Cross-Sectional and Dollar Components of Currency Risk Premia

Currency strategies often appear simple on the surface – go long high-yielding currencies, short low-yielding ones, or take a position on the U.S. dollar. But these trades actually mix two distinct components: a Dollar component, which bets on broad movements of the U.S. dollar against all others, and a Cross-Sectional (CS) component, which exploits relative differences across countries. The question is, which of these components really drives currency risk premia? A new paper by Vahid Rostamkhani tackles this long-standing question by decomposing the predictive power of eleven macroeconomic fundamentals—such as interest rates, inflation, unemployment, and fiscal variables—into these two components across almost a century of data (1926-2023). This approach directly tests whether it is more rewarding to time the dollar itself or to focus on cross-country fundamental spreads.

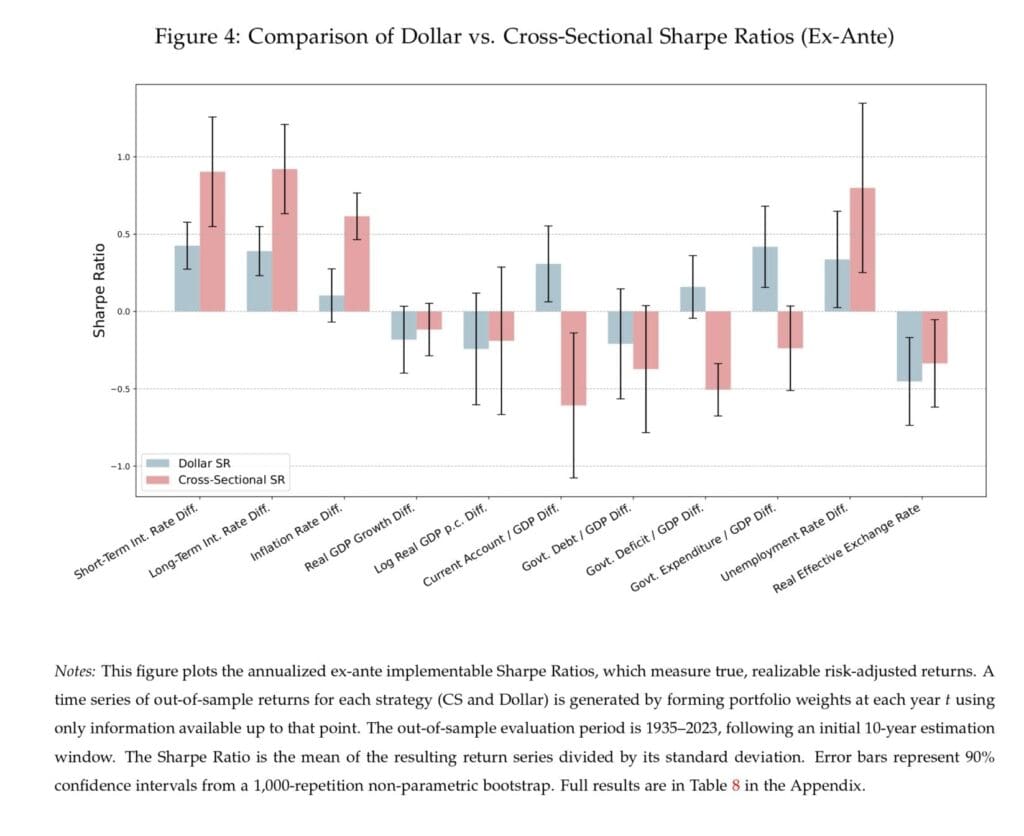

For practitioners running currency carry, value, or macro-fundamental strategies, this distinction is critical. A strategy dominated by the Dollar component is effectively a bet on the global financial cycle and the dollar’s safe-haven status—exposed to regime shifts in U.S. monetary policy and risk-off episodes. In contrast, CS-driven strategies isolate relative country risk premia and may offer better diversification. Rostamkhani’s results show that cross-sectional predictability is consistently stronger, delivering higher and more robust risk-adjusted returns (Sharpe ratios) than strategies that attempt to time the broad dollar.

To handle the “factor zoo” of 22 Dollar and CS signals, the paper applies a Bayesian Model-Averaged Stochastic Discount Factor (BMA-SDF) framework. The analysis finds that currency pricing is dense, not sparse: no single macro factor dominates, but many provide noisy pieces of valuable information about underlying risks. By optimally aggregating them, the BMA-SDF achieves much better out-of-sample pricing power than traditional two-factor models. For portfolio managers, this suggests that instead of seeking a single perfect macro predictor, combining a broad set of relative-fundamental signals—and emphasizing the cross-sectional side—may capture more of the available currency risk premium.

Key Findings

-

The paper decomposes currency strategies into Dollar vs. Cross-Sectional (CS) components across 11 macro fundamentals over 1926-2023.

-

CS strategies consistently outperform Dollar strategies in both in-sample and out-of-sample Sharpe ratios (e.g., CS SR ≈ 0.88 vs 0.43 for short-term interest-rate differentials).

-

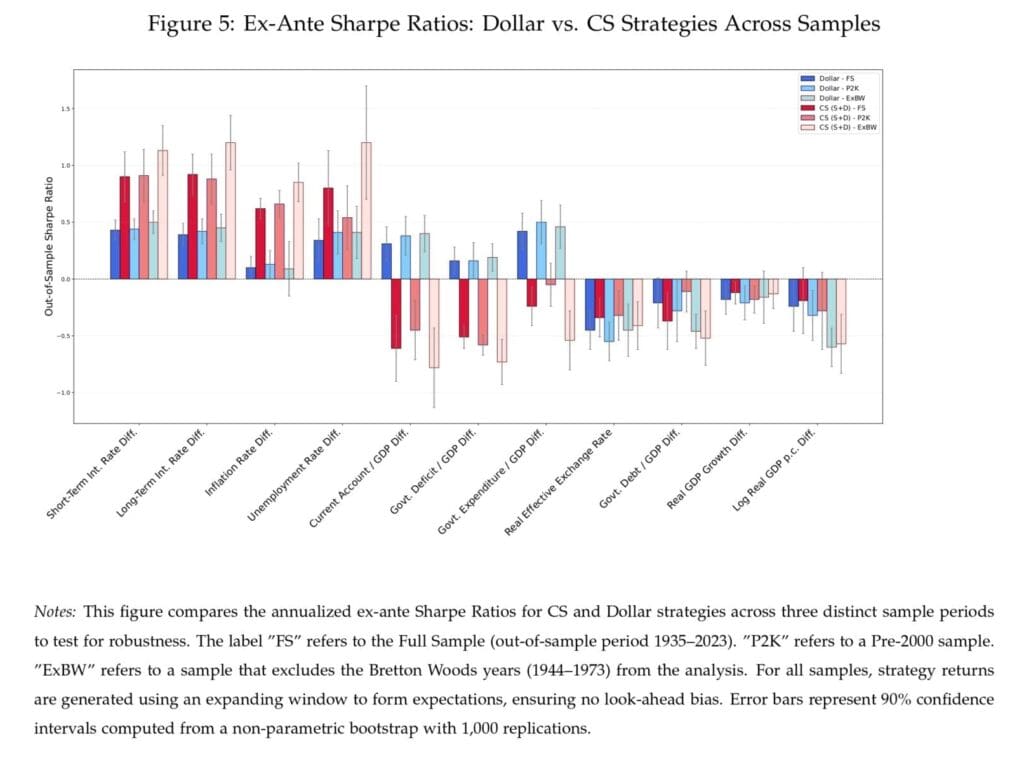

CS predictability is especially strong for interest-rate, inflation, current-account, and unemployment differentials and remains robust across sub-periods (pre-euro, post-Bretton Woods).

-

Currency pricing is “dense” – many fundamentals matter jointly; no single factor explains risk premia alone.

-

A Bayesian Model-Averaged SDF that aggregates all 22 factors achieves an implied Sharpe ratio of ~1.4, far exceeding the traditional two-factor Dollar + Carry model (~0.37).

-

Results highlight that diversified, cross-sectional fundamental signals provide a more stable source of currency risk premia than timing the U.S. dollar.

Authors: Vahid Rostamkhani

Title: Currency Risk Premia and (Many) Fundamentals Connected in the Long-run

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5349012

Abstract:

I study the macroeconomic foundations of currency risk premia using a unique annual dataset spanning nearly a century (1926-2023). First, for a broad set of macroeconomic fundamentals, I decompose the predictability of currency excess returns into two channels: a cross-sectional (CS) component that exploits relative differences across countries, and a Dollar component that times aggregate movements against the U.S. dollar. I find that strategies based on CS predictability generally yield higher and more robust risk-adjusted returns, both in-sample and out-of-sample. Second, to handle the resulting factor zoo of 22 CS and Dollar factor proxies, I employ a robust Bayesian asset pricing framework. I find that the currency Stochastic Discount Factor (SDF) is dense; no single factor dominates, but rather many fundamentals contribute noisy information about a smaller set of latent risks. Finally, I show that a Bayesian Model Averaged (BMA) SDF, which optimally aggregates information across all factors, achieves out-of-sample pricing performance compared to more parsimonious benchmark models.

As always, we present several interesting figures and tables:

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend