How Does the Passive Investing Impact Market Risk?

The rise of passive investing has been one of the most profound trends in the asset management industry in the past two decades. However, how does the popularity of passive funds impact market risk? We can rely on the data, and a recent research paper shows that the impact is significant, mainly through a substantial increase in stock correlations. As more investors flock to passive funds, which track indices, the prices of stocks within those indices tend to move more in tandem, increasing market-wide risk.

The presented paper focuses on the impact of passive investing on risk measures – second moments of stock returns. Academics find that passive investing (and index-based common ownership in general) has an asymmetric impact on different components of risk: While it contributes to systematic, co-movement-related risk measures, it is mainly unrelated and often observed to be negatively related to non-systematic, idiosyncratic movements. Since idiosyncratic price moments are considered essential signals for firm-specific information, their finding raises the question of whether the rise of passive investing (and other implicit index-based investing) will alter the information structure and efficiency in the price discovery process.

Academics hypothesize and show that the popularity of passive investing can undo the benefits of diversification and lead to higher market-level volatility: Market volatility has risen since around 2000 and is concurrent with passive investing, driven by higher correlations among individual stocks.

A firm-level variable that captures the extent to which a stock is held by passive investment vehicles – index funds and ETFs for the entire CRSP universe of stocks, can be constructed. Authors find a consistent and robust result that this measure is highly positively related to risk measures that reflect a stock’s co-movement with other stocks and the market: its beta, its average correlation with all other stocks, and its average covariance with all other stocks, but it is unrelated (or even negatively related in some specifications) to a stock’s idiosyncratic volatility. In other words, a stock’s exposure to passive investing positively contributes to the systematic (undiversifiable) portion of its risk but not to its non-systematic (diversifiable) portion.

Examining three episodes of sudden and largely exogenous rise in market volatility—the post-9/11 period, the 2008 financial crisis, and the 2020 COVID pandemic – in a difference-in-differences setting shows that the relation between passive investing and systematic risk becomes stronger during crisis periods as the risk contribution of stocks with high exposure to passive investing increases.

Correlated trading by passive funds likely explains these effects. First, stocks extensively held by passive funds have higher trading volume (turnover) correlations with other stocks. Second, the flow-induced trading of passive funds contributes positively and significantly to the co-movement-related risk measures: beta, correlation, and covariance, but not idiosyncratic risk. These results indicate that correlated trading affects aggregate risk through a co-movement, or systematic, channel instead of a volatility channel.

While the study focuses on index funds and ETFs with an explicit passive mandate, the true extent of index-based investing could be far more significant due to performance benchmarking and other fund manager incentives. Authors show that benchmark-driven closet-indexing practices have directionally the same effect as passive investing on stocks’ risk measures. Still, their effects do not subsume the impact of passive funds. Estimates suggest that explicit passive investing alone could explain a 20% increase in market risk over the last four decades (from 1980 to 2020). The true extent of the effect of index-based investing on market risk will, therefore, be even more significant – likely double – if implicit indexing is also considered.

Authors: Lily H. Fang, Hao Jiang, Zheng Sun, Ximing Yin, and Lu Zheng

Title: Limits to Diversification: Passive Investing and Market Risk

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4928631

Abstract:

We show that the rise of passive investing leads to higher correlations among stocks and increased market volatility, thereby limiting the benefit of diversification. The extent to which a stock is held by passive funds (index mutual funds and ETFs) positively predicts its beta, correlation, and covariance with other stocks, but not its idiosyncratic volatility. During crisis periods, stocks with high passive holdings contribute more to market risk compared to before the crisis. Correlated trading by passive funds explains these results, which are further amplified by implicit indexing due to performance benchmarking.

As always, we present several exciting figures and tables:

Notable quotations from the academic research paper:

“[…] paradox is the focus of our paper. We study how index-based investing – both index funds and index ETFs, which we collectively refer to as “passive investing” in this paper – affects the correlation structure between assets and, ultimately, the overall market volatility. Along the rationale outlined above, we hypothesize that passive investing increases correlations among assets and, since correlations among assets determine the aggregate market volatility, it also increases overall market volatility.

Our hypothesis has profound implications for market efficiency and the cost and benefit of passive investing. A large literature exemplified by Jensen (1968) and Carhart (1997) has presented robust evidence of the benefits of passive investing: Actively managed mutual funds generally do not outperform passive funds after fees and expenses. But our hypothesis suggests an important downside to the significant expansion of passive investing: Its rise could lead to higher market-level volatility, limiting the power of diversification and the virtue of passive investing itself.

Our hypothesis is based on the notion that passive investing often involves the simultaneous buying and selling of securities within an index, and this correlated trading can lead to increases in stocks’ systematic risk measures such as beta and correlation with other stocks (e.g., Basak and Pavlova 2013). To directly shed light on this mechanism, we first show that stocks with a high index exposure have higher trading volume correlation with other stocks in the market. We then examine the effect of trading induced by index and ETF fund flows (we call this passive-flow-induced trading). We construct a stock-level measure that captures the passive-flow-induced net trading of the stock across all index funds and ETFs in our sample. Presumably, the buying pressure induced by the inflows of some funds could be offset by the selling pressure driven by the outflows from other funds. Our measure captures the net amount of flow-induced trading that cannot be absorbed within the index fund sector, thus reflects a net liquidity demand by index funds to other investors. We find that this passive-flow-induced-trading is significantly correlated with stocks’ beta, average correlation, and covariance with other stocks, but negatively correlated with stocks’ idiosyncratic volatility. Moreover, the contributing effects of passive-flow-induced-trading on beta, correlations, and covariance, are especially strong during the crisis periods defined above. These results help establish correlated trading among passive funds as a likely channel through which passive investing affects market risk.

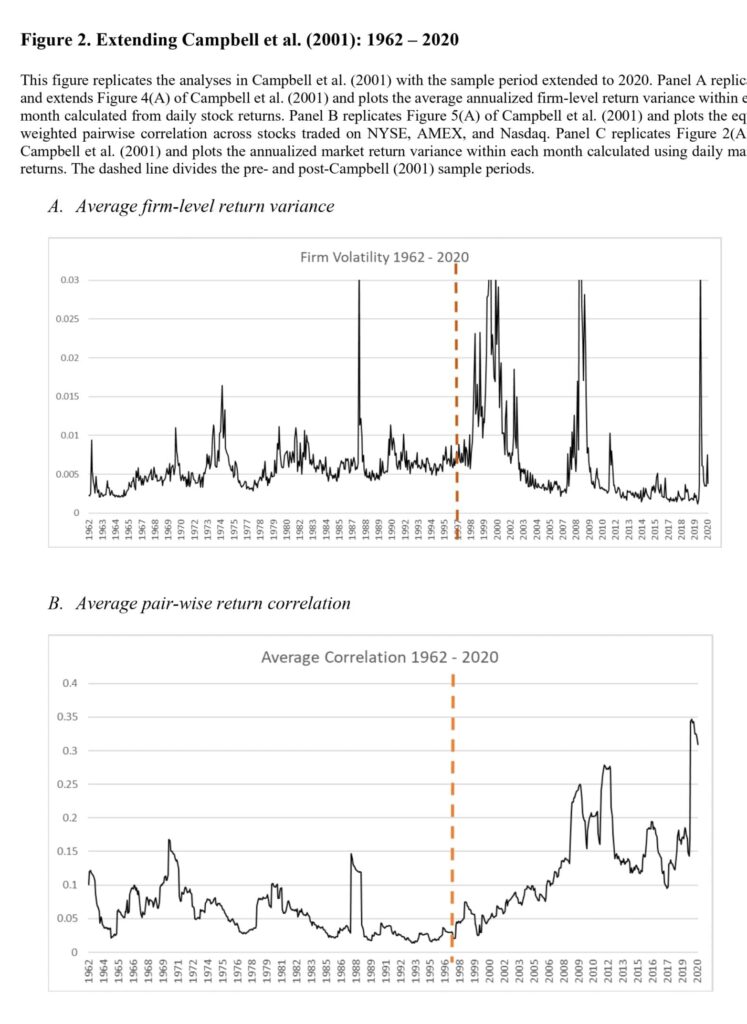

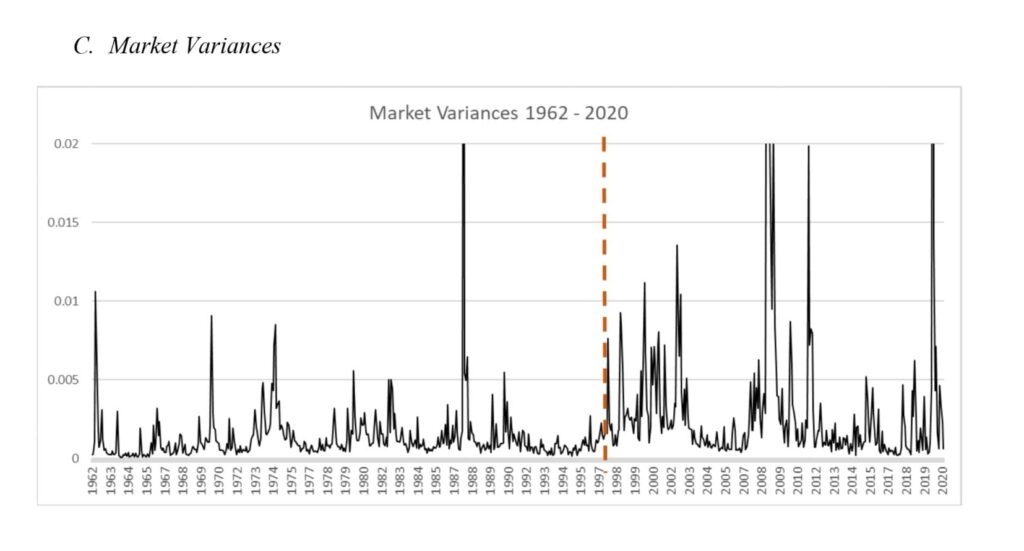

Figure 2 extends the sample period to 2020 and reveals a stark contrast between the pre- 1997 period and the time since. Panel A shows that individual stock volatility continued to rise until about 2001 but has since declined. In contrast, Panel B shows a striking increase in pair-wise correlation among stocks post 1997: the average pair-wise correlation is 13.4% in the period of 1998- 2020, more than doubling the 5.7% for the period 1962-1997 (t-statistic=17.85 for the difference). Panel C shows that the net effect of these two forces is an increase in market-level variance in the post 1997 era; the average pre- and post-1997 market annualized return volatility is 12.51% and 19.56% respectively, and the difference is statistically significant (t-statistic = 5.44).

[…] there can be multiple factors contributing to the increase in correlations among stocks, our paper focuses on the rise of passive investing—index funds and index ETFs. Figure 3 plots the extent of passive investing in the stock market—measured by the “Passive-to-Market” ratio, which is the total assets under management by index funds and index ETFs divided by the total market capitalization of all stocks—against the average pair-wise correlation among all stocks in the CRSP universe over the period of 1980 to 2020. While the quarterly average stock correlation series is quite volatile, the graph nevertheless reveals long term positive correlation between the two series.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend