How Much Are Bitcoin Returns Driven by News?

The main theme of these days in the crypto world is unmistakenly clear, it’s the mayhem connected with the collapse of the FTX empire, insolvencies of various lenders, and questions about underlying holdings in GBTC OTC ETF and reserves of exchanges and Tether (or other stablecoins as well). With new information, nothing does paint a bright picture of this industry in the financial world now and in the near future. Calls for finally working regulations are getting stronger and stronger, while politicians (and central bankers) are still active on Central Bank Digital Currencies (CBDCs) proposals. While Bitcoin survived several crypto winters, long-term investors are continuing their DCA-ing and “stashing Satoshis” Are they safe? Do they pay attention to the surrounding news? In our short cryptocurrency research blog entry, we will focus on the question of how news impact Bitcoin returns, being both the most famous cryptocurrency and also the one with the highest market capitalization.

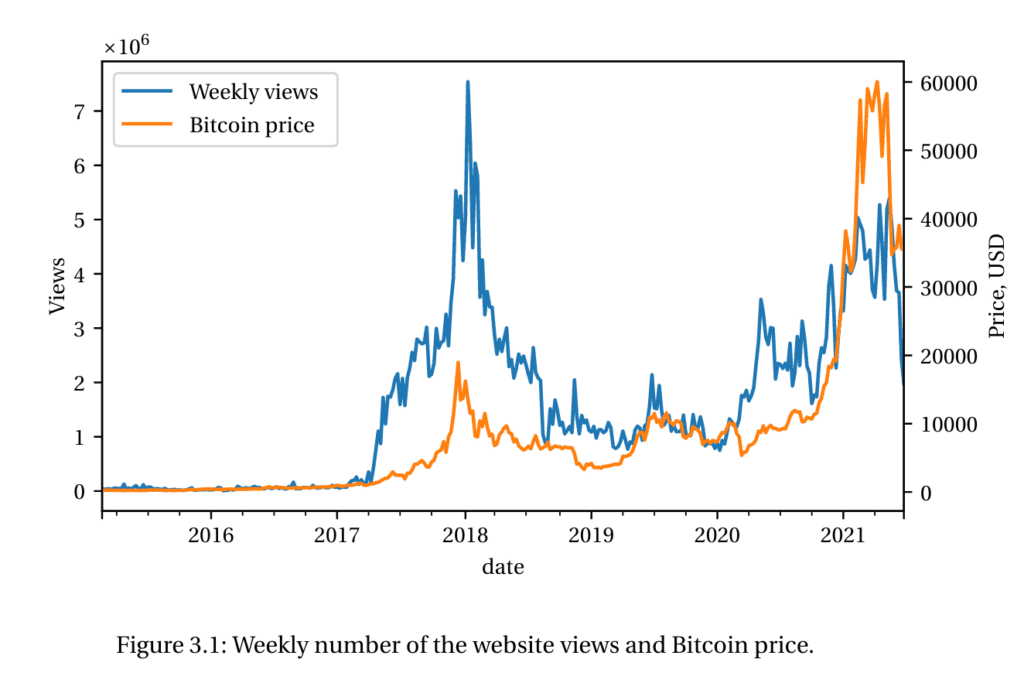

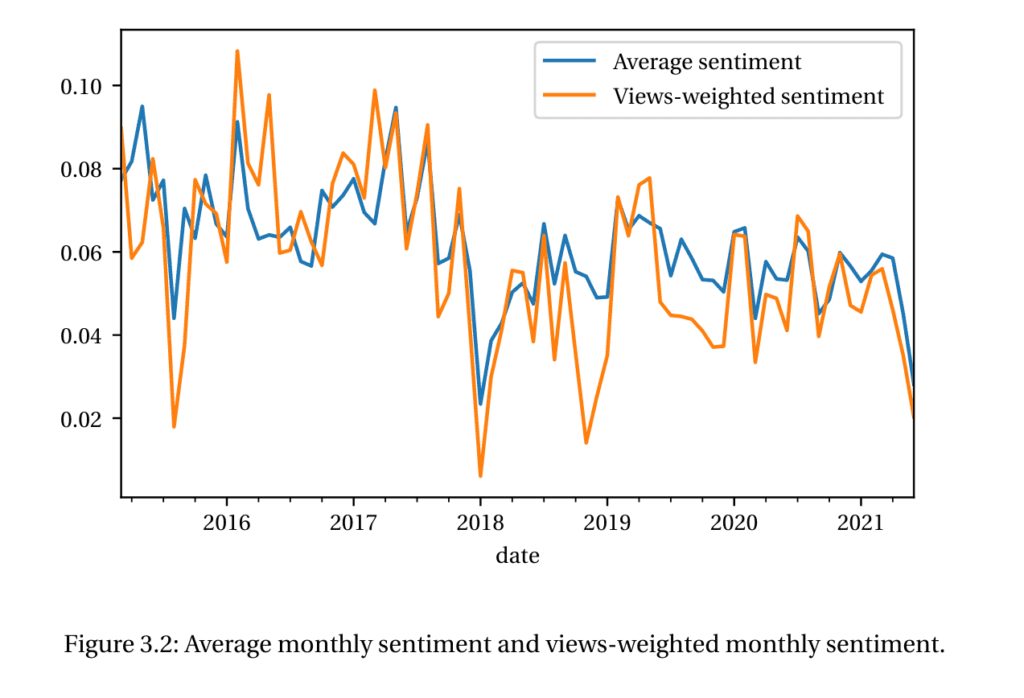

A novel paper by Bashchenko (2022) from the Swiss Finance Institute Research Paper Series proposes to use the news as a proxy for the fundamental information driving Bitcoin price by Natural Language Processing (NLP) utilizing the methodology of Approach Sentence-BERT (SBERT) network to obtain a comprehensible and easy-to-understand classification of the articles into a set of predefined topics of interest further analyzing their effects as vehicles on price action. A quite interesting observation is that the attention declines together with the Bitcoin price fall, but the popularity does not return to the previous peak levels even when Bitcoin price reached an all-time high in spring 2021. Another point is that the distribution of sentiment scores exhibits a moderate skewness — average sentiment in the sample is positive, declining towards the end of the sample, but even during the major crush of 2018, it remains positive. (See selected figures.)

A news database (ranging from 2013 up to 2021) collected from a specialized website is classified in a semi-supervised manner and shows that news sentiment is consistent with the information theory of media tone and thus contains information about coin fundamentals. And from these, 16% of Bitcoin return variation is explained by the fundamental news, thus rejecting the idea that the Bitcoin price is formed purely by speculation.

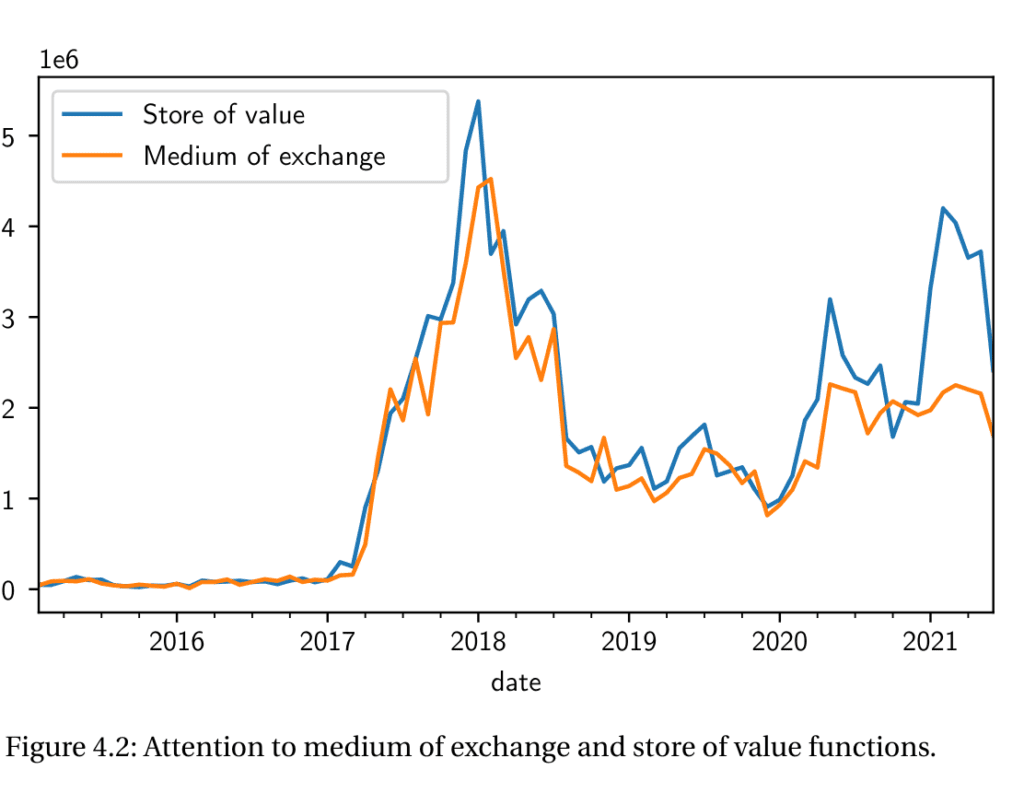

Wider adoption of cryptocurrencies and blockchain technology is highlighted as the most important driver of Bitcoin returns, while, at the same time, the store of value property is more valued by the investors than the medium of exchange (can be seen from the featured figure). Suppose we interpolate results into a wider range of cryptocurrencies, then it looks like the believers in these investment instruments are still out there to stay and are not going anywhere soon.

Author: Oksana Bashchenko

Title: Bitcoin Price Factors: Natural Language Processing Approach

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4079091

Abstract:

I propose a new methodology to construct interpretable, fundamental-based pricing factors from news to explain Bitcoin returns. Each news article from a specialized cryptocurrency website is classified in a semi-supervised manner into one of the few predefined topics. Topic sentiments become factors contributing to the price variation. I use a cutting-edge NLP algorithm (SBERT network) to embed linguistic data into a vector space, which allows the application of an intuitive classification rule. This approach permits the exclusion of news pieces that describe the price movements per se from the analysis, thus mitigating endogeneity concerns. I show that non-endogenous news contains fundamental information about Bitcoin. Thus I reject the concept of Bitcoin price being based on pure speculation and show that Bitcoin returns are partially explained by fundamental topics. Among those, the adoption of cryptocurrencies and blockchain technology is the most important aspect. On top of that, I study the media expressed attitude toward Bitcoin from the functions of money perspective. I show that investors consider Bitcoin as the store of value rather than the medium of exchange.

As always we present several interesting figures:

Notable quotations from the academic research paper:

“In this paper, I propose to use the news as a proxy for the fundamental information driving Bitcoin price. I use Sentence-BERT (SBERT) network to obtain a comprehensible and easy- to-understand classification of the articles into a set of predefined topics of interest. My first contribution is an efficient separation of the group of endogenous news (which simply describes the past price movements) from the fundamental news. For example, a news article reporting a recent cryptocurrency exchange hack is likely to influence investors’ beliefs about the future of Bitcoin, and thus I consider this news to be fundamental. At the same time, a news article reporting the performance of cryptocurrencies during the previous week is an example of endogenous (descriptive) news. Unlike the currently adopted benchmark, my solution alleviates the endogeneity concern by relying purely on the news content, instead of the time published. This allows to, first of all, work with news for never-closing Bitcoin markets, as well as to keep non-endogenous news arriving during the trading hours. Of course, this approach is not limited to cryptocurrency analysis. It opens wide possibilities for mitigating the endogeneity concern and producing meaningful economic insights when working with narrative data in any economic area. Second, I conclude that the explainability of Bitcoin price with news is at least comparable with the explainability of the traditional financial assets. I reach almost 38% explainability considering the full corpus of news. Moreover, taking care of endogeneity, I am still able to explain more than 16% of monthly Bitcoin return variation with fundamental news. Roll’s puzzle (Roll, 1988) formulates the infamous property of the classical, centuries-old equity markets: asset price variation is burdensome to explain (even ex-post) with anything else than other prices. In this light, my result, obtained for the young and wilder market without using any price time series, is quite satisfying. I show that fundamental news has a causal impact on future returns, thus confirming the fundamental information role in cryptocurrency price formation. At the same time, I show that Bitcoin investors mildly diverge in their opinions on the new fundamental information.

I present an algorithm to perform a semi-supervised news classification. The SBERT network allows to transform each text into a 768-dimensional embedding vector, and thus the usual algebraic operations could be applied to it. In particular, one is able to find the distance between the embeddings of a given news article and a pre-specified text, which leads to a natural classification rule. (…) The news dataset is scraped from the website cointelegraph.com. This website is consistently rated among the top-3 cryptocurrency news websites and is currently ranked as the No1 website covering blockchain and crypto assets. As of March 2022, this website averages 17 million views per month, while its close competitor coindesk.com reaches around 13 million.4

The price dataset consists of 77 monthly observations. Bitcoin entered February 2015 with a price slightly above 220 USD/BTC, and slowly rose to reach the 1’000 USD/BTC level at the beginning of 2017. Then the first Bitcoin boom happened: the cryptocurrency increased 19-fold within one year and peaked at 19’783 USD/BTC on the 17th of December 2017. After a rapid crash in winter 2018 a period of relative oblivion and stagnation followed. In 2020, Bitcoin came back to the stage light and reached a price level of 40’000 USD/BTC in early January 2021. It peaked at all-time high level of 64’000 USD/BTC in April 2021 and then rapidly crashed. Bitcoin monthly return during the period of interest averages 6.5% per month, with the standard deviation being around 21%. The returns exhibit slightly negative skewness and slightly negative excess kurtosis.

Even though some research follows the Adaptive Markets Hypothesis (Lo, 2004) and shows that Bitcoin market becomes more efficient with time (López-Martín et al., 2021), the consensus states that this market is still quite inefficient. (…) IS THERE A FUNDAMENTAL VARIATION? (…) Around 16.5% of the return time series is explained by the fundamental factors on the monthly level. Exogenous news has causal power on Bitcoin returns as this type of news reveals information about the coin fundamentals. (…) ARE ALL NEWS CREATED EQUAL? (…) The topic with the largest causal explanatory power is Adoption. This topic is closely followed by Macroeconomic situation.

I notice that the store of value function consistently receives more attention from the investors than the medium of exchange. Interestingly, the patterns are quite different for the first and second Bitcoin rallies: while at the end of 2017 both functions received a quite similar amount of the attention, the 2020-2021 rally demonstrates the clear dominance of the store of value function, as presented on the figure 4.2. This result is in line with the idea that investors are concerned about inflation and government spendings fueled by the COVID-19 pandemic. (…) The store of value is a dominating function of money for Bitcoin investors.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend