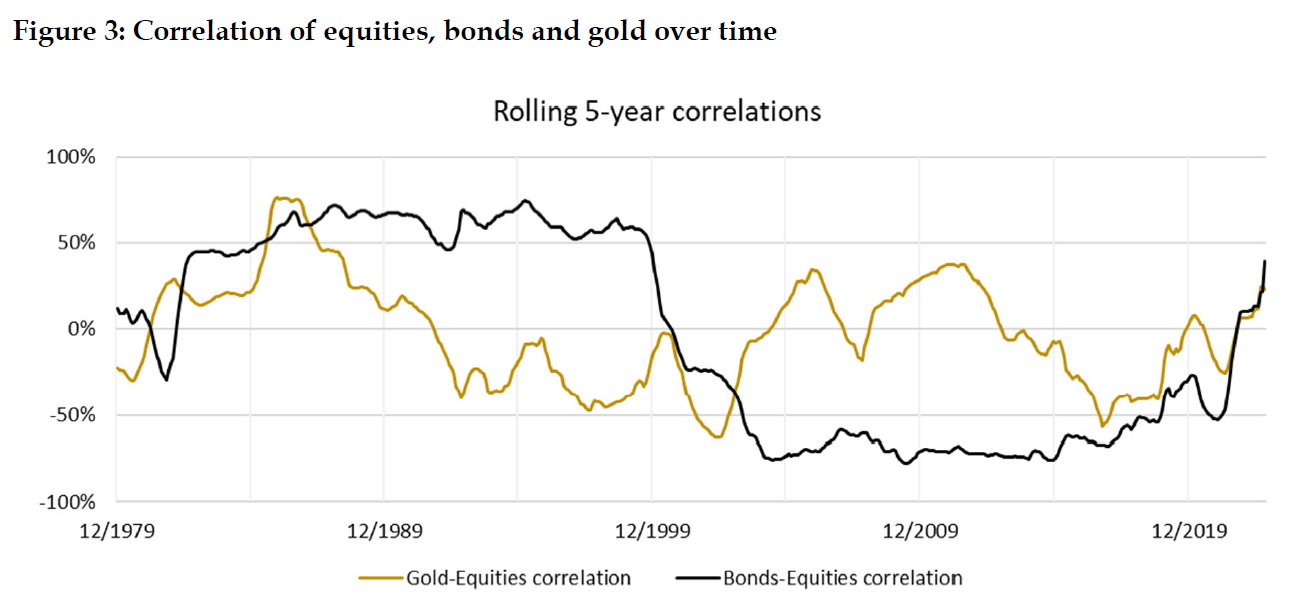

To shed further light on the underlying dynamics, Figure 3 shows the annual correlations between equities, gold and bonds over a rolling 5-year period. While these correlations are around zero over the full sample period, they display significant time-variation. The gold-equity correlation shows less fluctuations than the bond-equity correlation.

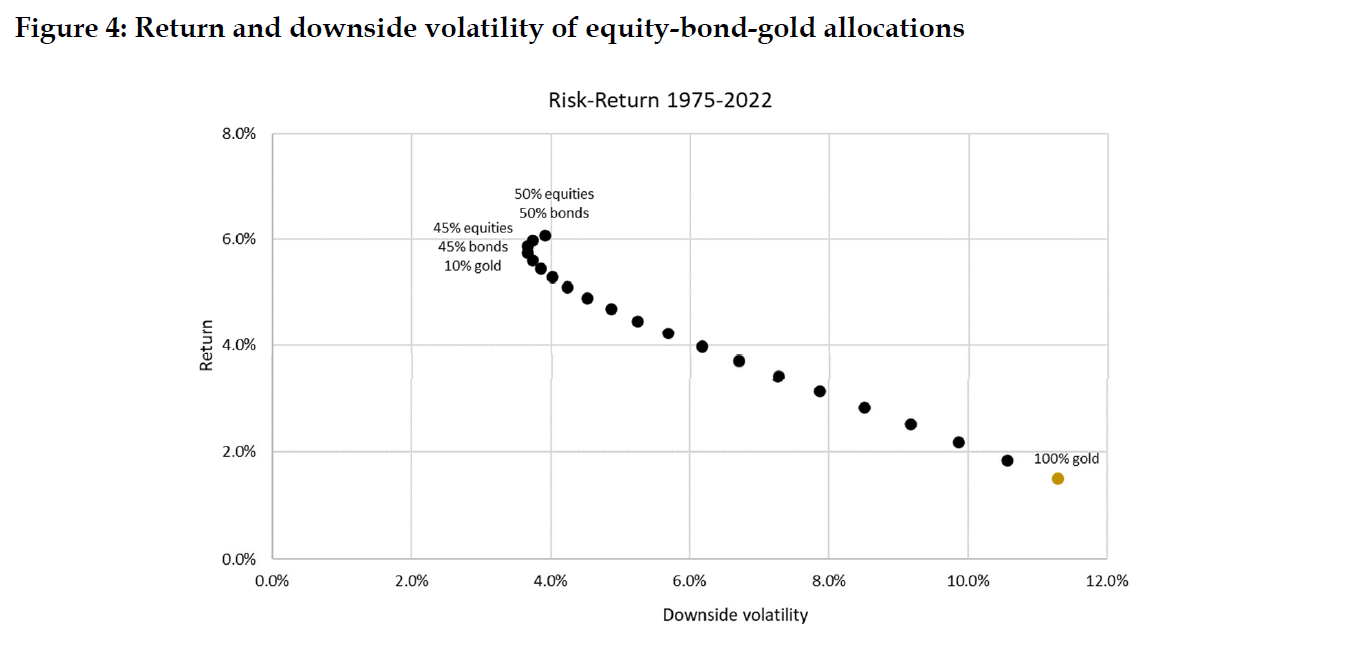

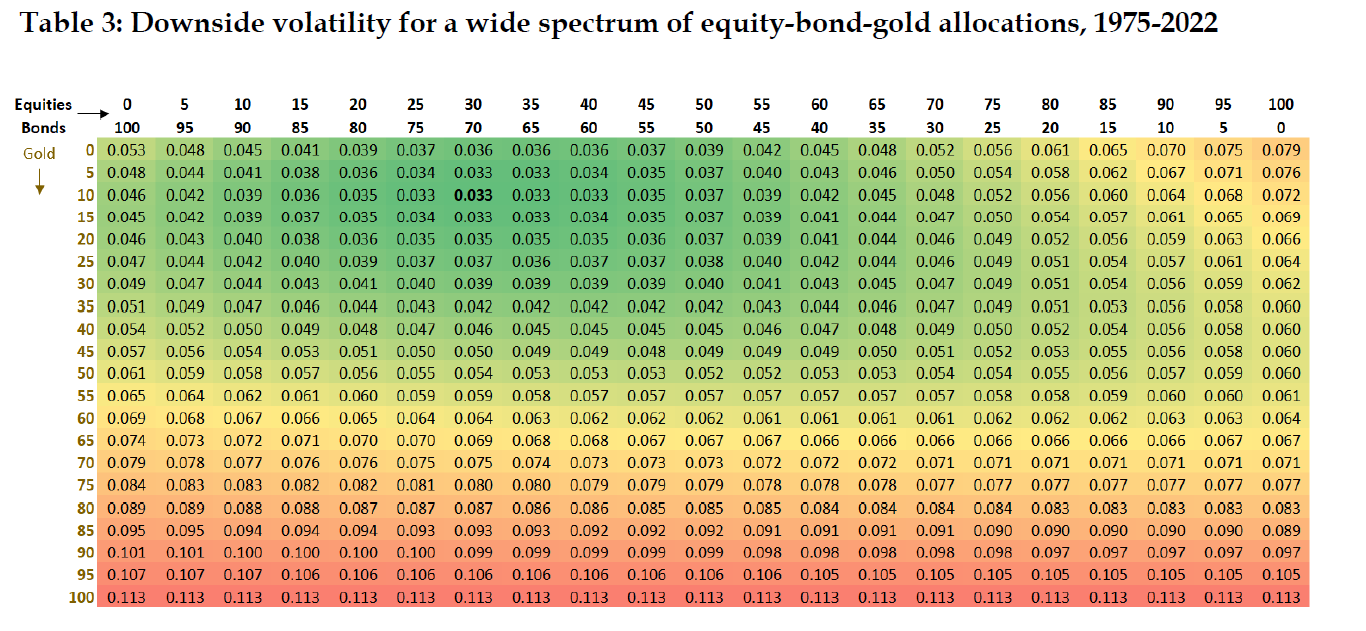

To get a sense of the relevance of gold in a multi-asset context, we next consider a plain 50/50 equitybond portfolio to which one sequentially adds 5 percent gold allocation increments up until one is fully invested in gold. […] Figure 4 plots the average realized return versus downside volatility (also referred to as semi-deviation, again with inflation as the target threshold). The ‘nose’ of the efficient frontier shows that the minimum risk portfolio is made up of 45/45/10 in equities, bonds, and gold, respectively. This portfolio brings down downside volatility to 3.7% relative to the original 50/50 stock-bond portfolio (3.9%). Allocating more than 20 percent to gold leads to higher risk and lower return portfolios which are clearly inefficient.

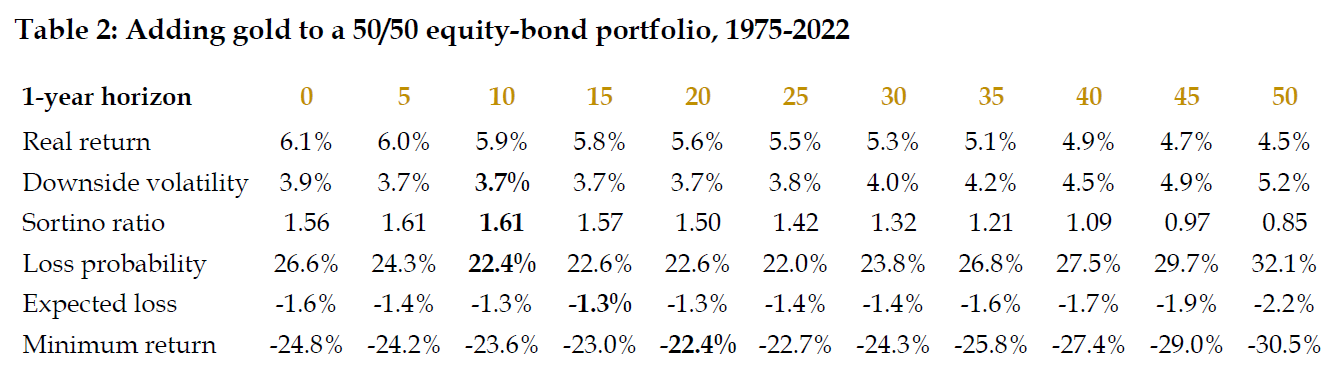

Table 2 shows the return, the three lower partial moments, Sortino ratio, as well as the minimum return across the different portfolio combinations (again using inflation as the threshold), where gold is added in 5 percent increments up to 50 percent (replacing the existing balanced mix in each step). Depending on the choice of risk measure, the optimal gold allocation varies between 10 and 20 percent.

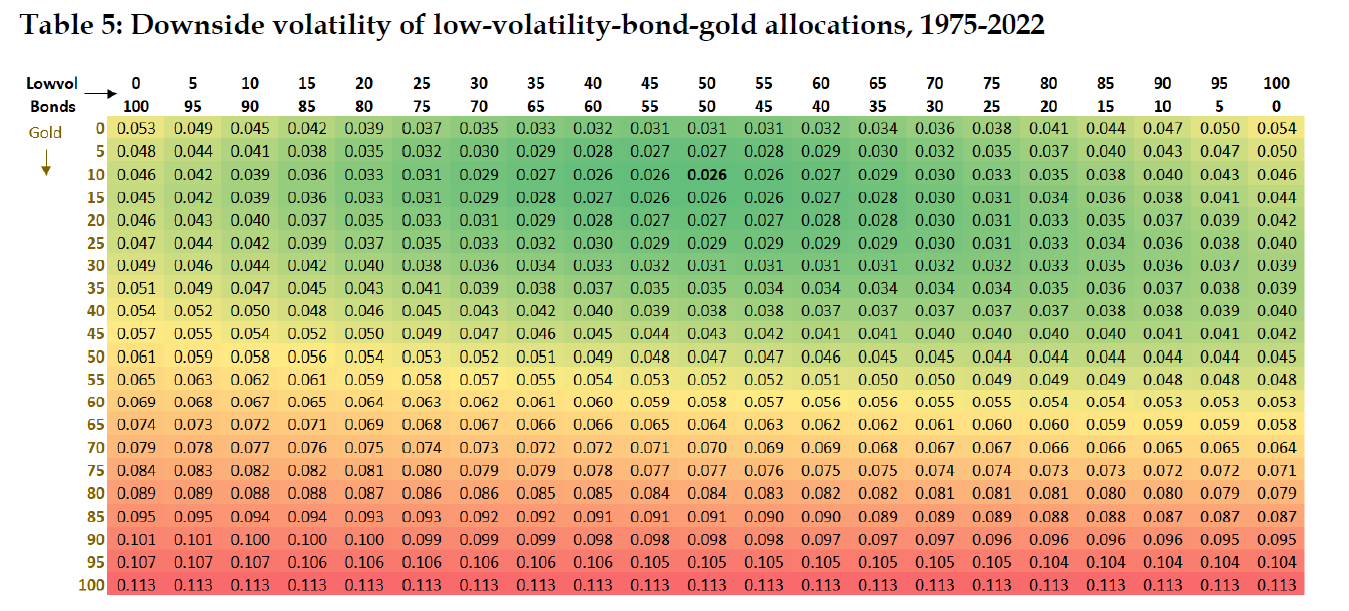

We broaden our quest for a minimum risk portfolio by replacing the equity market with the defensive low-volatility equity style and investigate a wide range of possible combinations of low-volatility stocks, bonds, and gold in Table 5. From a downside risk perspective, there is also a role for gold in the defensive equities and bond mix. A 10% gold allocation leads to the lowest downside volatility for a 50/50 equity-bond portfolio. Black’s (1993) recommendation to allocate more to defensive equities at the expense of bonds is also apparent from Table 5, with the greenest area of optimal downside volatility shifting to the right relative to Table 3. The lowest downside volatility in Table 3 is 3.3% for a 30/70 equity-bond allocation together with 10 percent gold. This downside volatility can be further reduced to 2.6%, with a higher allocation to low-volatility stocks and a lower allocation to bonds. The defensive multi-asset portfolio thus consists of a 45/45/10 allocation to bonds, low-volatility stocks and gold, respectively.“

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend