How to Combine Commodity Style Strategies

How should investor weight commodity strategies in his portfolio? Is it better to use simple approach or some sophisticated weighting scheme?

Authors: Fernandez-Perez, Fuertes, Miffre

Title: Harvesting Commodity Styles: An Integrated Framework

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3005347

Abstract:

This paper develops a portfolio allocation framework to study the benefits of style integration and to compare the effectiveness of alternative integration methods in commodity markets. The framework is flexible enough to be applicable to any asset class for either long-short, long- or short-only styles. We study the naïve equal-weighted integration and sophisticated integrations where the style exposures are sample-based by utility maximization, style rotation, volatility-timing, cross-sectional pricing or principal components analysis. Considering the “universe” of eleven long-short commodity styles, we document that the naïve integration enhances each of the individual styles in terms of their reward-to-risk tradeoff and crash risk profile. Sophisticated integrations do not challenge the naïve integration and the rationale is that, while also achieving multiple-style exposures, the equal-weighting approach circumvents estimation risk and perfect-foresight bias. The findings hold after trading costs, various reformulations of the sophisticated integrations, economic sub-period analyses and data snooping tests inter alia.

Notable quotations from the academic research paper:

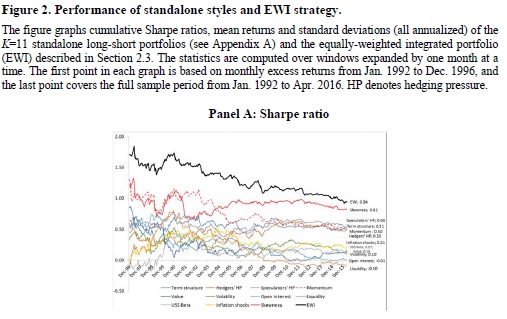

"Recent studies have shown a lot of long-short style portfolios that are able to capture a premium – the most notably based on backwardation and contango, past performance, net short hedging and net long speculation, liquidity, open interest, inflation beta, dollar beta, value, volatility or skewness signals.

Instead of “putting all the eggs in one basket” (i.e., adopting one of the commodity investment styles mentioned above), the present paper is concerned with the idea of forming a long-short commodity portfolio that has exposure to many styles. Style integration has a strong economic appeal. By relying on a composite variable that aggregates information from various signals, the investor ought to predict more reliably the subsequent asset price changes. Relatedly, an integrated portfolio should benefit from signal diversification in the form of less volatile excess returns. For the above reasons, one may readily agree that style integration is a sensible approach that may improve performance relative to standalone style portfolios. This, however, begs the question: How do we integrate K styles at asset level (i.e., within a unique portfolio)? Specifically, how shall we decide the weights that the integrated portfolio allocates to each of the individual styles?

This paper makes three contributions to the style integration literature.

Our first contribution is to propose a simple, yet versatile, framework to conduct style integration. The proposed integration framework accommodates many variants pertaining to: i) the scoring scheme to rank the N assets according to each of the individual styles, and ii) the weighting scheme for the K individual styles (or the style exposures). The proposed framework is very flexible as it is applicable to long-only, short-only, as well as long-short investment styles, for any asset class. This contribution addresses an important goal of the paper which is to provide academics and practitioners with a well-structured way to blending multiple asset characteristics to improve

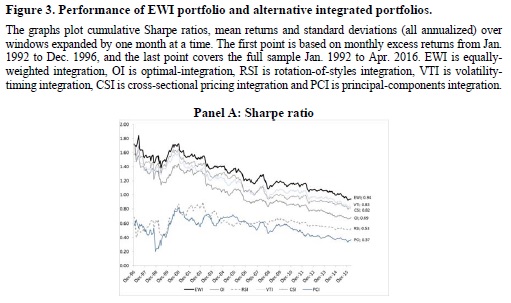

portfolio allocation. The framework proposed nests many integration methods. We formulate a naïve integration with time-constant, equal-weights for all styles (Equal-Weighted Integration; EWI), and various ‘sophisticated’ approaches with time-varying and heterogeneous style exposures determined by different criteria.

Our second contribution is to illustrate the flexibility of the integration framework by deploying the aforementioned strategies to the “universe” of styles in commodity futures markets in order to ascertain which integration method is most effective in practice. To our knowledge, no prior study (for any asset class) has conducted such a comparison of alternative style-integration approaches. Furthermore, there is a dearth of research on style integration in commodity futures markets. Our findings suggest that the naïve EWI portfolio stands out by generating very attractive reward-to-risk ratio profile (Sharpe, Sortino and Omega ratios) and lowest crash risk (downside volatility, 99% Value-at-Risk, and maximum drawdown) that is not challenged by the standalone portfolios nor the sophisticated integrated portfolios. The failure of the latter to outperform the EWI portfolio suggests that the benefits from allowing time-varying and heterogeneous exposures to the K styles are offset by estimation risk and perfect-foresight bias.

Our final contribution is to add to the debate as to whether holding the EWI portfolio is equivalent to investing a fraction 1/K of wealth into each of K independently-managed style portfolios. The EWI portfolio can be thought of as an “aggregate-then-invest portfolio” while the 1/K approach, also called portfolio mix, is an “invest-then-aggregate portfolio”. This debate has been confined to long-only equity styles thus far and we contribute to it by comparing theoretically and empirically the Sharpe ratio of both integration approaches for long-short commodity styles. We show that, even before transaction costs, the EWI portfolio achieves a higher reward per unit of risk than the portfolio mix because the latter randomly fails to fully invest the clients’ mandate.

"

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend