How to Value Overvalued MicroStrategy?

MicroStrategy has become one of the most polarizing companies in public markets. Once a conventional business intelligence firm, it has transformed into the world’s largest publicly traded Bitcoin proxy, holding over a million BTC on its balance sheet and continuously raising capital to buy more. Supporters praise it as a visionary “Bitcoin ETF with leverage,” while critics argue it is an irrationally overvalued vehicle whose market capitalization regularly trades far above the fair value of its underlying assets. The persistent premium — the gap between MicroStrategy’s equity value and the market value of its Bitcoin holdings — has puzzled analysts, defied traditional valuation logic, and raised the question: why does this spread exist, and why does it not close through arbitrage? A recent academic paper, Valuing MicroStrategy, offers a structural model that explains this phenomenon and sheds light on how the firm’s unique financing mechanics allow its stock price to exceed the value of its assets.

The paper provides a rigorous lens into how speculative dynamics surrounding corporate Bitcoin exposure challenge conventional finance theory. The authors situate MicroStrategy’s equity within the literature on limits to arbitrage, showing that equity markets can sustain persistent mispricings even when debt markets remain disciplined. By embedding these dynamics into a structural valuation model, they reveal how the interaction between corporate financing capacity and speculative sentiment generates a new intangible asset: a “financing franchise.” This framework underscores the complexity of modern valuation, where firms tethered to volatile digital assets like Bitcoin can trade at levels that systematically diverge from fundamental benchmarks, reshaping our understanding of corporate finance in hype‑driven regimes.

In effect, the analysis suggests that MicroStrategy’s equity need not be intrinsically “overvalued,” even though its market capitalization trades at more than a 50% premium relative to the mark‑to‑market value of its Bitcoin holdings. Instead, the firm’s issued debt appears systematically overpriced, reflecting over‑optimistic pricing by creditors. Because these debt instruments are not readily shortable, arbitrageurs cannot enforce convergence. Consequently, MicroStrategy effectively monetizes the mispricing by extracting rents from debt investors, thereby financing its long‑horizon Bitcoin accumulation strategy through the optimism embedded in its own credit spreads.

Main findings summarized:

The first resounding finding is the identification of a persistent wedge between the market capitalization of MicroStrategy’s equity and the fair value of its Bitcoin holdings, a wedge that conventional arbitrage arguments cannot rationalize. The model posits that debt markets remain disciplined—arbitrageurs enforce near-fair pricing of credit instruments—yet equity markets are susceptible to speculative amplification. This asymmetry underscores a profound limit to arbitrage: while rational investors can short debt or demand higher yields, equity overvaluation persists because shorting constraints, coordination frictions, and the option-like payoff structure of equity collectively prevent convergence. The implication is that equity markets can sustain valuations that systematically exceed asset values, not due to irrationality per se, but because the financing channel itself becomes an intangible asset.

The second significant contribution lies in formalizing the notion of a “financing franchise” as an endogenous asset class. During hype states, the firm can issue debt at a premium to fundamental value, effectively transferring wealth from new creditors to incumbent shareholders. This mechanism generates a positive feedback loop: the more overvalued the equity, the greater the firm’s capacity to extract rents from debt issuance, which in turn justifies higher equity valuations. The authors’ structural model captures this recursive dynamic and demonstrates its empirical consistency with MicroStrategy’s observed market data. Beyond the case study, the framework generalizes to any corporate entity whose valuation is tethered to volatile, sentiment-driven assets, thereby offering a rigorous lens through which to analyze the complexity of modern financial markets where speculative financing equilibria destabilize traditional valuation anchors.

Authors: Sandro C. Andrade, Brian Coomes, and Diogo Duarte

Title: Valuing MicroStrategy

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5434457

Abstract:

Bitcoin treasury stocks present a novel situation in which a firm’s assets and equity are traded independently. Surprisingly, the market value of equity can at times be significantly larger than the market value of assets. We build a continuous–time structural credit model to replicate this pattern, assuming the firm is able to issue new debt at a premium to fair value during a “hype state”, thereby violating Modigliani-Miller conditions. This violation creates a “financing franchise”‘ owned by shareholders that can be valuable enough to push the market value of equity above the market value of the assets. Our model is consistent with data showing that limits to arbitrage bind for MicroStrategy’s debt but not for its equity.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

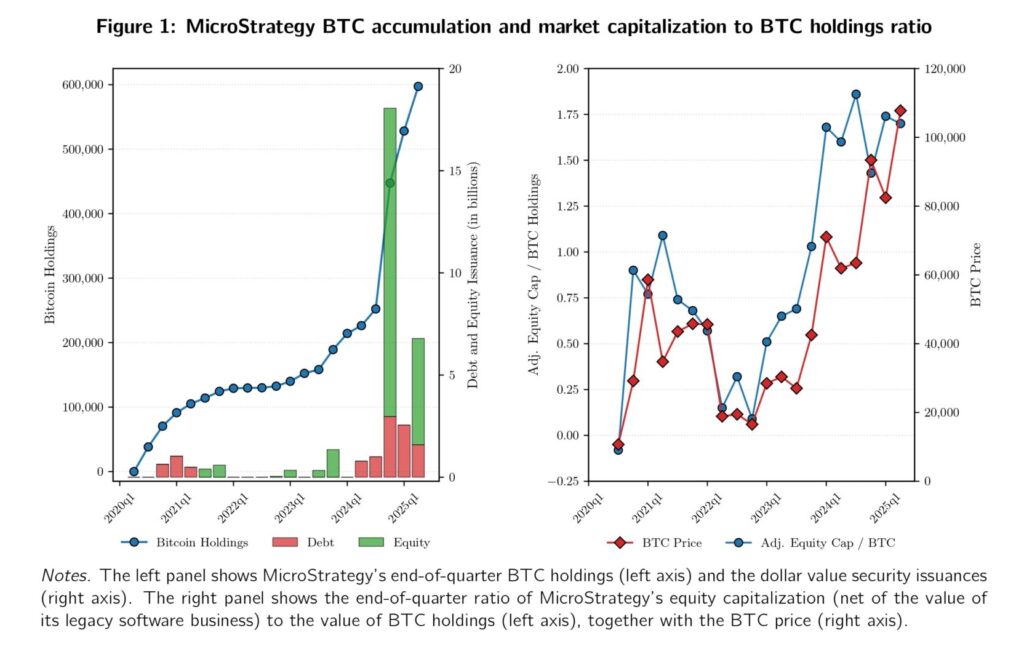

“MicroStrategy’s business model presents an unusual situation in corporate finance for two reasons. First, unlike regular businesses, the market value of the firm’s assets is observable: the quantity of BTC held multiplied by BTC’s price. Second, in blatant violation of Modigliani-Miller propositions, MicroStrategy’s equity market capitalization can be significantly higher than the market value of its assets. For example, at the end of 2025Q2, the market value of BTC holdings was $64.4 billion and the firm had over $10 billion of outstanding debt, while its equity market capitalization was $110.5 billion.1 This 50+ billion gap would be a contender for the largest mispricing across a pair of securities ever documented.

Figure 1 illustrates the (apparent) overvaluation of MicroStrategy’s equity relative to Bitcoin. Panel (a) shows MicroStrategy’s BTC accumulation along its funding sources over time. Panel (b) shows the equity-to-assets ratio (solid blue line), defined as the (adjusted) market value of equity divided by the market value of their BTC holdings, alongside the BTC price (dashed red line) over the same period.2 The figure shows that the ratio climbs persistently above 1 after 2023Q4, reaching 1.7 in 2025Q2.

Figure 3 shows that the net financing cost for MicroStrategy’s equity is persistently negative and very close to minus a standard money-market rate over the period. In other words, MicroStrategy stock was cheap to short during throughout the entire period, consistent with Figure 2. Moreover, Figure 3 shows that the cost of shorting MSTR’s stock fluctuated very little, again consistent with Figure 2.

[Authors] develop a continuous-time model to value MicroStrategy, the pioneering “Bitcoin treasury stock”. We show how a Modigliani-Miller violation — the ability to sell overpriced bonds to invest in fairly priced securities while the market in a hype state — creates an intangible asset whose value can make the market value of equity exceed the market value of the firm’s (tangible) assets. In our model, the firm is continuously selling fairly priced equity and overpriced debt to expand its balance sheet in favorable terms to shareholders (old and new). The model helps explain why MicroStrategy’s equity capitalization was persistently higher than the value of its BTC holdings from 2023Q4 to 2025Q2, a discrepancy that reached 70% and more than $50 billion. Consistent with our assumptions, data on the cost of shorting securities indicate that, from 2023Q4 to 2025Q2, the limits to arbitrage are binding for MicroStrategy’s debt, but not for MicroStrategy’s equity.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend