Commodity Futures Predict Stock Market Returns

Commodities are an essential exporting asset for a lot of countries around the world. Therefore, it is not surprising that the stock market returns of some emerging market countries are dependent on the returns of those commodities. What is more striking is that commodities do not forecast equity returns for only those few small exporting countries. Academic research paper written by Alves & Szymanowska shows that commodity futures returns predict stock market returns in 65 out of 70 countries and macroeconomic fundamentals in 62 countries. That is looking like an idea worth dig into …

Authors: Alves, Szymanowska

Title: The Information Content of Commodity Futures Markets

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3352822

Abstract:

We find that commodity futures returns contain information relevant to stock market returns and macroeconomic fundamentals for a large number of countries. Commodity futures returns predict stock market returns in 65 out of 70 countries and macroeconomic fundamentals in 62 countries. This predictability is not concentrated in the energy and industrial metals sectors, as it is economically and statistically significant across all sectors. Surprisingly, we find that the role of countries’ dependence on commodity trade is limited in its ability to account for this predictability. This holds true even when considering new measures that take into account indirect exposures through financial and trade linkages between countries. We find much stronger evidence of predictability being related to the ability of commodities to forecast inflation rates. Overall, our evidence is consistent with commodity markets having a truly global information discovery role in relation to financial markets and the real economy.

Notable quotations from the academic research paper:

“We study the information content of commodity futures returns with respect to stock market returns around the world, using an extensive dataset covering 70 countries and six commodity sectors over the course of a sample period between 1979 and 2016. To the best of our knowledge, we are the first to show that the information flow from commodity to stock markets is a pervasive global phenomenon and that the information content of commodity sector returns extends well beyond countries’ dependence on commodity trade. Overall, our findings are consistent with the idea that commodity markets play an important role in aggregating dispersed global information.

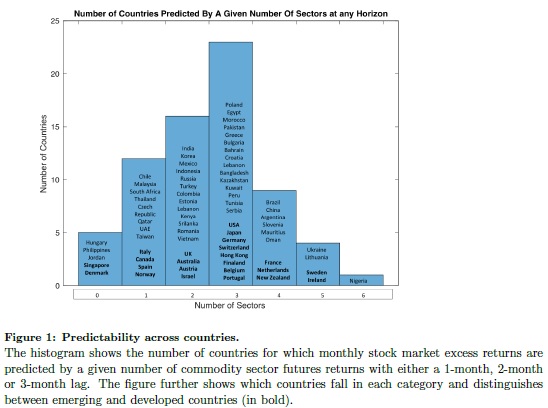

We find that in 65 of the 70 countries in our sample, country stock market returns are predicted by the past commodity futures returns of at least one commodity sector. The majority of those stock market returns are, in fact, predicted by two to four commodity sectors. This is true for both emerging markets and developed countries. Furthermore, all commodity sectors predict a wide range of countries in our sample. The Energy, Industrial Metals, and Livestock & Meats sectors predict the highest percentage of countries, ranging between 43% and 54% of all the countries in our sample, while the Precious Metals and Agriculture sectors predict around 35%. These results remain robust even when controlling for known stock market predictors. Hence, from a statistical signi cance standpoint, all sectors contain information that is relevant to stock markets around the world.

However, it is not only that commodity markets predict stock markets in many countries, it is also that the economic magnitude of this predictability is large and, for most countries, several commodity sectors contain important economic information that is not subsumed by the others. In fact, when looking within each country, we fi nd that that there are few countries for which the economic magnitude of predictability is dominated by a single sector. This is surprising given that many countries are disproportionately more dependent on trade in some commodity sectors than in others. We also show that the economic magnitude of predictability is not concentrated in the largest economies; rather it is spread evenly across the globe.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend