The Attention Factor: The Link That Connects Crypto and Public Equity Markets

In an era of increasingly fragmented market microstructure, the emergence of cross-asset connectedness between Crypto and public equity markets presents a critical challenge for modern portfolio construction. This blog post examines the recent working paper by Harin de Silva, “The Attention Factor: The Speculative Risk You May Already Own,” which identifies a previously underappreciated transmission channel: a speculative cohort of marginal investors whose sentiment shifts propagate correlated price movements across BTC, zero-day-to-expiration (0DTE) options, commission-free brokerages, and social-sentiment-driven equities. The author introduces the Attention factor—a capital-backed measure of collective conviction—as a systematic risk driver that persists after controlling for traditional macro factors, fundamentally reshaping how we model Equity Risk in multi-asset portfolios. For quantitative practitioners, this work underscores the need to augment conventional Risk Models with sentiment-aware factors to capture residual connectedness that standard factor frameworks may overlook.

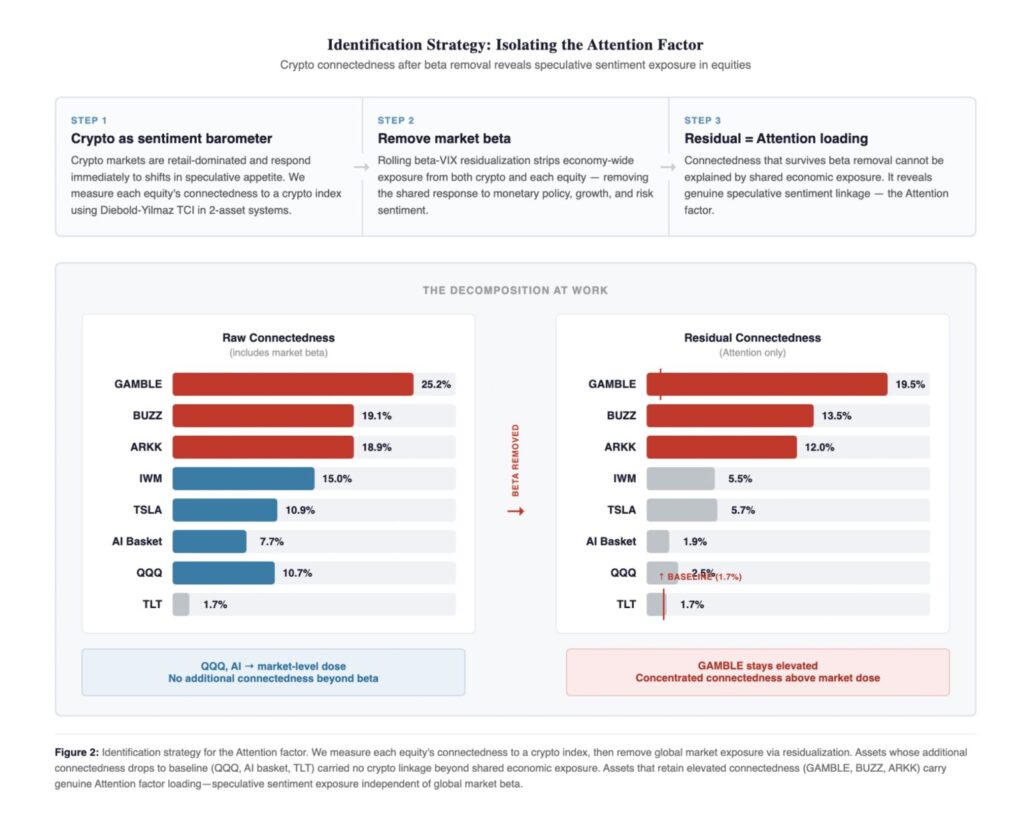

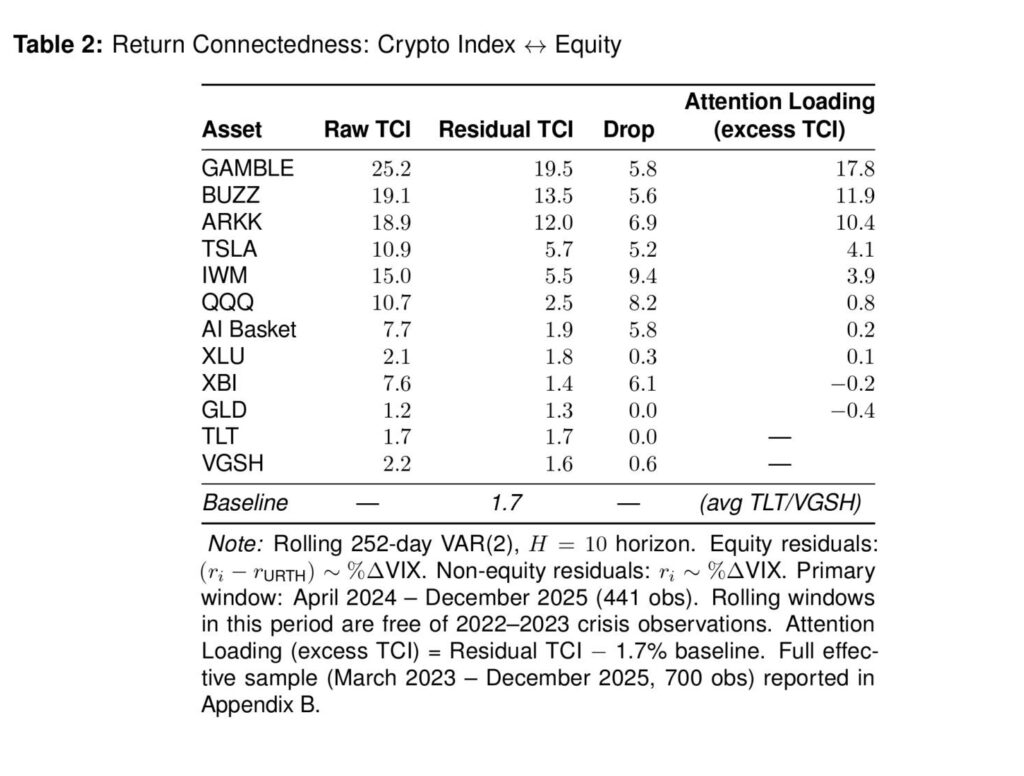

The paper’s central empirical contribution lies in decomposing crypto-equity co-movement into systematic and residual components. After regressing Bitcoin returns on global equity market returns and risk appetite proxies, a statistically significant residual connectedness remains—particularly for equities with revenue exposure to speculative participation (e.g., Coinbase, Robinhood, DraftKings) and for sentiment-harvesting vehicles like the BUZZ Social Sentiment ETF. This residual is interpreted as the Attention factor’s footprint, transmitted via overlapping investor bases rather than fundamental linkages. TCI (Trading Concentration Index) metrics further reveal that periods of elevated retail order-flow concentration coincide with spikes in cross-asset correlations, suggesting that liquidity-provision dynamics amplify the Attention factor’s impact. Crucially, institutionally dominated benchmarks such as the Nasdaq-100 exhibit minimal residual connectedness, implying that the factor’s influence is heterogeneous across the equity spectrum and concentrated in segments with high retail participation.

The findings advocate a spectrum-based assessment of speculative-sentiment exposure rather than a binary “crypto yes/no” allocation decision. Every equity portfolio inherently carries some market-level Attention factor exposure, given Bitcoin’s broad co-movement with global equities during periods of high speculation. However, thematic growth funds, small-cap indices, and social-media-driven strategies exhibit amplified sensitivity, potentially introducing unintended concentration risk. Integrating Attention-factor loadings into multi-factor Risk Models enables allocators to quantify this hidden beta and adjust position sizing or hedging overlays accordingly. The framework also offers a diagnostic tool for stress-testing portfolios against sentiment-driven regime shifts—a capability that is increasingly vital as 0DTE option volumes and crypto derivatives markets continue to expand the footprint of speculative capital.

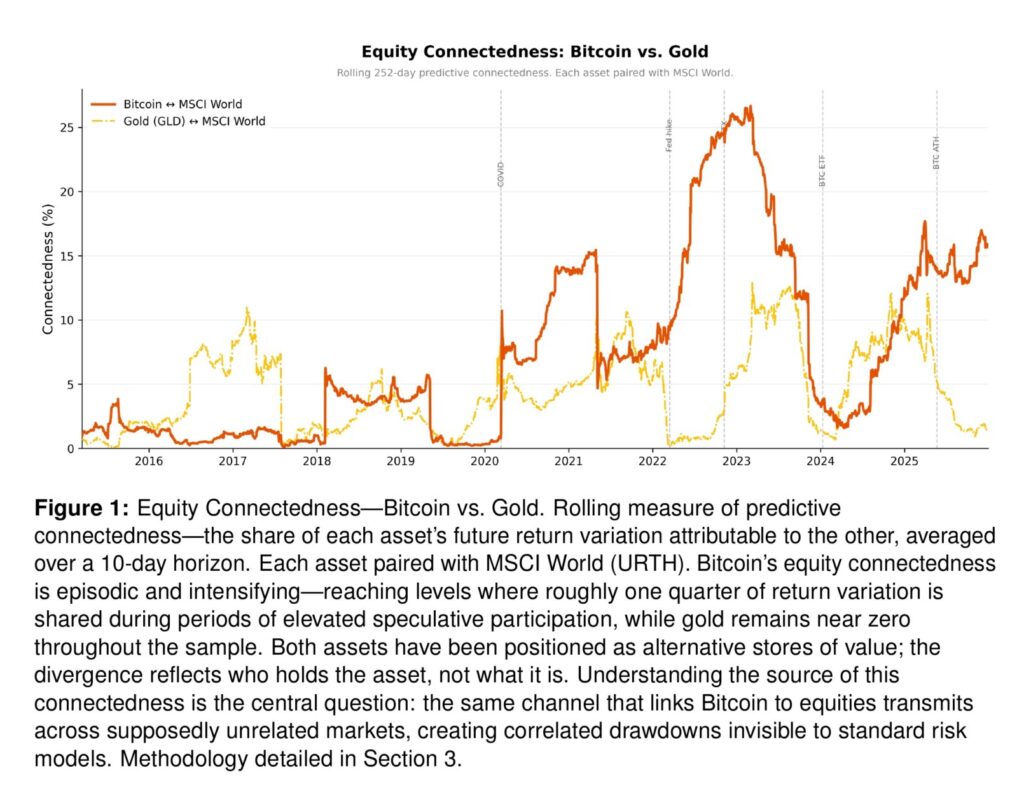

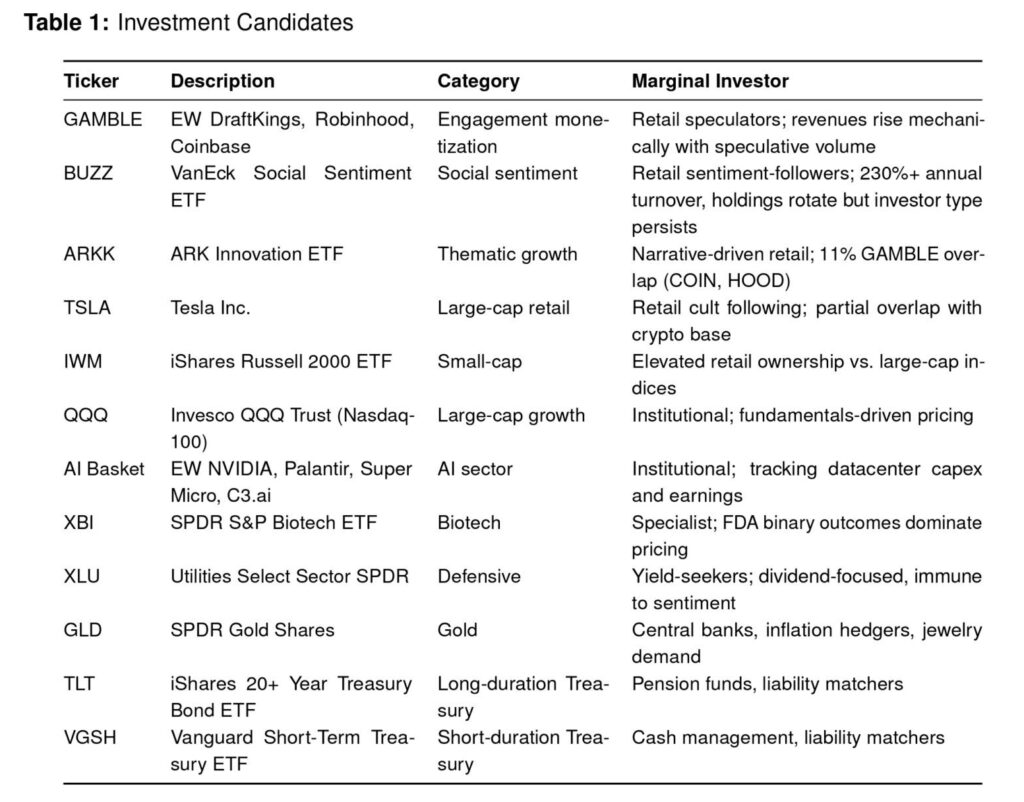

Regarding the paper’s visual evidence: Figure 1 plots the rolling 90-day correlation between Bitcoin and MSCI World Equities, highlighting episodic spikes that align with surges in retail trading activity and social media sentiment metrics—visually confirming the linkage’s non-stationary, regime-dependent nature. Table 1 presents regression results that decompose Bitcoin’s return variance, showing that approximately 25% is explained by global equity returns during periods of high speculation, whereas gold has near-zero explanatory power, underscoring crypto’s unique role as a sentiment signal. Figure 2 maps residual connectedness (post-systematic factor adjustment) across a cross-section of equities and ETFs, with speculative-exposure names clustering in the upper-right quadrant, while institutional benchmarks remain near the origin. Table 2 reports factor loadings for the constructed Attention factor across style buckets, confirming statistically significant exposures for small-cap, high-beta, and social-sentiment strategies, while value and low-volatility portfolios show negligible loadings—providing actionable inputs for factor-tilted portfolio construction.

Authors: Harin de Silva

Title: The Attention Factor: The Speculative Risk You May Already Own

Link: https://ssrn.com/abstract=6277718

Abstract:

Cryptocurrency and equity markets have become linked-and the linkage is intensifying. Bitcoin now shares roughly a quarter of its return variation with world equities during periods of elevated speculative participation, while gold shares near zero. An asset with no shared business fundamentals-cash flows, earnings, or production linkages has developed meaningful co-movement with equity markets. For allocators, understanding this linkage is not a crypto question-it is a portfolio risk question. We therefore test whether the linkage is entirely explained by shared exposure to economy-wide conditions-global market returns and risk appetite shifts. It is not. After removing these systematic channels, a residual connectedness survives-but not uniformly. The residual is largest for firms whose revenues depend mechanically on speculative participation (DraftKings, Robinhood, Coinbase) and for sentiment-driven strategies (BUZZ Social Sentiment ETF). For institutionally priced benchmarks like the Nasdaq-100 and AI stocks, residual connectedness drops to the level explained by shared market exposure alone-despite their popularity. This pattern suggests a common cause. Our hypothesis: the linkage transmits through shared marginal investors. A speculative cohort-retail traders active across crypto exchanges, zero-day options, sports betting, and commission-free brokerages-sets prices in multiple markets simultaneously. When this cohort’s sentiment shifts, it creates correlated movements across every venue they participate in. Crypto, having no fundamental equity linkage, serves as the cleanest signal of this transmission. We interpret this transmission as an Attention factor-capital-backed collective conviction expressed by a speculative cohort active across multiple markets. The key finding is not binary. Every equity investor carries some speculative sentiment exposure through the market itself-crypto co-moves with world equities broadly, meaning this channel is already embedded in market returns. What varies is how much additional connectedness specific equities carry beyond this market-level dose. Thematic growth funds, small-cap indices, and social-sentiment strategies concentrate it. The relevant question for allocators is not whether to add crypto, but how much speculative sentiment exposure already exists in the portfolio-and where on the spectrum their holdings sit.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Figure 1 tells a different story. Bitcoin’s connectedness to world equities is episodic and intensifying; returns to Bitcoin are uncorrelated with this connectedness. During periods of elevated speculative participation—the 2020–2021 and 2024–2025 episodes—roughly a quarter of Bitcoin’s near-term return variation is shared with MSCI World. When participation cools, the linkage collapses. Gold rarely exceeds 5%.

This paper makes five contributions. First, we document that crypto-equity connectedness exists beyond shared market exposure and risk appetite channels—a finding that is itself empirically novel for a fifteen-year-old asset class with no fundamental equity linkage (Section 5). Second, we show that the residual connectedness varies systematically across equities, mapping onto marginal investor composition rather than sector, popularity, or volatility (Section 5.1). Third, we provide independent validation through BUZZ (VanEck Social Sentiment ETF): despite 230% annual turnover and completely different construction methodology, BUZZ exhibits persistent residual connectedness—the holdings rotate but the loading endures, illustrating that the factor tracks investor type rather than specific holdings. Fourth, we demonstrate that the transmission operates primarily through returns rather than volatility—consistent with sentiment transmission rather than balance sheet contagion (Section 7). Fifth, we validate the speculative participation mechanism directly: detrended zero-day-to-expiration options volume co-moves with crypto-equity connectedness (r = 0.30, p < 0.001), confirming that the same cohort driving 0DTE activity drives the Attention factor (Section 5.3).

Table 1 summarizes the assets tested for Attention exposure. The final column—marginal investor— is the key predictor of Attention loading. The results in Section 5 bear this out: assets whose prices are set by retail speculators show elevated residual crypto connectedness; assets priced by institutions show no additional connectedness beyond the market-level dose, regardless of popularity.

Every equity investor carries some speculative exposure through the market itself. What varies is how much additional exposure specific holdings add. Standard factor models—market, size, value, momentum, quality—do not capture this channel. The Attention spectrum reveals hidden co-movement and correlated drawdown risk that conventional decompositions miss: when speculative sentiment reverses, high-Attention assets decline together, and together with crypto, through a channel invisible to standard risk attribution. What ultimately matters is not whether a portfolio holds crypto, but whether it holds the marginal investor—and whether that exposure is intentional.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend