Determinants of Emerging Market Bonds Returns

Do you invest in emerging market bonds? A new interesting academic research paper just for you:

Author: Kang, So, Tziortziotis

Title: Embedded Betas and Better Bets: Factor Investing in Emerging Market Bonds

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3196018

Abstract:

We document novel empirical insights driving the prices of sovereign external emerging market bonds. In the time series, we examine the market portfolio’s time-varying exposures to a broad set of macro factors (rates, credit, currency, and equity) and identify these embedded betas as key drivers of its excess returns. In the cross-section, we construct complementary value and momentum style factors and demonstrate their ability to explain country expected returns. Building off these insights, we introduce a simple risk-on versus risk-off framework to characterize the correlation structure spanning our macro and style factors. Lastly, we show how our style factors can be incorporated in an optimized long-only portfolio to generate outperformance relative to a value-weighted benchmark portfolio.

Notable quotations from the academic research paper:

"Our paper attempts to answer several salient questions:

What broad insights can macro factors provide into the time series of returns?

What country-specific insights can style factors provide into the cross-section of expected returns?

How can a factor-based investor systematically leverage these insights?

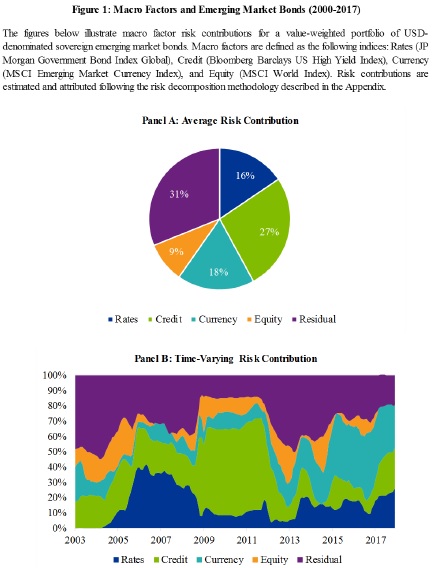

To motivate our paper, we begin by illustrating how macro factors have been a significant source of time-varying risk in the EMB universe. The top panel of Figure 1 decomposes the total risk of a value-weighted EMB portfolio between 2000 and 2017 in terms of macro risk factors. As expected, interest rate and credit risk factors appear to be the primary sources of risk, with relative risk contributions of 16% and 27%, respectively.2 While the EMB universe only includes USD denominated bonds with no explicit exposure to exchange rate fluctuations or global equity markets, our EM currency and global equity factors surprisingly account for 18% and 9% of the portfolio’s risk, respectively. Moreover, the bottom panel of Figure 1 reveals that these relative risk contributions have not been static, but in fact varied significantly over time.

Given these observations, our empirical analysis begins with an examination of the time series relationship between macro factors and EMB returns. We first highlight the impressive performance of the EMB portfolio, which realized an annualized excess return of 7.5% with a volatility of 9.0% over this sample period, corresponding to a Sharpe Ratio of 0.83. After controlling for its macro factor exposures, however, we find that the EMB portfolio realized no significant outperformance. We then examine the EMB portfolio’s macro factor exposures, which we call embedded betas, finding the relative risk contributions from these macro factors to be well balanced on average.

Next, we investigate the ability of value and momentum style factors to explain the cross section of country expected returns. We find that our risk-seeking value factor serves as an important source of risk-adjusted returns, while our momentum factor provides valuable defensive protection. We construct our value factor based on a measure we call default-adjusted spread, which corresponds to option-adjusted spread adjusted for expected sovereign default risk. On the other hand, our momentum factor exploits a simple cross-asset insight from currency markets to identify challenging sovereign credit conditions. Since a depreciating currency weakens a sovereign issuer’s ability to service its external debt, we argue that negative currency momentum should forecast lower bond prices to the extent that bond markets underreact to movements in the foreign exchange market.

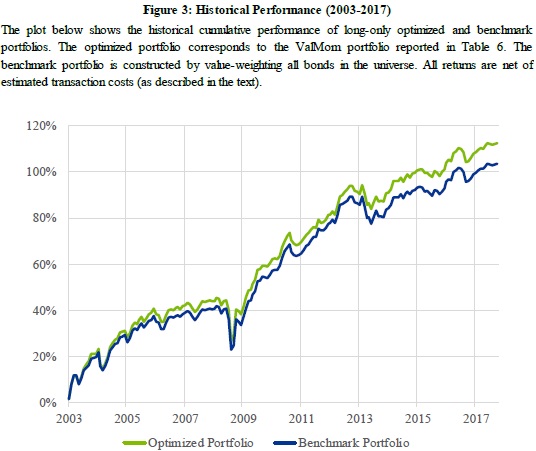

Finally, we empirically test how incorporating our style factors in a long-only portfolio can generate outperformance relative to the value-weighted EMB portfolio through improved country selection bets. We do so by constructing and backtesting optimized long-only portfolios that incorporate realistic benchmark-relative constraints and trading frictions. We find that a multifactor strategy that combines value and momentum insights outperforms its value-weighted benchmark by 60 basis points per annum net of transaction costs, resulting in a net information ratio of 0.82."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend