Music Sentiment and Stock Returns around the World

There was a time in history when researchers believed that we, as a human species, act ultimately reasonably and rationally (for example, when dealing with financial matters). What arrived with the advent of Animal spirits (Keynes) and later Behavioral Finance pioneers such as Kahneman and Tversky was the realization that it is different from that. We often do not do what is in our best interest; quite the contrary. These emotions are hardly reconcilable with normal reasoning but result in market anomalies.

Researchers love to find causes and reasons and link behavioral anomalies to stock market performance. A lot of anomalies are related to various sentiment measures, derived from a alternative data sources and today, we present an interesting new possible relationship – investors’ mood and sentiment proxied by music sentiment!

This study introduces a novel measure of investor sentiment, which captures actual sentiment rather than shocks to sentiment. The main result from (Edmans et al., 2021) is a positive and significant relation between music sentiment and contemporaneous market returns, controlling for world market returns, seasonalities, and macroeconomic variables.

Interestingly, they also found a significant price reversal the following week. Taken together, their findings are consistent with sentiment-induced temporary mispricing that subsequently reverses. A battery of validation tests shows that seasonal factors, such as mood-decreasing months, cloud cover increases, and COVID-related restrictions, are associated with a significant decrease in their music-based sentiment measure. The relationship between music sentiment and market returns is stronger when countries implement trading restrictions such as short-sale bans during the COVID-19 pandemic, consistent with more significant limits to arbitrage.

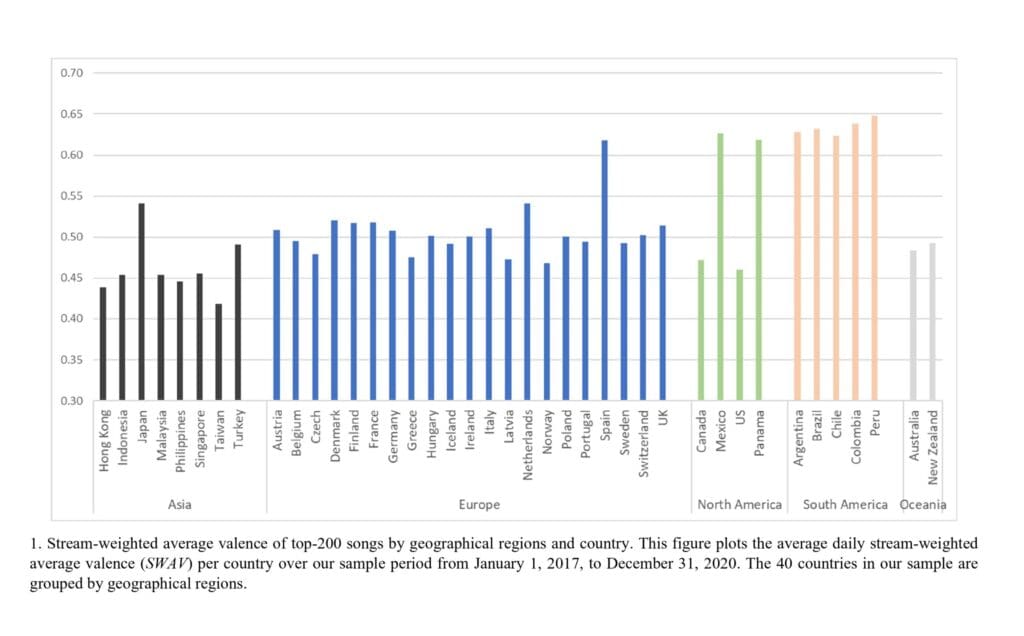

Fig. 1 shows a chart of the full sample average SWAV [stream-weighted average valence] across countries. Music sentiment also predicts increases in net mutual fund flows and decreases in government bond returns, and absolute sentiment precedes a rise in stock market volatility. Overall, our study provides evidence that a proxy for the actual sentiment of a country’s citizens is significantly correlated with asset prices.

Authors: Alex Edmans, Adrian Fernandez-Perez, Alexandre Garel, and Ivan Indriawan

Title: Music Sentiment and Stock Returns Around the World

Link: https://ssrn.com/abstract=4057537

Abstract:

This paper introduces a real-time, continuous measure of national sentiment that is language-free and thus comparable globally: the positivity of songs that individuals choose to listen to. This is a direct measure of mood that does not pre-specify certain mood-affecting events nor assume the extent of their impact on investors. We validate our music-based sentiment measure by correlating it with mood swings induced by seasonal factors, weather conditions, and COVID-related restrictions. We find that music sentiment is positively correlated with same-week equity market returns and negatively correlated with next-week returns, consistent with sentiment-induced temporary mispricing. Results also hold under a daily analysis and are stronger when trading restrictions limit arbitrage. Music sentiment also predicts increases in net mutual fund flows, and absolute sentiment precedes a rise in stock market volatility. It is negatively associated with government bond returns, consistent with a flight to safety.

As always, we present several impressive figures and tables:

Notable quotations from the academic research paper:

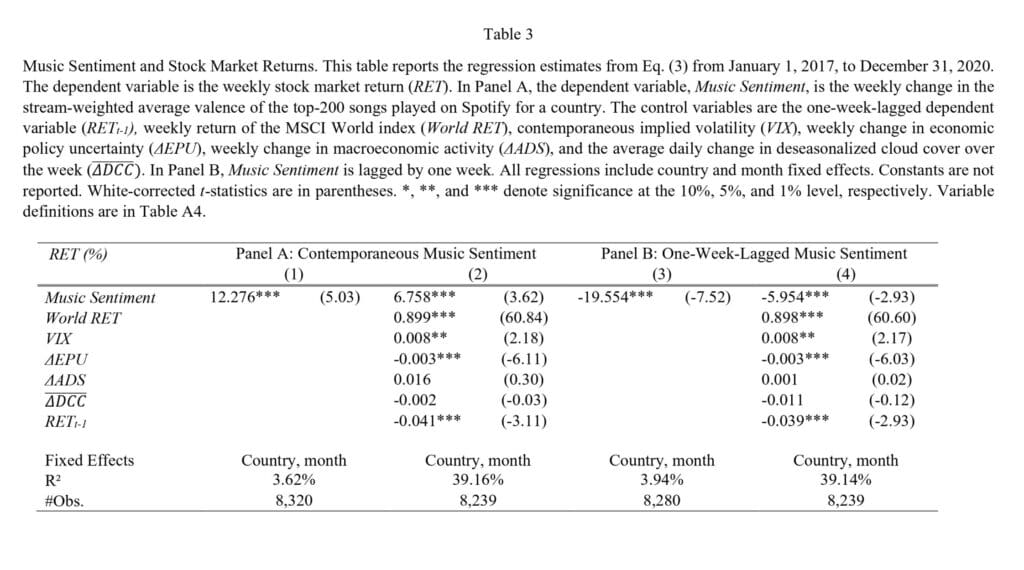

“Our main analyses investigate the relation between music sentiment and stock market returns. We find a positive and significant association between music sentiment and contemporaneous returns, controlling for past returns, the world market return, seasonalities, weather conditions, and macroeconomic variables. A one-standard-deviation increase in music sentiment is associated with a higher weekly return of 8.1 basis points (bps), or 4.3% annualized. This effect reverses over the next week: a one-standard-deviation increase in music sentiment predicts a lower next-week return of 7.0 bps or -3.7% annualized. Both results are consistent with sentiment-induced temporary mispricing, and prior theoretical and empirical findings that negative investor sentiment causes prices to temporarily fall but subsequently correct (De Long et al., 1990; Baker and Wurgler, 2006, 2007; Edmans, Garcia, and Norli, 2007; Ben-Rephael, Kandel, and Wohl, 2012).

We obtain similar results with a daily analysis – music sentiment is associated with significantly higher contemporaneous stock returns, which subsequently reverse. Our results hold for both dollar and local currency returns, when excluding one country at a time to ensure that they are not driven by a specific country, and when excluding the 50 most-streamed songs per country to address the concern that Spotify suggests songs to users.

Our music-based sentiment measure also involves subjectivity, since the valence algorithm was initially trained based on experts’ opinion. However, the sentiment measure applies to songs all over the world, which increases comparability. While equivalent words in different languages have different meanings, music is less equivocal: as is often emphasized, “music is a universal language.” Mehr et al. (2019) study 315 cultures and find that they use similar kinds of music in a similar context, suggesting music has universal properties that likely reflect commonalities of human cognition throughout the world. Thus, a measure of song valence is likely to be applicable globally. Moreover, music captures ineffable emotions that a word-based sentiment measure cannot.

This paper is also related to studies investigating high-frequency proxies of sentiment using non-textual sources. Obaid and Pukthuanthong (2021) estimate sentiment in the U.S. through a sample of editorial news photos. Like them, we study a measure that may convey sentiment more effectively than words, but an audio rather than visual one. Our analysis also differs by considering an endogenous measure of mood, studying 40 countries, and analyzing equity fund flows and government bond returns in addition to stock returns.

Finally, our study is part of a new stream of literature using big data in finance. Music sentiment satisfies the three features of big data identified by Goldstein, Spatt, and Ye (2021). It is large in size, aggregating the listening behavior across all Spotify listeners with a country every day. It is high dimension, as a song has multiple characteristics that feed into its valence measure. It is also unstructured, requiring an algorithm to assess its positivity. All three features mean that music streaming is an aggregate measure of consumption available at high frequency, whose positivity can be assessed to form a proxy for national sentiment.

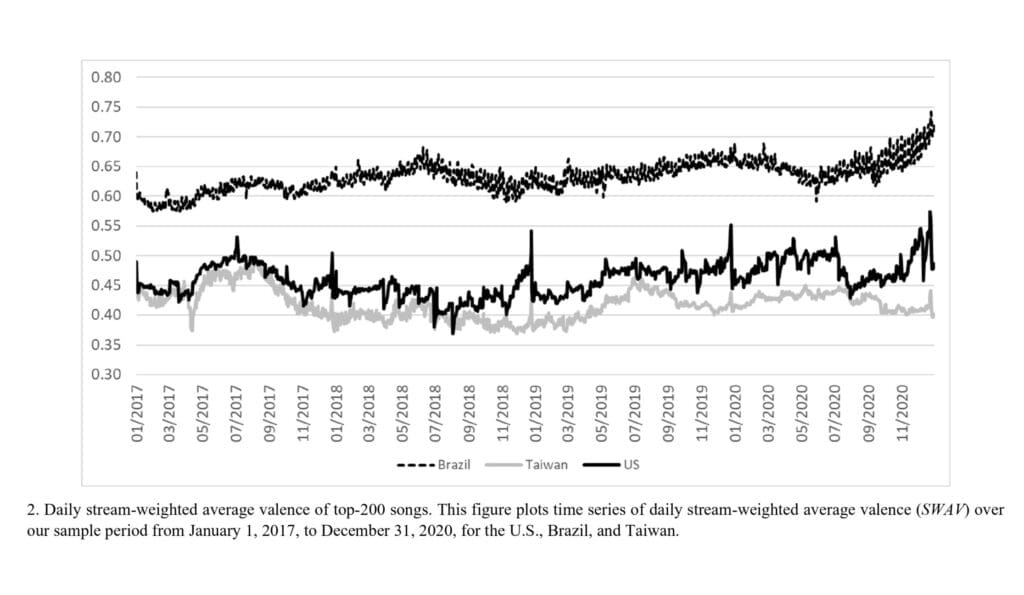

We observe that South American countries have a higher average SWAV, whereas Asian countries have a lower average SWAV. Fig. 2 plots daily SWAV over time for three countries: US, Brazil (which has one of the highest average SWAV), and Taiwan (which has one of the lowest). Although SWAV is persistent, it also exhibits variations over time that we can exploit to construct a music-based sentiment measure. The coefficient of variation (standard deviation divided by the mean) of daily SWAV is 5.5% when computed separately for each country and then averaged. The persistence of SWAV means that our music-based sentiment measure is based on changes in SWAV.

To match our music sentiment measure with stock market and macroeconomic data, we aggregate it at a weekly level to avoid non-synchronicity between the opening and closing times of the stock markets and the time of day that Spotify reports its daily statistics. Such non-synchronicity would lead to a daily measure of SWAV partially leading daily stock returns for some indices and lagging it for others. We define our sentiment measure as the weekly change in sentiment, both to control for country-level differences in the average level of sentiment, as shown in Figure 1, and also because we expect the change in sentiment to cause changes in stock prices.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend