ESG Investing in Fixed Income

Corporate bonds and equities of the same firm should share the same fundamentals, but does this preposition hold for the ESG scores and their implications? In the equity market, there is convincing literature that states that ESG scores lower risks or even can improve the performance of portfolios. However, it was shown that the ESG implications could not be universally applied to all countries and their markets. Novel research by Slimane et al. (2020) examines the role of the ESG in the fixed market. The paper shows that the fixed income market is probably some years behind the equity market, but the ESG is also emerging in the fixed income. The performance of ESG outperformers compared to underperformers is continually rising. In Europe, the difference is already economically significant; the rest of the world seems to lag a little. Therefore, the ESG might have a bright future also in the corporate bond market. So far, the results are promising...

Authors: Mohamed Ben Slimane, Eric Brard, Théo Le Guenedal, Thierry Roncalli and Takaya Sekine

Title: ESG Investing in Fixed Income: It’s Time to Cross the Rubicon

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3683477

Abstract:

This research is the companion study of three previous research projects conducted at Amundi that address the issue of ESG (Berg et al., 2014; Bennani et al., 2018; Drei et al., 2019). These studies, which were focused on the stock market, showed that 2014 marks a turning point for ESG screening and the performance of active and passive management in developed equities. Indeed, ESG investing tended to penalize both passive and active investors between 2010 and 2013. Contrastingly, ESG investing has been a source of outperformance since 2014 in Europe and North America. Moreover, it appears that ESG investing and factor investing are increasingly connected. In particular, Bennani et al. (2018) and Drei et al. (2019) concluded that ESG is a new risk factor in the Eurozone.

The case of fixed income is particular since it has been little studied by academics and professionals. It is true that implementing an ESG investment policy in the bond market is less obvious than in the stock market. For example, in the case of sovereign bonds using ESG filters may dramatically change the profile of the bond portfolio, particularly in terms of liquidity. In fact, it seems that ESG investors pursue two different goals when they consider equities and bonds. They invest in stocks with good ESG ratings in order to avoid extra-financial longterm risks, whereas they consider that fixed income is the field of impact investing. This explains the high demand for green and social bonds, and this also explains why ESG screening is less widely implemented in fixed income markets than in equity markets.

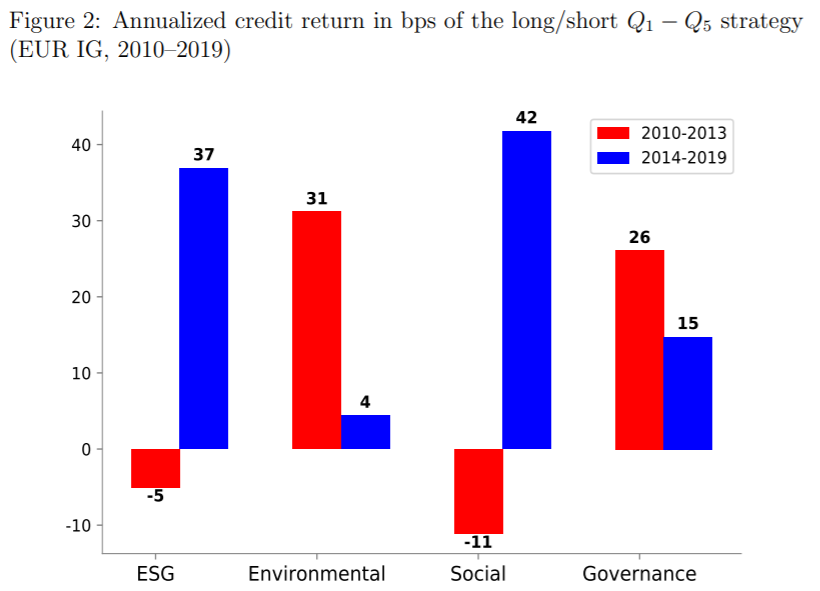

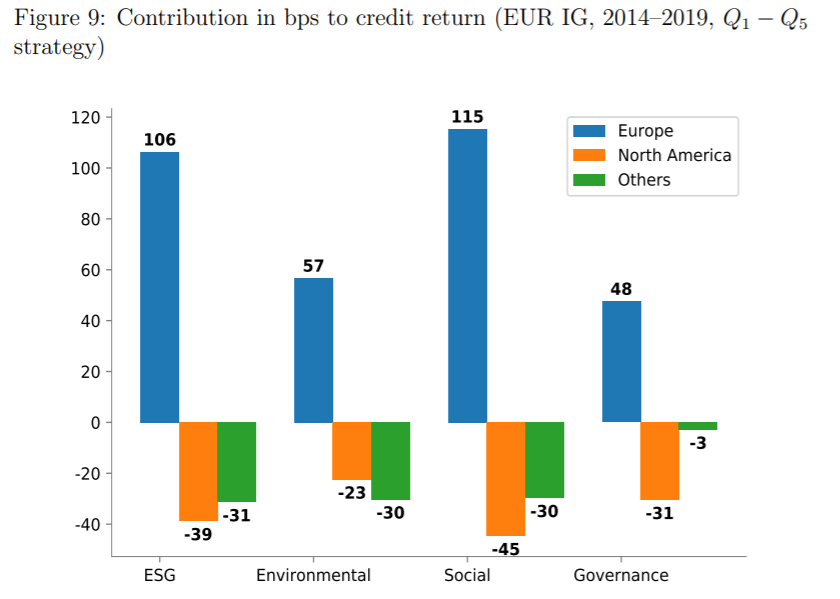

The objective of this new study is to explore the impact of ESG investing on asset pricing in the corporate bond market. For that, we apply the methodologies that have been used by Bennani et al. (2018) for testing ESG screening in active and passive management. In particular, we consider the sorted portfolio approach of Fama and French (1992), and the index optimization method that consists in minimizing the active risk with respect to the benchmark while controlling for the ESG excess score. Three investment universes are analyzed: euro-denominated investment grade bonds, dollar-denominated investment grade bonds, and high-yield bonds. Results differ from one universe to another. In the case of EUR IG bonds, we retrieve some common patterns observed by Bennani et al. (2018) in the case of equities. Indeed, from 2010 to 2013, ESG screening has produced a negative alpha, whereas we observe an outperformance since 2014 when we implement ESG scoring in active and passive management. In the case of USD IG bonds, the results are disappointing since ESG screening produces negative alpha for the entire period. Results on high-yield bonds are difficult to interpret since ESG coverage of this market is not satisfactory.

We also test how ESG has impacted the cost of corporate debt. Our results show that there is a positive correlation between ESG and credit ratings. This is normal since credit rating agencies also incorporate extra-financial risks in their default risk models. Using the approach developed by Crifo et al. (2017), we propose an integrated credit-ESG model in order to understand the marginal effects of ESG on the cost of capital. We find that there is a negative relationship between ESG scores and yield spreads. The better the ESG rating, the lower the yield spread. For instance, we estimate that the cost of capital difference is equal to 31 bps between a worst-in-class corporate and a best-in-class corporate in the case of EUR IG corporate bonds. In the case of USD IG corporate bonds, the difference is lower but remains significant at 15 bps. Moreover, the impact of ESG is more pronounced for some sectors, for instance Banking and Utility & Energy. These results are important because ESG investing and ESG financing are two sides of the same coin. In order to tackle environmental and social issues, ESG must be a winning bet for both investors and issuers.

As always, the results can be presented through interesting charts:

Notable quotations from the academic research paper:

“In the case of bonds, the development of ESG investing is less advanced,

and for many reasons. First, credit agencies pretend to incorporate ESG risks in their ratings, even if it is only one component among others. By the way, we can expect a convergence between credit rating agencies and ESG rating agencies in the future (Nauman, 2019). Second, bond scoring systems are mainly driven by three factors: duration, credit spread and liquidity. In a diversified investment grade portfolios, duration and credit risk are the two main active bets and there is less room to play some idiosyncratic risk than in a portfolio of large cap stocks. Third, liquidity issues imply that a significant part of bond portfolios is managed using a buy-and-hold strategy. Therefore, systematic rebalancing is less obvious implying that active bond management with ESG signals is complex. Fourth, there is a big difference between investing in stocks or bonds in terms of capital structure. The stock holder is the owner of the firm, and his concern is that the firm is well-managed in the short run in order to prepare the long-term business. The return on equity is then unknown and stochastic. The goal of the bond holder is different. He receives a known and constant return on debt, and faces the risk that the firm defaults before the bond maturity. His primary objective is then to manage the default risk of the firm (Merton, 1974). If the long-term business of the firm gets worse, the stock holder is impacted, but not the bond holder as long as the firm fulfills all its credit obligations. Therefore, it makes sense that equities are more sensitive to extra-financial risks than bonds. Finally, the fifth reason concerns the mindset of investors. Generally, they incorporate ESG scoring directly in the management of their equity portfolio and this integration becomes increasingly comprehensive as the investors develop their ESG expertise. They do not dramatically change how they manage their fixed income portfolio. In fact, ESG investing in fixed income is more identified with pure play securities such as green, social or sustainability (GSS) bonds. Therefore, it seems that ESG investing is more related to impact investing in the bond universe.

The results on the EUR IG bond market share many common points with those obtained by Bennani et al. (2018) and Drei et al. (2018) with the stock market. Indeed, we observe that the 2014–2019 period is more favorable to ESG investors than the 2010–2013 period. In the first period, we generally observe a negative alpha in terms of active management when ESG investors implement best-in-class versus worst-in-class bond selection, and underperformance of ESG tilted portfolios. In the second period, the active management strategy creates a positive alpha and ESG optimized portfolios have positive excess returns with respect to the benchmark index. Among the different pillars, Social is the winning pillar.

If we consider USD IG corporate bonds, results are mainly negative. However, we observe a trend that the cost of ESG investing has decreased over time. In recent years, the alpha of ESG active and passive management remains negative, but it is lower. In the case of high-yield bonds, results are less convincing and we also face some robustness issues.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend