How Olympic Games Impact Stocks?

Summer Olympics are a major event that attracts attention from the moment the host country is announced. However, that’s not shocking. The Olympics require a lot of planning, infrastructure building and investments. Still, countries battle for the opportunity to host these events. Undoubtedly, hosting the Olympics is prestigious, helps tourism, and many even argue that it also helps the domestic economy despite the costs of hosting. Therefore, it is natural to expect that the Tokyo Olympics should impact the domestic stock market.

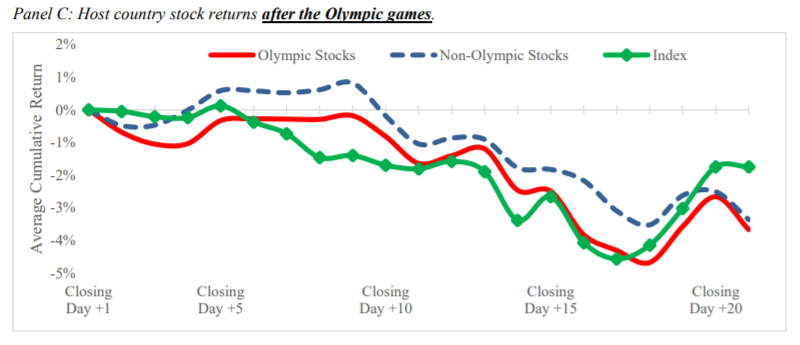

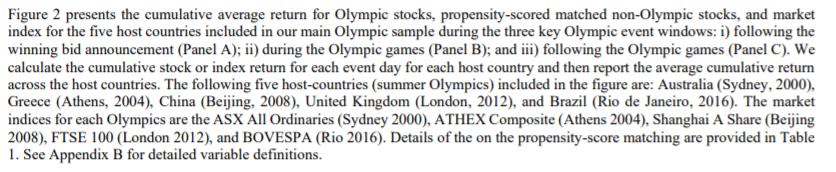

Given the games in Tokyo that are taking place right now, the novel research paper by Dechow et al. (2021) sheds light on this current topic. The authors show that the Olympics affect the stock market in numerous ways right after the announcement of the winning bid to host the games. Based on data connected with past games in Sydney, Athens, Peking, London, and Rio, there are several crucial implications. Firstly, the stock market indices rise at the time of announcement. Secondly, Olympic stocks – stocks identified as connected to the Olympics by media, social media, or sponsors/partners outperformed other non-Olympic matched stocks. Moreover, this higher valuation seems to be permanent and persists even after the games. Lastly, there is a larger co-movement among Olympic stocks with each other and also with the stock index. Nonetheless, the co-movement does not persist and is reversed after games.

Authors: Patricia M. Dechow, Alastair Lawrence, Mei Luo and Ventsislav Stamenov

Title: Media Attention and Stock Categorization: An Examination of

Stocks Hyped to Benefit from the Olympics

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3881333

Abstract:

We investigate whether there are temporary valuation impacts on stocks that media outlets list as involved in a major sporting event (the summer Olympics). We examine five summer Olympics and identify stocks that media outlets hype as benefiting from the Olympics (Olympic stocks). We find that Olympic stocks exhibit increases in comovement of returns after the announcement of the winning bid and declines in comovements after the games are played, consistent with the Olympics being used by investors as a category for investment. Furthermore, Olympic stock returns outperform their matched counterparts over this time period. If the comovement and valuation benefits are due to changes in underlying economics then we expect to observe corresponding increases in comovements of fundamentals and improvements in profitability. However, we find no observable changes in fundamental comovements or profitability. Consistent with investor sentiment driving the categorization, we find that Olympic firms with a greater retail investor presence have stronger comovements effects; and trading volume and volatility are abnormally high for Olympic firms on days where media outlets have stories linking the firm to the Olympic games. To clarify event-based categorization occurs in other settings where media outlets classify stocks for investment, we show comovement increases for stocks classified as “Stay-at-Home” by analysts and the media and “Meme” by retail investors on the Reddit social media platform.

As always we present several interesting figures:

Notable quotations from the academic research paper:

“The media coverage of megasports events is extensive with advertising revenues generating large profits for broadcasting networks. In this paper, we focus on five summer Olympics and examine whether the hype and excitement concerning these mega-sports events have spill-over effects into equity valuations. Specifically, we investigate whether investors use the Olympics as a way to identify and classify stocks for investment. We investigate whether the excitement and visibility of the Olympics pushed by the media impact the equity valuations of host-country firms that are expected to benefit from the Olympics (hereafter, “Olympic stocks”). Olympic stocks include those in the airline, construction, hospitality, media, and service industries that either directly or indirectly contribute to the broader Olympic experience.

If investors then infer from this good economic news provided by experts, that certain stocks are likely to disproportionately benefit (those involved in the Olympics), then this news can create new demand for such stocks irrespective of how much the firms actually benefit from the Olympics. Second, the Olympics are an interesting news story for people in hosting countries. Prior to the Olympic games, the media gives frequent updates on the construction progress being made towards the Olympics, gives estimates on the number of tourists that will visit, and discusses other benefits of the games. The media also frequently combines news of the Olympics with the performance of the stock market discussing which companies are likely to benefit and even makes specific lists of such Olympic stocks. This greater media focus is likely to increase investor attention on Olympic stocks and potentially bias them towards selecting these stocks for investment.

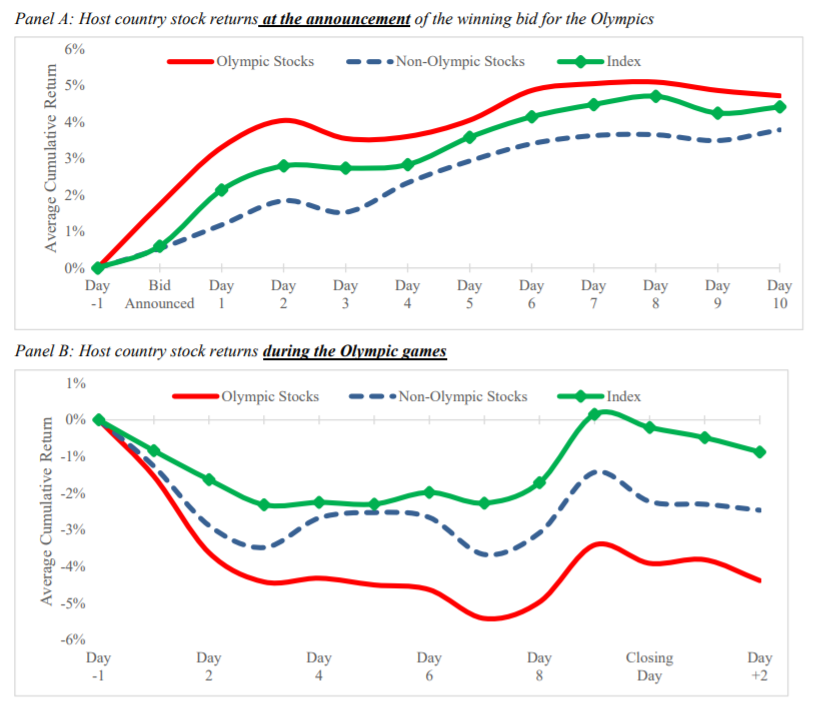

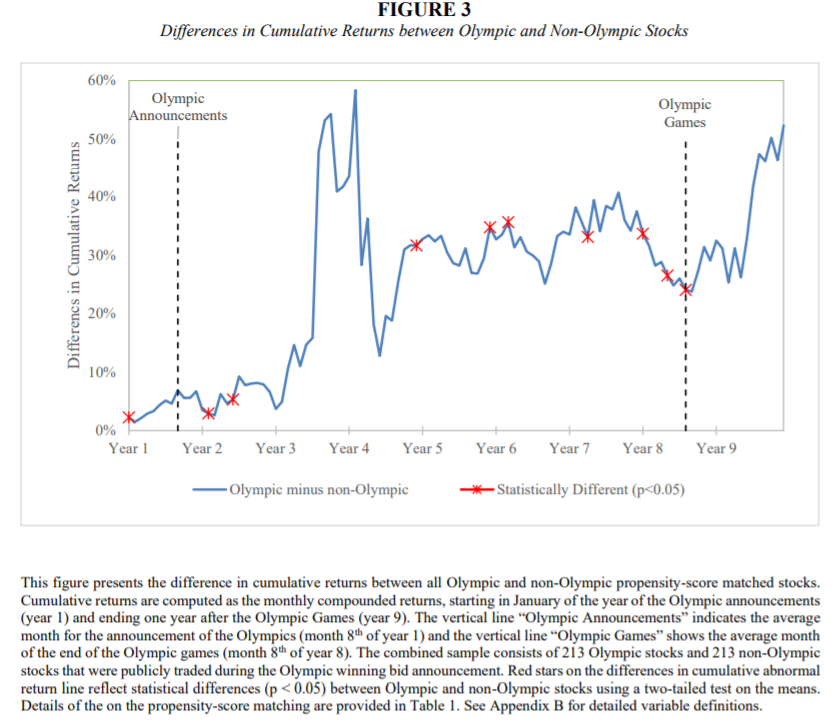

We investigate the pricing of Olympic stocks in five Olympic-hosting countries: Australia (Sydney 2000), Greece (Athens 2004), China (Beijing 2008), the United Kingdom (UK) (London, 2012), and Brazil (Rio, 2016). We classify a stock as an “Olympic stock” as follows. First, we use national and local media, depending on the country, to identify mentions of stocks expected to be involved in or benefit from the Olympic games. Second, we searched investing and social media sites for lists of Olympic theme stocks. Third, we identify all official Olympic sponsors and partners that were publicly traded in the host-country. The main sample across these five Olympics consists of 213 Olympic stocks that were publicly traded as of the Olympic winning bid announcement with 37 Sydney Olympic stocks, 41 Athens Olympic stocks, 60 Beijing Olympic stocks, 60 London Olympic stocks, and 15 Rio Olympic stocks.

Consistent with investors viewing the Olympics as having a positive economic benefit to the hosting country, we document that stock market indices rise at the time that the winning bid is announced. There is a seven-year period between the time that a country first learns that it has successfully won a bid to host the Olympics to the playing of the Olympic Games (we term this the Olympic time period). We find that over the Olympic time period, the stocks that media outlets classify as being involved in the Olympics have positive cumulative returns and outperform their matched counterparts by approximately 25 percent. The valuation benefits appear to be permanent since we do not observe them dissipating after the

Olympic games are played.

We next investigate whether the Olympic classification by the media results in categorization of these stocks by investors. Our first measure of comovement is the average R-squared from firmspecific regressions of Olympic firm returns on an index comprising of all Olympic firms. We find that across the five Olympics, the average R-squared increases by 21.7 percent from the preannouncement period to the year of the Olympic Games with a quick increase in comovement around and after the winning bid announcement which is largely sustained until the Olympic Games. However, consistent with the categorization hypothesis, we find a complete reversal in the increase in R-Squared within the year after the games are played.

Our third measure of comovement attempts to control for general trends in stock synchronicity. This measure is based on the average betas from firm-specific regressions of an Olympic firm’s stock return on an Olympic Index and a non-Olympic Index. We find that the beta on the Olympic Index increases after the winning bid announcement by approximately 10 percent and continues to increase to approximately 27 percent by the year of the Olympic games while the beta on the non-Olympic Index decreases by over 35 percent over this same period.

After establishing the stock market impact of the Olympics, we investigate whether these effects are also reflected in underlying firm fundamentals. We find no evidence of abnormal profitability or growth for Olympic firms during the Olympic period. Earnings and revenues of Olympic stocks are similar to those of matched firms in all periods leading up to and during the Olympic year. In addition, we find little to no evidence that fundamentals (earnings or revenues) of Olympic stocks comove with each other more strongly during the Olympic period. The lack of results for fundamentals could be due to us having low power tests since data is only available on a quarterly or semi-annual basis. However it could also be the case that the Olympics games do not result in detectable levels of abnormal profitability or fundamental comovement risk since (i) the Olympic games only last 16 days; and (ii) Olympic firms come from a variety of industries and so differ in the timing of benefits and risks associated with the Olympics (e.g., a construction firm’s profits will depend on the negotiated contract earned before the games, whereas hotels and restaurants profits are dependent on tourism and are earned around the time of the games); and (iii) the press and more recently, social media outlets are the source of the classification of firms benefiting from the Olympics and not the firms themselves.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend