Predicting Stock Market Performance with the Global Anomaly Index

Today’s article focuses on investigating long-short anomaly portfolio return predictability in international stock markets, which often undergo mispricing due to investors’ sentiment. A paper by Jiang, Fuwei et al. (Apr 2023), suggests using the AAIG (Global Anomaly Index) and it examines the ability of the aggregate anomaly index to predict future returns in 33 stock markets. While previous research finds that a high aggregate anomaly measure predicts a low return in the U.S. market, this study further demonstrates that the global component of AAI (aggregate anomaly indices) is the key that drives international return predictability and reveals that the global anomaly index is a strong and robust predictor of equity risk premiums not just in the U.S. market but also in international markets, both in- and out-of-sample, consistently delivering significant economic values.

The predictive power is driven by globally widespread stronger mispricing correction persistence for overpricing relative to underpricing and partly by the predictive ability to forecast future sentiment changes. Controlling for a range of variables, the global anomaly index exhibits a strong and persistent power to predict international market excess returns.

The dataset utilized in this study consists of 33 MSCI DM and EM markets and covers the sample period between January 1990 and December 2021. Estimating aggregate anomaly indices (AAI) of international markets is based on Dong, Li, Rapach, and Zhou (2022) ’s simple average approach. The authors employ a cross-sectional average of 153 long-short anomalies (a description of the 153 anomalies can be found in Table A1) portfolio returns as the proxy of the aggregate anomaly index for each market. The global anomaly index (AAIG) is then estimated as the first principal component of these aggregate anomaly series. Finally, each market’s local anomaly index (AAIL) is estimated as the residual of its aggregate anomaly index regressed on the global anomaly index. The return data is value-weighted in U.S. dollars, and each market’s monthly excess returns are calculated relative to the one-month U.S. treasury bill rate.

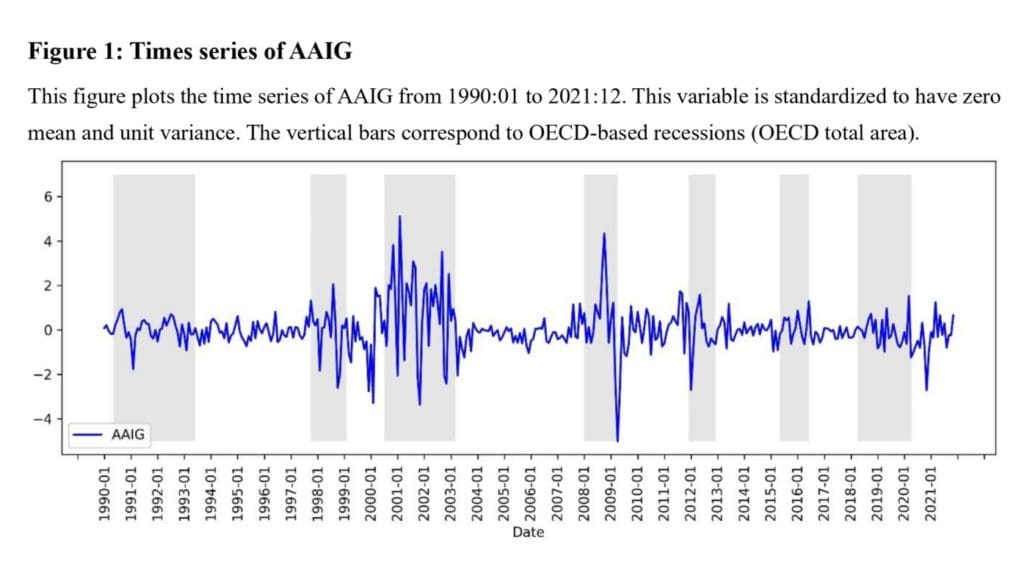

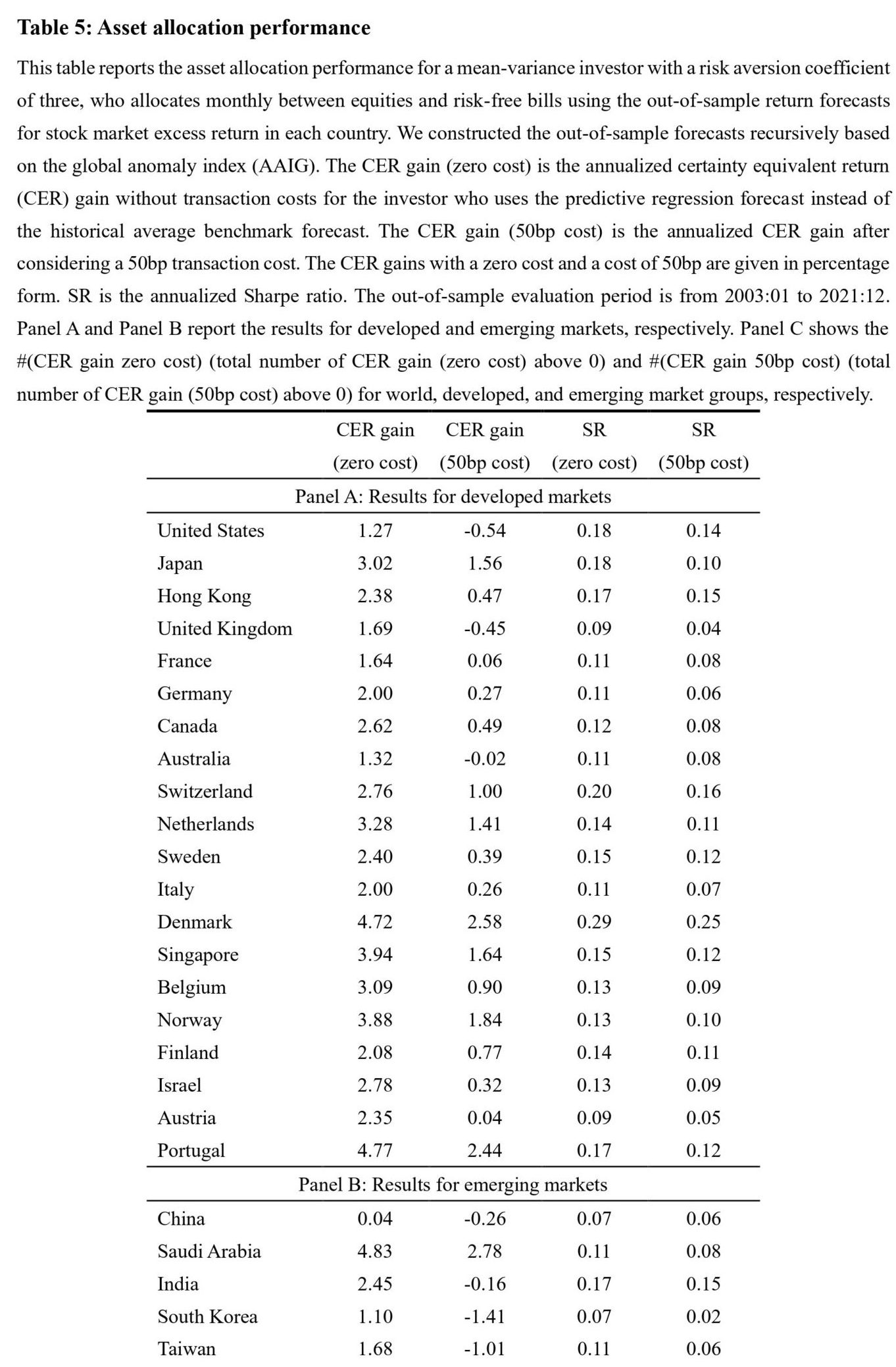

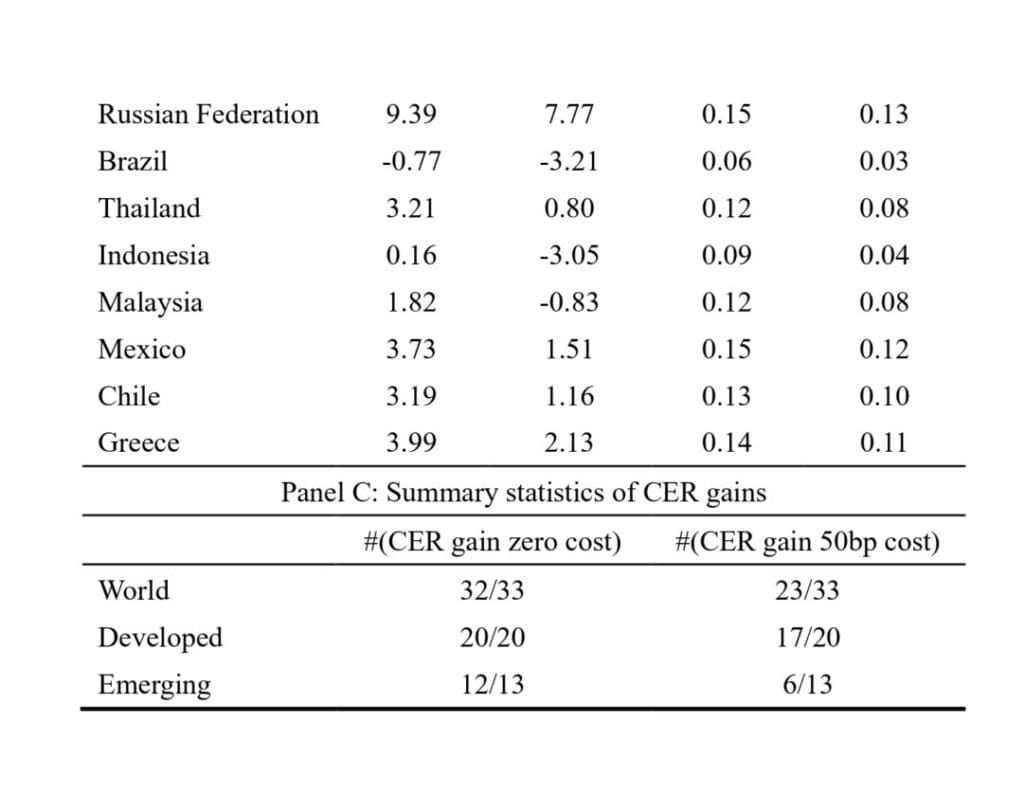

Figure 1 displays the time-series plot of AAIG from 1990:01 to 2021:12, along with the OECD-based recession (OECD total area) indicator. Authors find that AAIG is more volatile around recessions. The components of the AAI orthogonal to the AAIG are defined as local anomaly indices (AAIL). In each market, they regress the aggregate anomaly indices on the global anomaly index and generate local anomalies as residuals. Table 5 reports the asset allocation performance of the AAIG in terms of the CER gain and SR. Overall, the CER gains are positive for 32 of the 33 markets. In Table 5, Panel A, shows the CER gains are positive for all 20 developed markets, ranging from 1.27% (United States) to 4.77% (Portugal) for a risk aversion parameter of three. In Table 5, Panel B, they find that the CER gains are positive for 12 of the 13 emerging markets, ranging from 0.04% (China) to 9.39% (Russian Federation).

Authors: Fuwei Jiang, Hongkui Liu, Guohao Tang, Jiasheng Yu

Title: Global Mispricing Matters

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4384265

Abstract:

This paper constructs a global anomaly index based on the 153 long-short portfolio returns of 33 stock markets. We find that global anomaly index is a strong negative predictor of future aggregate stock returns in international markets both in- and out-of-sample. It captures the common changes in overpricing across stock markets, and is not subsumed by the extant well-known stock return predictors. The predictive power of global anomaly index arises from globally widespread stronger mispricing correction persistence for overpricing relative to underpricing, and partly from the predictive ability to forecast future sentiment-changes. We provide evidence that global mispricing is an important pricing factor for predicting aggregate stock returns around the world.

And, as always, we would like to point out the most important figures and tables:

Notable quotations from the academic research paper:

“Prior literature has found a variety of predictors for forecasting future aggregate stock returns. As discussed in Rapach and Zhou (2021), the return predictability documented in the literature can be explained by two potential explanations: (1) rational risk-based explanations consistent with market efficiency, predominantly related to macroeconomic fundamental predictors in much of the earlier literature; 1 (2) market inefficiencies (i.e., security mispricing) resulting from behavioral biases and information frictions, related to the predictors in recent literature, including short interest, options, corporate activity and ESG, technical indicators, and sentiment.2 Recently, Dong, Li, Rapach, and Zhou (2022) reveal a negative pattern between aggregate long-short anomaly portfolio returns and future stock market returns in the U.S. market, which implies the stock mispricing is an important pricing factor in aggregate stock return predictability. However, it remains unclear whether similar patterns exist outside the U.S. In this study, we examine the international predictability of aggregate anomaly measures and identify the key source of its predictive power.

We follow Dong, Li, Rapach, and Zhou (2022) to construct aggregate anomaly indices (AAI, hereafter) for 33 markets, including 20 developed markets and 13 emerging markets. AAI is obtained by averaging 153 long-short anomaly portfolio returns in cross-section, and an aggregate shrinkage approach is to filter the idiosyncratic noise for each anomaly. However, we use simple averaging instead of more advanced shrinkage methods like Principal Component Analysis (PCA) and Partial Least Squares (PLS) due to the missing financial data issue, which is a widespread issue as discussed in Bryzgalova, Lerner, Lettau, and Pelger (2022) and Freyberger, Höppner, Neuhierl, and Weber (2021). 3 Many anomaly data are missing, especially in the early part of the sample, and the missingness patterns vary across markets. The implementation of PCA and PLS requires complete anomaly data in the timeseries. The practice of using cross-sectional means for padding or directly removing the missing variables, may result in a large bias. Simple averaging, in contrast, is suitable for our study as it does not require each anomaly data to be complete in the time-series.

Empirically, we demonstrate that, over the sample period of 1990:01 to 2021:12, AAIG is a robust contrarian predictor of market excess returns around the world. Specifically, in 30 out of the 33 markets examined (including 18 out of the 20 developed markets and 12 out of the 13 emerging markets), the one-month horizon regression slopes on the global anomaly index are significantly negative at the 10% level or better. Furthermore, we find that local component of aggregate anomaly measures is not effective for forecasting future international market excess returns.

Overall, our finding reveals that global component of the AAI is the key factor for forecasting future international market excess returns. In contrast, both the market-level aggregate and local idiosyncratic anomaly measures have limited predictive ability of stock returns.

Our findings indicate that the predictive ability of AAIG remains robust even when constructed with different market groups. Additionally, we find that AAIG exhibits stronger predictability during periods of business cycle recessions in international markets. Furthermore, our analysis suggests that the fluctuations of AAIG are linked to the financial uncertainty and sentiment.

In summary, our findings reveal that AAIG has a strong predictive power for the market excess returns around the globe, while the predictive power of AAI and AAIL is limited. Our finding suggests that AAIG is the primary driving force of the international return predictability. It is likely that the predictive power of some AAI is due to their ability to capture the predictive power of AAIG.

The results indicate that the predictive power of AAIG is not subsumed by local economic and financial conditions, U.S. spillover effects, market fear and rare disaster concerns, or global economic policy uncertainty. Furthermore, our result suggests that AAIG is among the most comprehensive predictors of international returns, forecasting in almost the largest number of markets.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend