ESG Ratings Disagreement in 2023

Sustainable investing is a topic we cover extensively in the form of systematic ESG investing strategies and/or blogs. Enormous capital allocation decisions are based on ESG ratings given by various agencies. The problem is that there is no actual normalization and standardization, which creates wrinkles on the faces of hedge and pension fund managers when making those critical individual equity allocations, be they inclusions or exclusions.

Ehling, Paul and Sørensen, Lars Qvigstad’s (January 2023) new paper analyzes the portfolio choice consequences arising from the well-known divergence of ESG scores. From a risk point of view, the optimized ESG portfolios differ more across each other than they differ relative to the benchmark, suggesting that the different rating agencies’ scores result in substantially different portfolios. Funds with high ESG scores tend to have high quality and momentum factor loadings using MSCI ESG scores. On the other hand, several asset managers have negative screens, which force a zero weight on the excluded stocks.

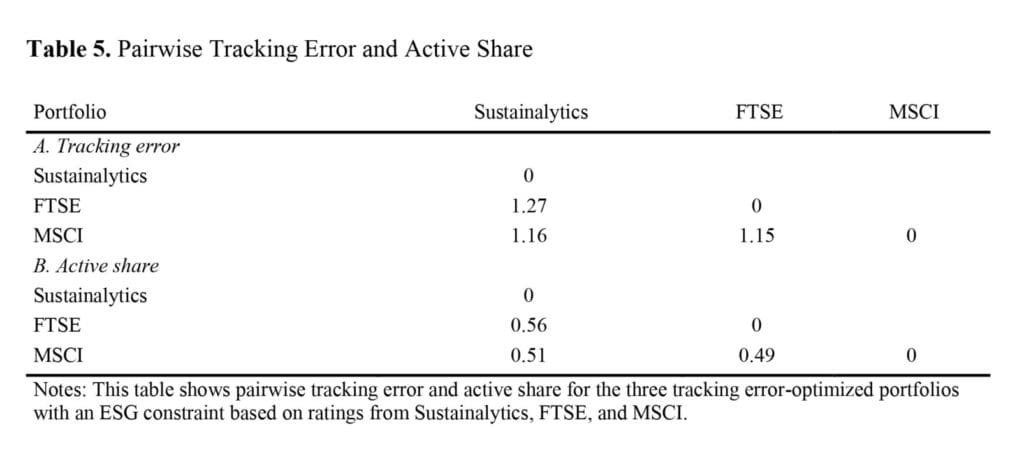

Authors conclude that this divergence is exacerbated when constructing minimum tracking error portfolios subject to a portfolio-level constraint on ESG scores. The pairwise tracking errors between the optimal portfolios are all higher than those portfolios’ 1% tracking error (see Table 5 below) relative to MSCI World. The implication and essential message for the asset management industry and us, individual investors, is that an ESG-motivated portfolio differs substantially based on the agency chosen for the ESG ratings. The choice of ESG provider should not be passive but a deliberate decision. Ultimately, the asset manager (or you!) must decide which rating agency supplies ratings consistent with the asset manager’s (your) values and beliefs. This decision and its reasons should be conveyed to stakeholders, thus allowing clients an informed choice.

And how dissimilar are ratings among the agencies? We find staggeringly comic that ratings of Warren Buffett’s (and Charlie Munger’s) Berkshire Hathaway (NYSE: BRK.B) disagree by a large margin (see red ellipses in Figure 2 below). While Sustainalytics give it an outperforming rating, FTSE and MSCI regard it as one of the top laggards.

Authors: Paul Ehling and Lars Qvigstad Sørensen

Title: Portfolio Choice with ESG Disagreement

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4328880

Abstract:

What are the implications of disagreement about environmental, social, and governance (ESG) ratings for portfolio choice? Constructing an optimal portfolio for each ESG rating agency by minimizing tracking error while satisfying a portfolio-level ESG constraint, we found that ESG rating disagreement was exacerbated, yielding significantly different optimal portfolios. Optimal active weights increased with the ESG rating, as expected, but were shrunk toward zero for stocks with high stock-specific risk or low benchmark weight. We conclude that optimal portfolio choice and resulting ESG properties are highly dependent on rating agency.

And, as always, we present several exciting figures and tables:

Notable quotations from the academic research paper:

“Our optimal portfolio choice tilts the portfolio such that an investor holds positive active weights in sustainable companies and negative active weights in ESG laggards, while remaining within tracking error limits. This approach to portfolio construction is similar to that used in a different context in Bolton, Kacperczyk, and Samama (2022). They utilized the framework introduced in Andersson, Bolton, and Samama (2016) and examined how investors can be aligned with the goal of carbon net neutrality while at the same time maintaining an acceptable level of tracking error. In contrast, we examined differences in constituents that resulted from using ESG data from different agencies in the tracking error optimization. Importantly, our results were obtained assuming a long-only constraint, consistent with the restriction faced by most portfolio managers (Almazan, Brown, Carlson, and Chapman 2004).

We found that differences in ESG scores did not wash out in the optimization, however: using scores from different raters yielded substantial differences in optimal portfolios. The three optimal portfolios were more different among themselves than they were compared to MSCI World, which constituted the benchmark. The ex-ante tracking error between the optimal portfolios ranged from 1.15% to 1.27%, compared to each portfolio’s 1% tracking error against MSCI World by construction. Furthermore, the largest active weights differed greatly among the three optimal portfolios. In fact, the largest positive active weight using FTSE ESG scores (Johnson & Johnson) was the largest negative active weight using MSCI ESG scores. A portfolio manager must thus rely on quite different arguments justifying the ESG properties of the largest bets taken depending on the ESG ratings of the provider that was chosen.

Taken together, our main results indicate that the problem of ESG rating divergence is exacerbated in a realistic portfolio choice context, prevalent among practitioners. The active weights of the three optimal portfolios had a low pairwise correlation, and active weights in one optimal portfolio explained very little of the variation in active weights in another optimal portfolio. There exists a silver lining in terms of portfolio choice agreement, however: the three optimal portfolios agreed on a zero weight in 689 out of 1404 stocks, which constituted 23.1% of the weights in MSCI World on the analysis date.

Our results dispel the notion that different index-tracking ESG portfolios have similar risk profiles and choose similar portfolio weights. This means that vendor choice is an active and crucial decision with respect to portfolio choice. Robertson (2019) documented large heterogeneity between index funds, leading to the conclusion that important decisions were delegated to the index creator. The same outsourcing of portfolio choice decisions takes place when using ESG ratings that diverge substantially as inputs in portfolio optimization. A key recommendation in this paper is therefore that asset owners, asset managers, and other stakeholders must ascertain that ESG data from their chosen rating agency and the resulting portfolio are aligned with their views about sustainable investing.

In this study, we employed a risk-based approach to portfolio construction. Specifically, we minimized the relative risk versus a benchmark, while at the same time achieving a minimum desired ESG threshold. In optimum, the ESG constraint will be binding. This is trivially true because the starting point is the benchmark itself, against which a portfolio without an ESG constraint achieves zero tracking error by simply choosing no deviations from the benchmark weights in optimum.

The key ingredient to performing a tracking error minimization is the covariance matrix of returns. Computing the covariance matrix is non-trivial and requires modeling. Many assets, some of which have a short return history, complicate the estimation of the covariance matrix. Therefore, a popular solution is to posit a factor model for returns, where the number of factors is much smaller than the number of stocks, thereby reducing the dimensionality of the problem. To compute risk and the covariance matrix, we used MSCI Barra, one of the leading providers of risk solutions (see, e.g., Pedersen et al. 2021). This matrix is always nonsingular, which means it can be inverted to solve for the optimal portfolio. The portfolios were optimized using the long- term version of the MSCI Multi-Asset Class (MAC) factor model.

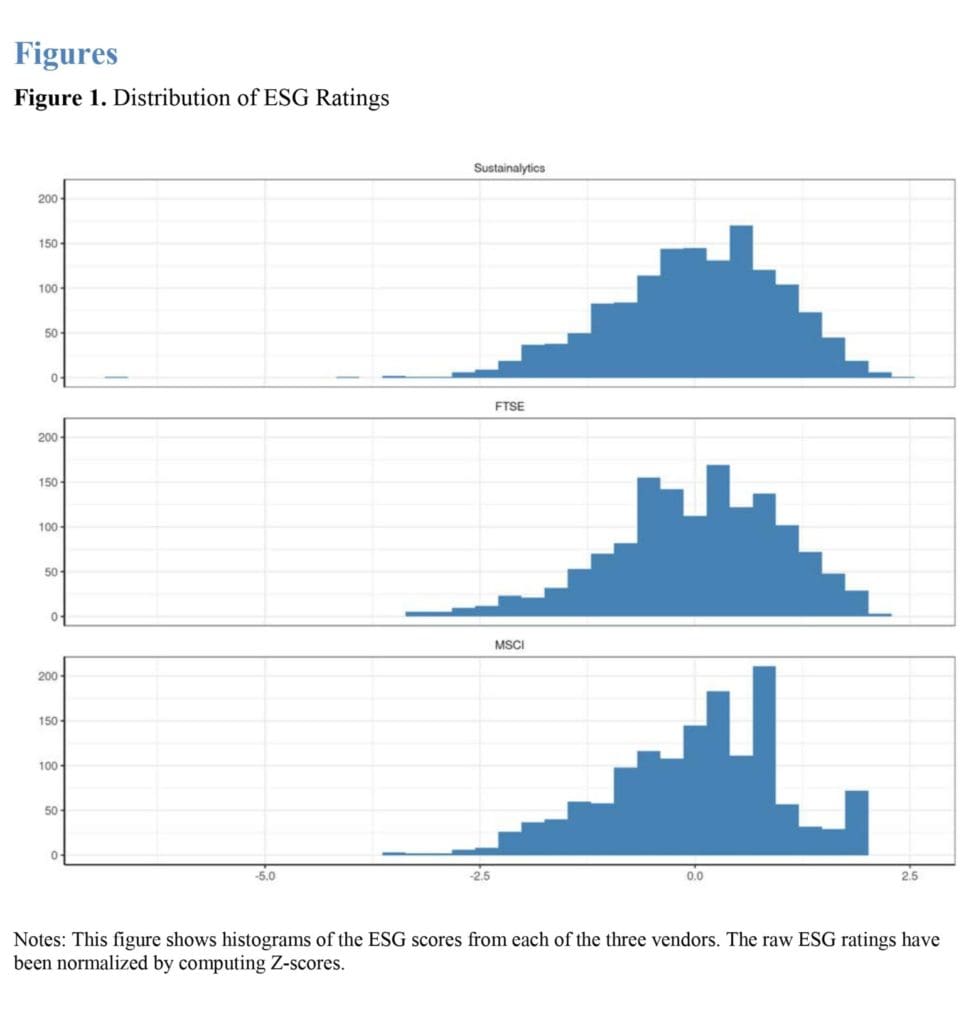

Figure 1 shows histograms of ESG Z-scores for each rater. We changed the sign when computing the Z-score for Sustainalytics because a lower raw number implies lower ESG risk and hence a better ESG score. Sustainalytics had the most granular ESG data with a score that behaved like a continuous variable with 1,387 distinct values. FTSE had 43 and MSCI had 98 distinct scores. All raters’ scores displayed fat left tails, meaning that some companies had very poor ESG properties. There was no similar right tail. As can be observed from the graph, MSCI awarded the highest rating to more companies than the other two vendors.

Table 1 shows descriptive statistics for the three optimal portfolios and the benchmark, MSCI World. The first three columns refer to the source of the ESG data used in the portfolio-level ESG constraint, that is, they represent the three optimal portfolios. The first row shows that there is a considerable reduction in the number of stocks relative to MSCI World for the ESG- optimized portfolios, with the number of stocks in the optimal portfolios ranging from 23% to 29% of the number of eligible stocks from MSCI World. In our view, this reduction in the number of stocks justifies the choice of tracking error limit as the features we wanted to highlight are present despite limiting the tracking error to 1%. The next three rows show the value- weighted Z-scores for the portfolio ESG ratings using each vendor’s score in the portfolio-level ESG constraint.15

Figure 2 shows a bar chart with the largest positive and negative active weights relative to the benchmark MSCI World for each rating agency. Individual points represent the standardized ESG score corresponding to each rater. Circles indicate an ESG score above the mean and triangles a score below the mean. All positive active weights have an ESG score above the mean, but some of the negative active weights have a positive standardized ESG score, illustrating that there is no linear relation between scores and optimal weights.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend