How Fragile is Liquidity Across Asset Classes?

Authors: Nihad Aliyev, Matteo Aquilina, Khaladdin Rzayev, Xingyu Sonya Zhu

Title: Through Stormy Seas: How Fragile is Liquidity Across Asset Classes?

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5254046

Abstract:

Liquidity has improved across global markets, but fragility concerns remain. We study the distribution of bid-ask spreads across equities, bonds, and foreign exchange (FX) in the US, Europe and Japan. While average and standard deviation of spreads have decreased since 1990s, skewness and kurtosis have increased, especially in bond and most equity markets, but not FX. We identify structural breaks in the mean and skewness and map them to macroeconomic events, market structure changes, and regulatory reforms. Simulations show that increased skewness raises trading costs-up to $1 billion annually in US equities-even when few trades require urgent execution.

As ever, we present several interesting figures and tables:

Notable quotations from the academic research paper:

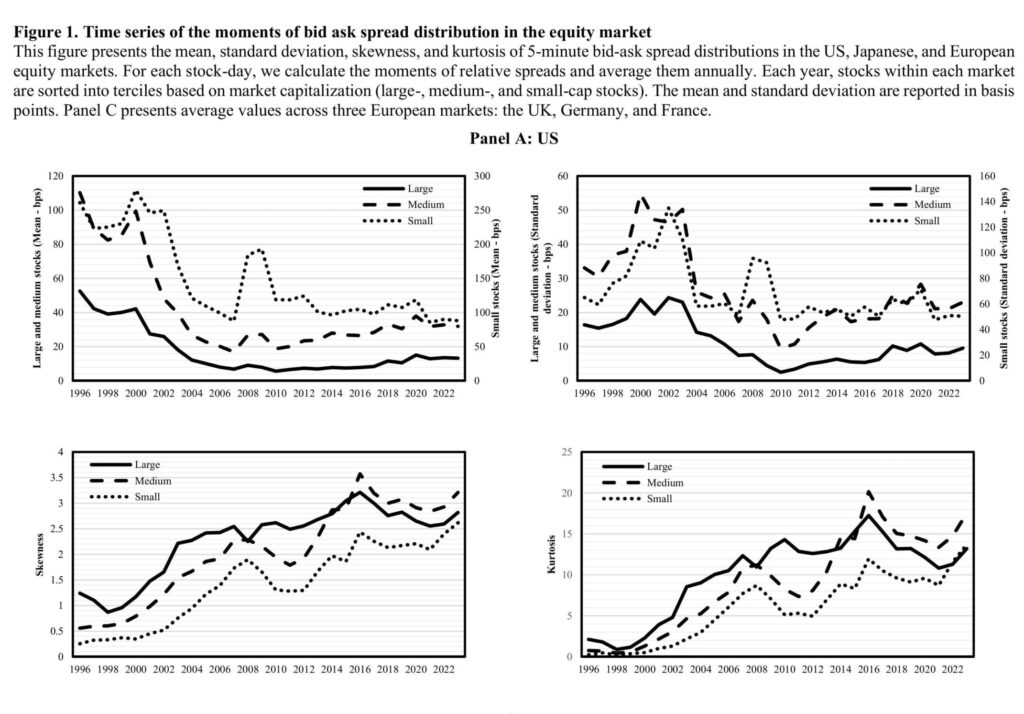

“[…] we go beyond average measures of liquidity and examine how higher-order moments of its distribution, specifically skewness and kurtosis, have evolved over time. Our aim is to understand how liquidity behaves not only in normal times but also in the tails during periods of stress when it matters most. We focus on three major asset classes: stocks, government bonds, and foreign exchange (FX). These markets play a critical role in capital allocation, monetary policy transmission, and risk management for governments, corporations, and investors. We study the distribution of bid-ask spreads (and other liquidity measures for robustness) across the key developed markets of the United States, Europe, and Japan.1 To this end, we compile a high- frequency dataset of relative bid-ask spreads, which we aggregate into monthly and annual metrics to capture the distribution of liquidity over time, across asset classes, and across regions.

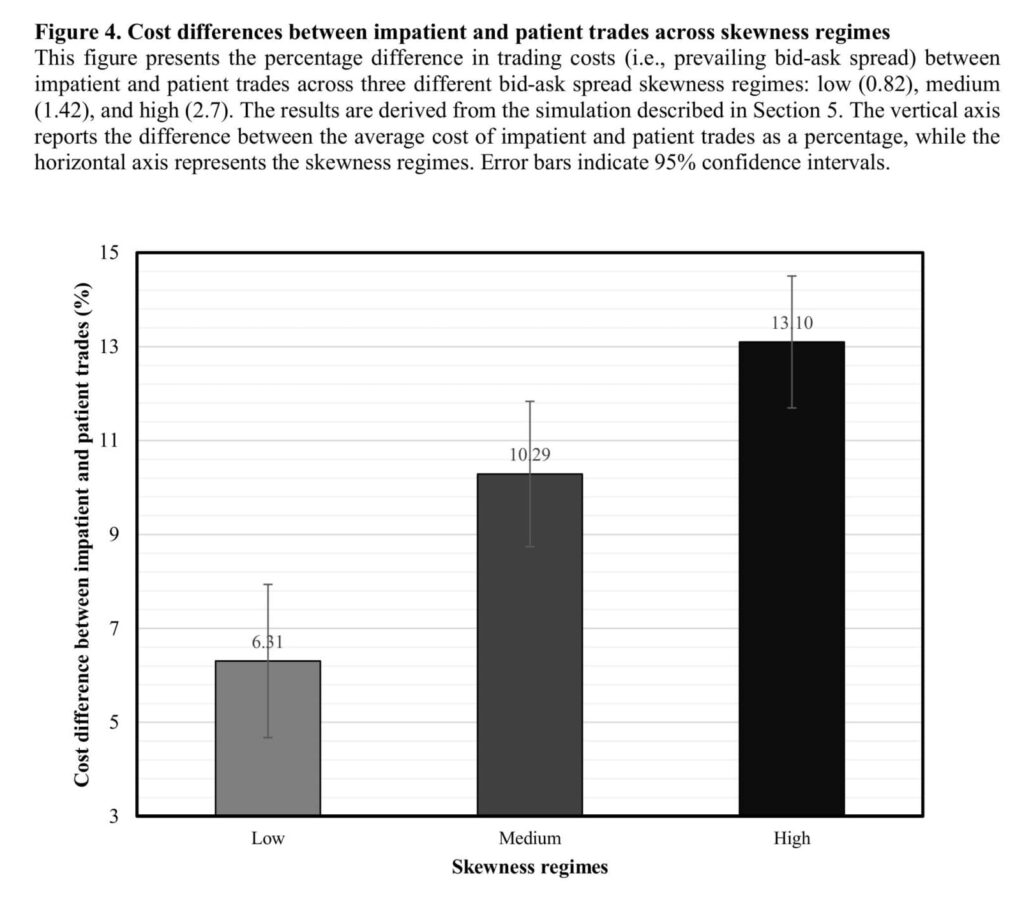

Simulation results show that changes in the skewness of spreads can have meaningful effects on trading costs. We find that moving from the low-level of skewness of the late 1990s to the high-level of US large cap equities in 2023, the trading cost difference between patient and impatient trades becomes significantly larger. In the low-skewness environment, the premium paid for immediate execution is around 6%, but it more than doubles to 13% in the high skewness environment. When the probability of being impatient is low, overall trading costs remain similar across different skewness levels as traders can wait for the spread to revert. However, as the probability of impatience increases—a condition more likely during market stress—trading costs increase quickly in high-skewness regime.

[…] First, to our knowledge, we are the first to document how the distribution of liquidity has evolved across three major asset classes (equities, government bonds, and FX) in the major global markets of the US, Europe, and Japan, drawing on a dataset of over 2 billion high-frequency observations. This broader perspective is important because it allows us to compare patterns across markets that differ in structure, participants, and regulation. For example, FX markets—where average spreads have decreased but skewness has not increased—may offer useful insights into mechanisms that preserve the resilience of liquidity. Understanding these differences can help identify which aspects of market design contribute to more stable liquidity and what structural features one market might adopt from another to improve the resilience of liquidity.

Second, we go beyond describing trends and identify potential drivers of both mean and skewness of liquidity and link them to macroeconomic events, market structure, and regulation across different markets and regions. This allows us to disentangle the factors associated with improvements in average liquidity from those contributing to its increased fragility. Third, we quantify the trading cost implications of skewed liquidity using simulations. We show that higher skewness in spreads, even when average conditions are stable, can increase costs for traders who need to execute quickly. Together, our findings provide new evidence on what makes liquidity fragile across different markets and why that matters for market participants.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend