How to Select the Best Commodity CTAs

A new academic paper related to our previous blog-post (Benchmarking Commodity CTAs):

Authors: Blocher, Cooper, Molyboga

Title: Performance (and) Persistence in Commodity Funds

Link: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2658153

Abstract:

This study documents persistent, net-of-fees, alpha-generating commodity trading advisor funds focused on commodity investment (“Commodity Funds”). The baseline for performance measurement is a new benchmark model that includes factors established in the literature. A nonparametric bootstrap test establishes the existence of alpha that cannot be explained by luck. Performance persists 12 months out of sample and subsequently disappears. Such performance, without a reversal, indicates that persistent alpha is based in information about fundamentals, not fund flows or sentiment. These results are robust to data biases established in the literature.

Notable quotations from the academic research paper:

"To evaluate fund manager performance, we first implement and test a five-factor asset pricing model as a benchmark for commodity manager performance measurement. The model includes a market factor, a time series momentum factor, a spot basis factor, and high and low term premia factors. These factors are drawn from the extant literature, based in commodity fundamentals, and each has been shown separately to capture a risk premium embedded in commodity futures (e.g., Szymanowska et al. 2014, Bakshi, Gao Bakshi, and Rossi 2014, Moskowitz, Ooi, and Pedersen 2012). This factor model for commodity futures parallels Fama and French’s now ubiquitous model for publicly traded equities (now also with five factors, see Fama and French 2015).

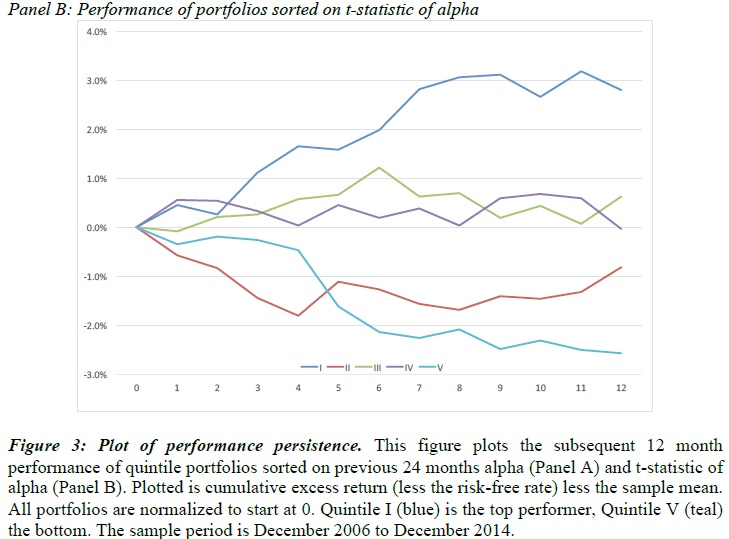

We then use this five-factor model benchmark to identify commodity fund manager performance and persistence. First, we conduct a bootstrap analysis of the distribution of alpha t-statistics and find both top and bottom performers that cannot be explained by luck. Second, we find that both good and bad performance persists for approximately 12 months. Annualized alpha of the top performing quintile is 2.53%, while the same for the bottom performing quintile is -1.94%. This performance persistence disappears after 12 months, but does not reverse. This nonreversal indicates that commodity fund manager performance is based on information and/or skill, rather than sentiment or other non-fundamental factor, which is often the case in mutual funds (Blocher 2015, Lou 2012).

"

"

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend