Does Social Media Sentiment Matter in the Pricing of U.S. Stocks?

Although the models cannot entirely capture the reality, they are essential in the analysis and problem solving, and the same could be said about asset pricing models. These models had a long journey from the CAPM model to the most recent Fama French five-factor model. However, the asset pricing models still rely on fundamentals, and as we see in the practice every day, the financial markets or investors are not always rational, and prices tend to deviate from their fundamental values. Past research has already suggested that the assets are driven by both the fundamentals and sentiment. The novel research of Koeppel (2021) continues in the exploration of the hypothesis mentioned above and connects the sentiment with the factors in Fama’s and French’s methodology. The most interesting result of the research is the construction of the sentiment risk factor based on the direct search-based sentiment indicators. The data are sourced by the MarketPsych that analyze information flowing on social media. For comparison, public news is not a source of such exploitable sentiment indicator.

The sentiment score extracted from social media can be exploited to augment the Fama French five factors model. Based on the results, this addition seems to be justified. Adding the sentiment to the pure fundamental model explains more variation and reduce the alphas (intercepts). Moreover, the factor is unrelated to the well-known and established risk factors utilized in the previous asset pricing models, including the momentum. Finally, the sentiment factor seems to be outperforming several other factors, even those established as the smart beta factors.

Authors: Christian Koeppel

Title: Does Social Media Sentiment Matter in the Pricing of U.S. Stocks?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3771788

Abstract:

This paper applies a recently developed social media-based sentiment proxy for the construction of a new risk factor for sentiment-augmented asset pricing models on U.S. equities. Accounting for endogeneity, autocorrelation and heteroskedasticity in a GMM framework, we find that the inclusion of sentiment significantly improves the performance of the five-factor model from Fama and French (2015, 2017) for di ff erent industry and style portfolios like size, value, profitability, investment. The sentiment risk premium provides the missing component in the behavioral asset pricing theory of Shefrin and Belotti (2008) and (partially) resolves the pricing puzzles of small extreme growth, small extreme investment stocks and small stocks that invest heavily despite low profitability.

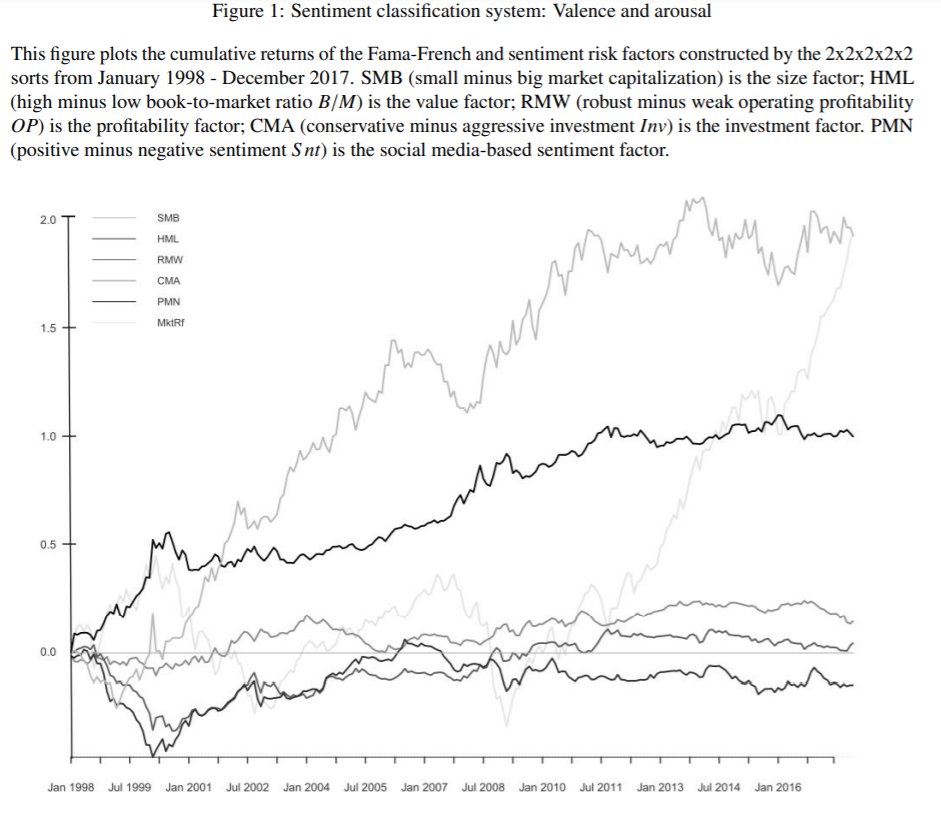

As always the results are best presented through figure:

Notable quotations from the academic research paper:

“Classical models assume that their predictions are the same, whether the price behavior is rational or irrational, and constant over time. Thus, the results show that even the FF5 model only partially describes an asset’s expected return and, in particular, fails for presumably irrational situations. Asset pricing puzzles of hard-to-value stocks, i.e. in explaining average returns of small stocks or companies which invest heavily despite low profitability, remain unsolved. When supply and demand determine

market prices, those firms’ evaluations seem to deviate from their fundamentally explainable values and could be driven by irrational investors. Such behavior cannot be captured by any fundamental pricing model that assumes rational agents in perfect markets. In fact, investors do not necessarily act completely reasonable nor do they only pursue the maximization of their personal utility function. Likewise, they are not even unexceptionally risk-averse. They do not have perfect data nor the unlimited cognitive capabilities to gather, absorb and interpret all information immediately and correctly to derive fully rational and optimal decisions. Neither are the markets strongly efficient nor free of arbitrage as widely assumed by traditional finance. In contrast, behavioral theories consider human biases and market imperfections in the analysis of risk and return, and the decision-making process for investments. In addition to the risk-free rate and a fundamental risk premium, the intrinsic value of an asset is further described by sentiment, forming a joint stochastic discount factor for future cash flows. Due to the lack of other sources, the sentiment risk premium has been often estimated as the dispersion of analyst’s forecasts.

We test Shefrin and Belotti’s hypothesis by constructing a novel sentiment risk factor based on a set of recently developed, direct search-based investor sentiment indicators provided by MarketPsych. This new type of measure is derived from a proprietary human language processing that analyzes asset-specific information as it circulates through social media channels (see, e.g., Chen et al., 2014). This study shows that this indicator

captures and quantifies investors’ sentiment, making it the ideal factor to model the sentiment risk premium in the cross-section of U.S. equity markets.

By using search-based and bottom-up sentiment indicators to construct a new risk factor, we reveal patterns in average returns related to investors’ mood. The sentiment score augments the existing fundamental asset pricing model by Fama and French (2015) for the U.S. equity market and adds the sentiment premium to the pricing paradigm from Shefrin and Belotti (2008). We trace back the significant performance improvements for different factor-mimicking and industry portfolios to investors’ activities in

social media. The same effect is not found exploiting sentiment extracted from public news channels. Different notions of human mood are expressed in social media and can be used to form a monthly-rebalanced sentiment risk factor which is orthogonal to underlying macroeconomic or

business cycle-related developments. It is also unrelated to existing fundamental pricing factors and independent of momentum.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend