Retail Investment Boom, Robinhood, Passive Investing and Market Inelasticity

This week’s blog is unique compared to our previous posts. We have identified two papers that are connected, each with interesting findings and implications. One of today’s leading topics is the Robinhood trading platform, but not from the point of view of recent short squeezes and speculations. The Robinhood can be an interesting insight into retail investing and implications for the market. Research suggests that despite the very low share of retail investors, their power is significantly high. This seems to be caused by the inelastic market, which passive investing contributes to. Therefore, inelasticity is another crucial point.

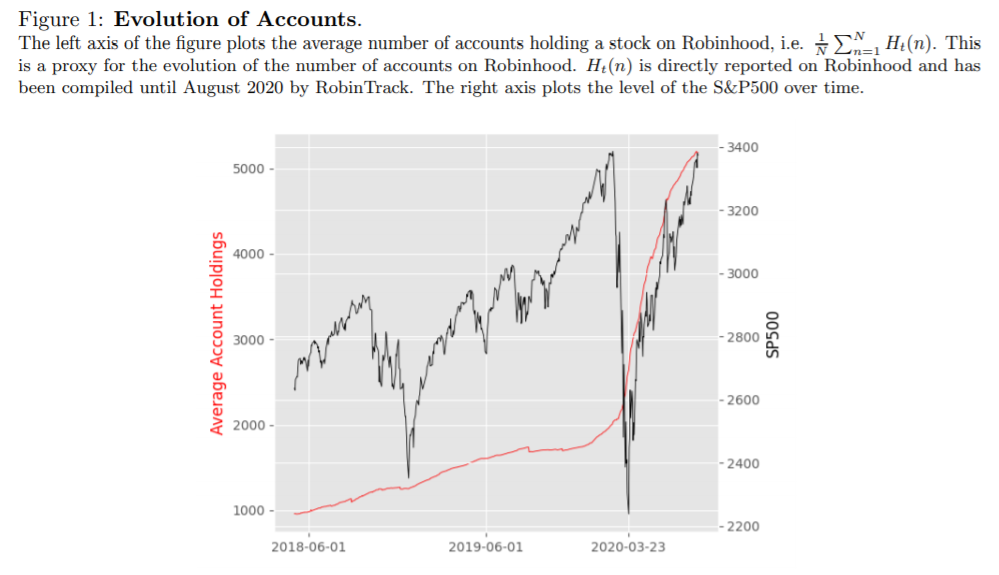

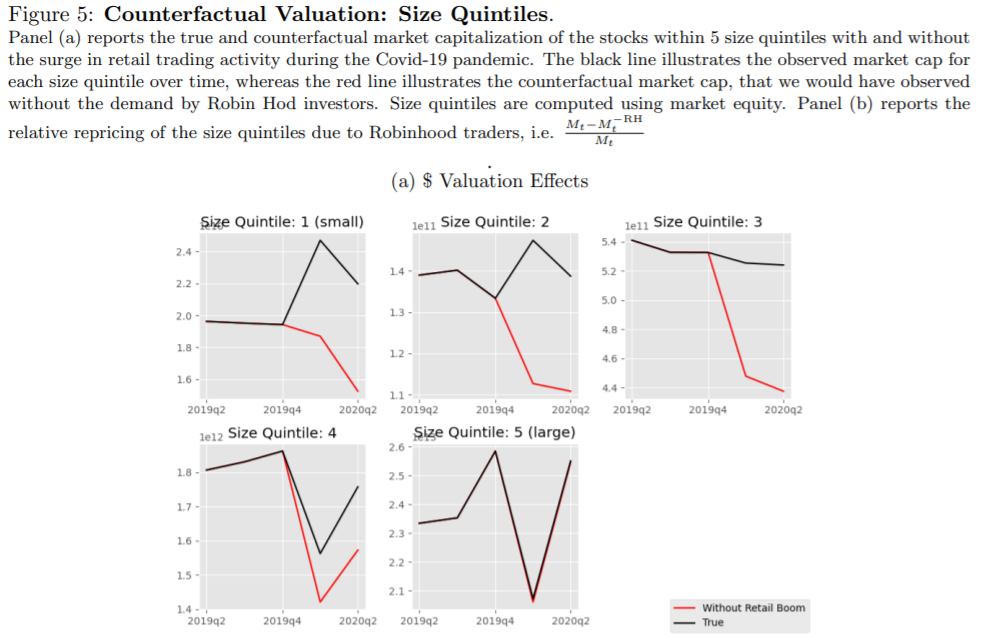

Lately, Robinhood was in the spotlight mainly thanks to the short-squeezes on stocks like Gamestop or AMC. Indeed, the business model of Robinhood and their commission-free investing attracts many retail investors. However, these speculative trades are not the only exciting insights from the platform. The Robinhood investors played their significant part in the sharp recovery after the covid market fall. The novel research of van der Beck and Jaunin (2021) examines the role and magnitude of influence of the retail investors on the Robinhood. Despite the retail’s small share, the authors show that retail investors and traders can significantly influence the market. The reason is probably another rising trend – passive investing. Institutional investors hold a significant part of the market with inelastic demand, which allows the active retail market participants to influence the market. How substantial is the impact? The academic paper shows that over 7% of the cross-sectional return variation is connected with retail traders’ demand on the Robinhood platform, even that their overall market share is minuscule (0.2%). Additionally, the users provided liquidity during big sellouts of institutions and helped with the recovery. Based on the approximation of the AUM, these traders have a multiplier effect of 5. To sum it up, Robinhood’s users’ activity provides an excellent opportunity to study the rising influence of retail traders and investors on the financial markets.

Authors: Philippe van der Beck and Coralie Jaunin

Title: The Equity Market Implications of the Retail Investment Boom

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3776421

Abstract:

Retail trading activity has soared during the COVID-19 pandemic. This paper quantifies the impact of the retail investment boom on the US stock market within a structural model. Using account holdings data from the online trading platform “Robinhood Markets Inc.” and 13F filings, we estimate retail and institutional demand curves and derive aggregate pricing implications via market clearing. The inelastic nature of institutional demand allows Robinhood investors to have a substantial effect on stock returns during the COVID-19 pandemic. Despite their negligible market share of 0.2%, we find that Robinhood traders account for over 7% of the cross-sectional variation in stock returns during the second quarter of 2020. We furthermore show that without the surge in retail trading activity the aggregate market capitalization of the smallest quintile of US stocks would have been over 30% lower. Lastly, Robinhood traders are able to affect the price of some large individual companies that are being held primarily by passive institutional investors.

Additionally, the inelasticity is probably even better analyzed in a research paper of Gabaix and Koijen (2021), accompanied with an extensive theory and propositions. Everyone interested in the financial markets must have observed that the proportion of passive investments is on the rise and that the actively managed capital is shrinking. These changing proportions raise many questions. Is the market becoming more inelastic? And how are the prices connected with the flows into the market? As it was previously mentioned, the theory is truly extensive in this research. However, there are several key results and hypotheses worth highlighting. According to the efficient markets theory, the stock´s price should be equal to the present value of future dividends (discounted dividends model). Therefore, the inflow of one dollar should not have any effect on the market. Contrary to this theory, authors theoretically and empirically show that the market´s value goes up five-fold (the previous research paper has identified a multiplier effect of 5). The inflow of one dollar into the stock market causes an increase in the aggregate market valuation of five dollars. Therefore, flows, whether in or out, affect the market significantly, and there is a sizeable impact both on prices and risk premia. Thus, the authors hypothesise that the markets are highly inelastic.

Authors: Xavier Gabaix and Ralph S. J. Koijen

Title: In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3686935

Abstract:

We develop a framework to theoretically and empirically analyze the fluctuations of the ag- gregate stock market. Households allocate capital to institutions, which are fairly constrained, for example operating with a mandate to maintain a fixed equity share or with moderate scope for variation. As a result, the price elasticity of demand of the aggregate stock market is small, so flows in and out of the stock market have large impacts on prices.

Using the recent method of granular instrumental variables, we find that investing $1 in the stock market increases the market’s aggregate value by about $5. We also show that we can trace back the time variation in the market’s volatility to flows and demand shocks of different investors.

We also analyze how key parts of macro-finance change if markets are inelastic. We show how general equilibrium models and pricing kernels can be generalized to incorporate flows, which makes them amenable to use in more realistic macroeconomic models, and to policy analysis. Our calibration implies that government purchases of equities have a non-trivial impact on prices. Corporate actions that would be neutral in a rational model, such as share buybacks, have substantial impacts too.

Our framework allows us to give a dynamic economic structure to old and recent datasets comprising holdings and flows in various segments of the market. The mystery of apparently random movements of the stock market, hard to link to fundamentals, is replaced by the more manageable problem of understanding the determinants of flows in inelastic markets. We delineate a research agenda that can explore a number of questions raised by this analysis, and might lead to a more concrete understanding of the origins of financial fluctuations across markets.

As always we present several interesting figures:

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend