Comparison of Commodity Momentum Strategy in the U.S. and Chinese Markets

The commodity momentum strategy is a crucial driving force behind Commodity Trading Advisor (CTA) strategies, as it capitalizes on the persistence of price trends in various commodity markets. By identifying and exploiting these trends, CTAs can achieve robust returns and diversification benefits.

In their new paper, John Hua FAN and Xiao QIAO (February 2023) present their perspective and understanding of cross–country and cross–sector influences on the behavior of commodity momentum beyond established commodity fundamentals focusing on U.S. and China markets. Pretty inspiring is their unique approach in matching variation in the average returns of commodity futures through a link to momentum profits with sector returns.

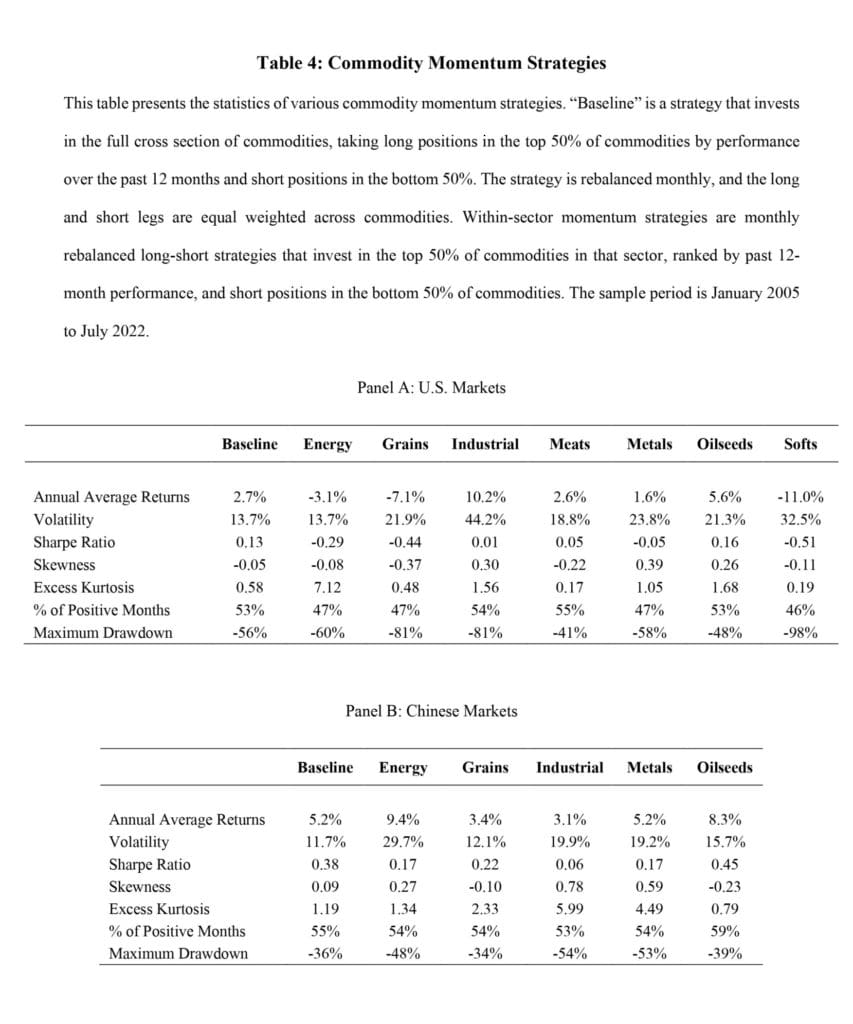

Commodity momentum strategies in the U.S. and China show some return co-movement, still, sources of their premia are primarily local. The main listed suspected fundamental reasons presented as possible explanations and further discussed include cross-broader cash-and-carry arbitrage, as well as substantial differences in market participants and sensitivity to global inflation shocks. Around the world, sector momentum was found to explain much of the average returns to commodity momentum strategies.

While Bayesian analysis (look into thoughtful Online Appendix in paper) still favors the profitability of commodity strategies in States, one cannot debate the mediocre performance of U.S. momentum strategies in the past decade. Standard risk factor models are puzzled by individual commodity effects, which are the main vehicle contributor to the overall profitability of momentum strategies in China, but are much weaker in the U.S. markets. Once more, for astute readers, tables 5 and onwards provide an easy-digestible and comprehensive overview of all researched variants of commodities, factors, and sectors.

Authors: John Hua Fan and Xiao Qiao

Title: Commodity Momentum: A Tale of Countries and Sectors

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4357642

Abstract:

This paper takes a cross-country and cross-sector perspective to investigate the drivers of commodity momentum strategies. Commodity momentum strategies deployed in the U.S. and Chinese markets generate positive average returns with non-negligible correlations, but their premia are primarily local, and their return characteristics are distinct. A prevalent sector effect explains a significant fraction of momentum profits in both markets, suggesting that long-short commodity futures momentum may be riskier than previously thought. Overall, our findings suggest commodity momentum is more consistent with a risk-based explanation in U.S. markets whereas risk alone is difficult to capture the premia in China.

And as always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“[T]wo key findings[:] Our first finding points to the local nature of commodity momentum returns. While baseline momentum strategies earn positive average returns in the U.S. and Chinese markets of 2.7% and 5.2% per year, their correlation is merely 0.34. In a series of tests, we first show that spanning regressions of the Chinese strategy on the U.S. strategy (and vice versa) report economically large intercepts of 4.8% (1.2%). We then introduce a set of global factors including two global momentum strategies constructed from commodity contracts in both countries and macro factors including foreign exchange rates, global value, momentum, and carry strategies across asset classes and geographies, and find that global strategies can indeed explain the average returns associated with baseline strategies in both markets. However, we find that the U.S. commodity momentum is exposed to global inflation but the same does not hold in China. In an overlapping sample of 12 commodities traded in both the U.S. and China, we find that domestic strategies earn annual average returns of 5.0% and 3.3% respectively but continue to have a relatively low correlation of 0.43. A strategy that takes U.S. (Chinese) signals to invest in Chinese (U.S.) markets earns an annual average return of 4.5% (8.1%). The fact that cross-country signals on average perform better than domestic signals suggests that past returns in foreign markets may convey information content beyond domestic market dynamics.

Our second key finding relates to commodity sector effects. Because commodity futures returns within a sector tend to be much more correlated than across sectors, momentum strategies can have large sector tilts and therefore are not well-diversified. If sector effects dominate, commodity momentum is exposed to sector concentration risk, favoring a risk-based explanation of its average returns. On the contrary, if commodity momentum were primarily driven by behavioral biases, then rational investors can earn a high Sharpe ratio with diversified positions across commodities (Moskowitz and Grinblatt, 1999).3 Indeed, a series of tests show that sector momentum explains a significant fraction of commodity momentum profits.

Our sector analysis relates to the recent work of Kang et al. (2021), who demonstrate that “crowding” effects, proxied by excess speculative pressure, can explain the recent poor performance of momentum strategies in U.S. commodity markets. Our findings suggest that the recent underperformance is due largely to sector effects rather than individual commodity effects. Since commodity momentum strategies require concentrated bets in sectors, our finding suggests a higher degree of crowding effects may be present in sectors traded by commodity momentum strategies. Moreover, our paper relates to studies linking momentum returns to sector effects. Moskowitz and Grinblatt (1999) demonstrate that industry momentum drives much of equity momentum strategies, which become significantly less profitable after controlling for industry momentum. Szymanowska et al. (2014) argue that cross-sectional and time-series variation in commodity futures returns is related not so much to sectors as to characteristics such as momentum. We find that in commodity futures markets, sector momentum contributes towards explaining the cross-sectional variation in average returns.

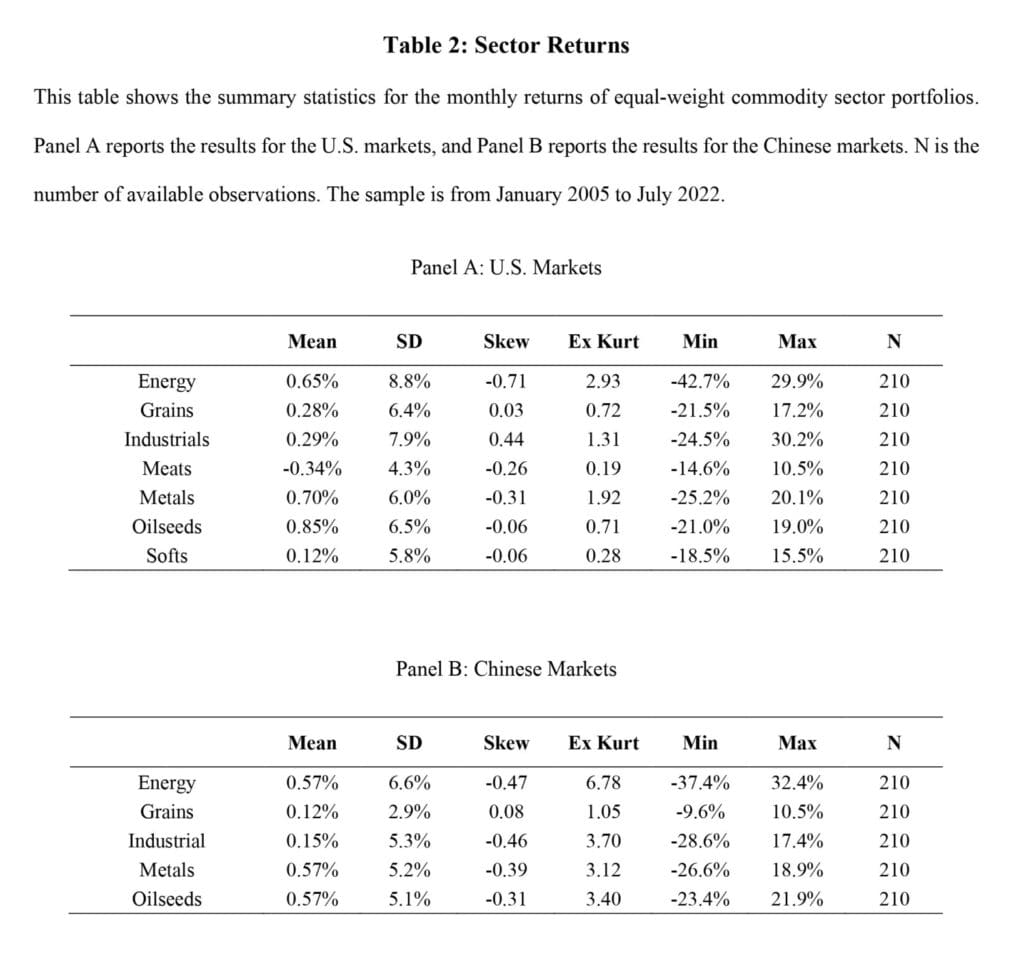

We construct monthly rebalanced equal-weight portfolios for each commodity sector. Table 2 presents the summary statistics for the equal-weight sector returns. For the U.S. markets, six of the seven sectors have positive average returns in our sample, ranging between 0.12% to 0.85% per month. Meats is the only sector that shows negative average returns, at -0.34% per month. For the Chinese markets, all five sectors have positive average returns, ranging between 0.12% to 0.57% per month. For both the U.S. and Chinese markets, commodity sector returns tend to be negatively skewed and leptokurtic.

Table 3 presents pairwise correlations of equal-weight sector returns. Pearson correlation coefficients, computed as the covariance between two variables divided by the product of their standard deviations, are shown in each cell. For comparison, Spearman’s rank correlation coefficients, calculated as the Pearson correlation between the ranked variables, are shown in square brackets. For the U.S. markets, 20 of 21 Pearson correlations are positive, with values between 0.02 to 0.71. Only one Pearson correlations is negative at -0.08. 19 of 21 Spearman’s rank correlations are positive, with values similar to those of the Pearson correlations. The two measures show opposite signs (0.02 and -0.04) for the correlation between meats and oilseeds, highlighting the weak relation between these two sectors.

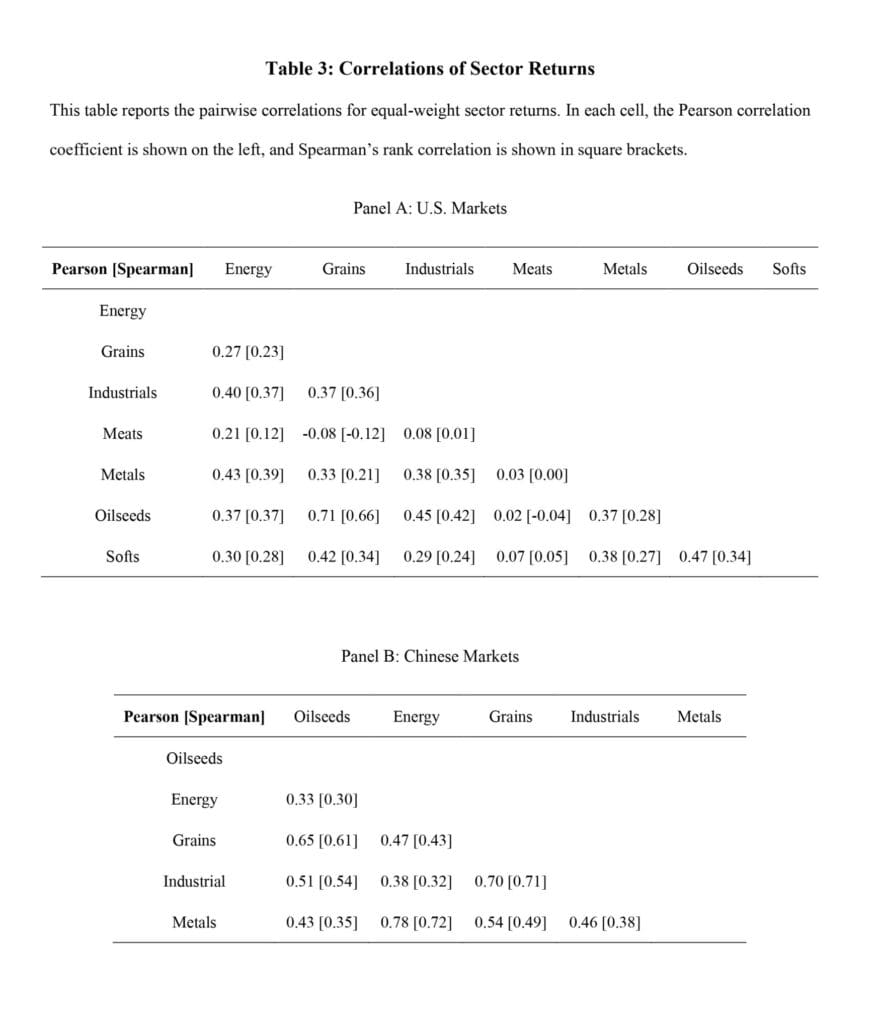

The rank-based momentum returns are highly correlated with the returns from portfolio sorts. The portfolio returns from the two methods have a correlation of 0.92 for the U.S. markets and 0.96 for the Chinese markets. Figure 3 plots the rank-based momentum returns, along with the sector and idiosyncratic components. For ease of viewing, the returns are smoothed using a 12- month window. There exists significant time variation in momentum profits. Years preceding to the Great Recession saw great returns for both the U.S. and Chinese strategies, and both strategies suffered drawdowns during the Great Recession. The drawdown in the U.S. markets was less severe and lasted for a shorter period, as sector and idiosyncratic components offset one another. Around the same time in the Chinese markets, both the sector and idiosyncratic components contributed negatively to a deeper drawdown. The recent underperformance in the U.S. markets can be largely attributed to a large negative sector component. In terms of economic magnitude, the rank-based method shows average returns of 2.1% for the U.S. and 8.4% for China. 99% of momentum profits in the U.S. can be attributed to the sector component. In the Chinese markets, the split is 51% and 49% for the sector and idiosyncratic components, respectively.

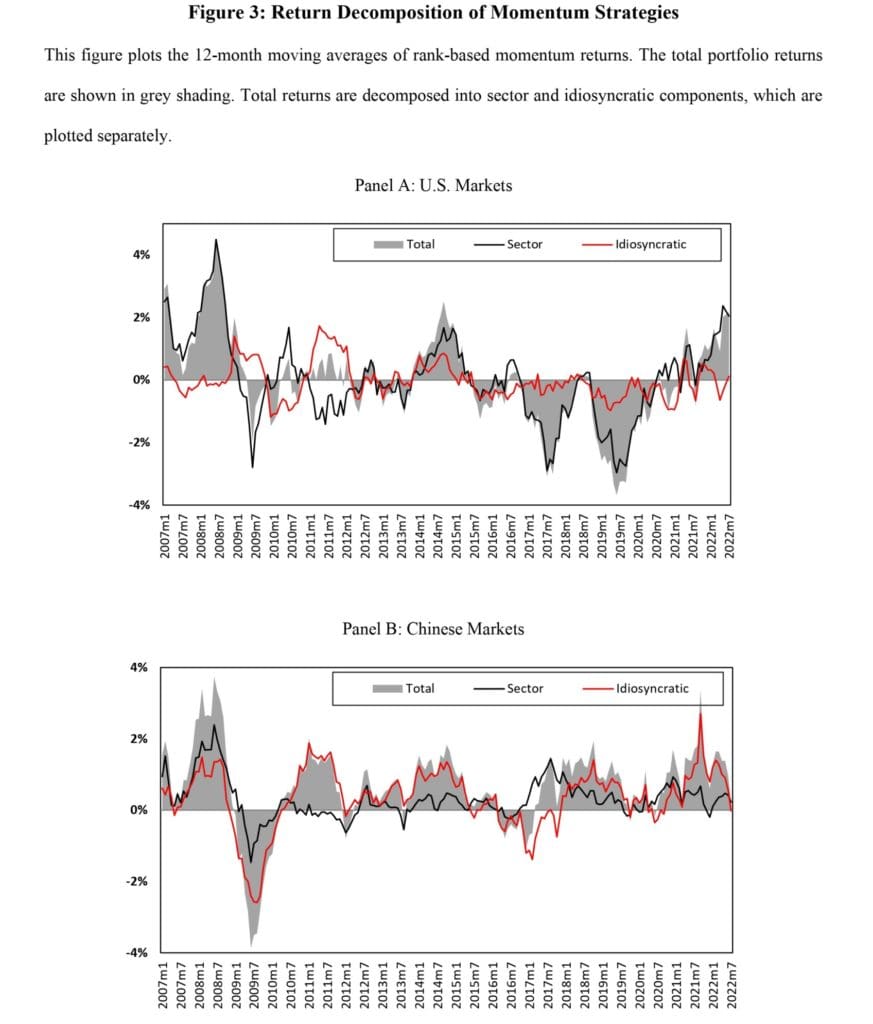

We further investigate the comovement of within-sector momentum strategies by examining the left tail of these return distributions. Figure 4 compare the drawdowns of sector returns and within-sector momentum strategies in the Chinese markets. Panel A illustrates that drawdowns tend to occur at the same time across several sectors: energy, industrials, metal, and oilseeds all simultaneously suffered a sharp drawdown in 2009. Although its magnitude was less dramatic, the grains sector also experienced a smaller drawdown at the same time as the other sectors. From 2015 to 2017, all five sectors had continuous losses. Because sector-level drawdowns tend to happen at the same time, an equal-weight portfolio of sector returns cannot alleviate this tail risk – an equal-weight sector portfolio shows a maximum drawdown of 46.3%. This equal-weight portfolio experienced a prolonged period of underperformance, from 2008 to 2020, as individual sectors perform persistently poorly.

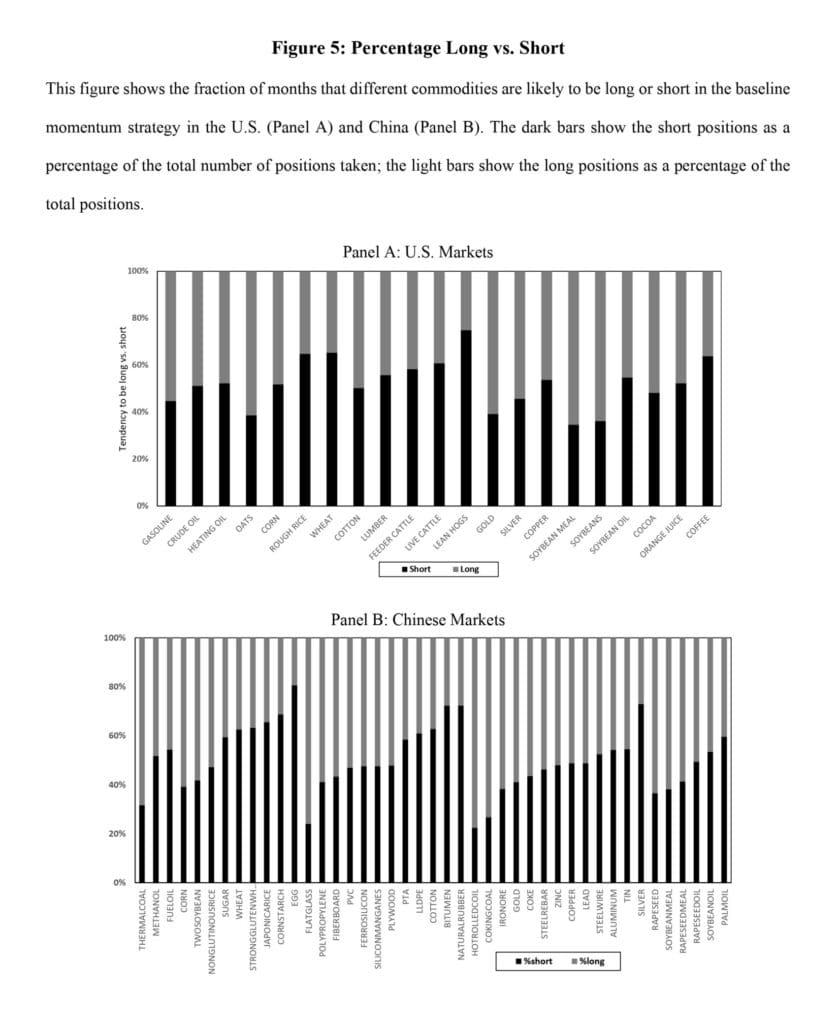

As a further test of the importance of individual commodity effects in the U.S. and Chinese markets, we examine the long and short positions for the baseline momentum strategies. If individual commodity effects drive the overall profits of commodity momentum strategies, we may expect to observe concentrated positions in specific commodities. Figure 5 shows the fraction of time each commodity is long or short. For both the U.S. and China, most commodities are traded both in the long and short portfolios, and the fraction of longs and shorts appear balanced. The baseline momentum strategies do not take many extreme positions, suggesting momentum profits are spread across sectors rather than concentrated in individual commodities. However, there are some exceptions in the Chinese markets. The baseline strategy in the Chinese markets exhibit more unbalanced positions across commodities, indicating stronger influence of individual commodity effects for the overall momentum profits.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend