Dear readers,

We have two new announcements we would like to start with:

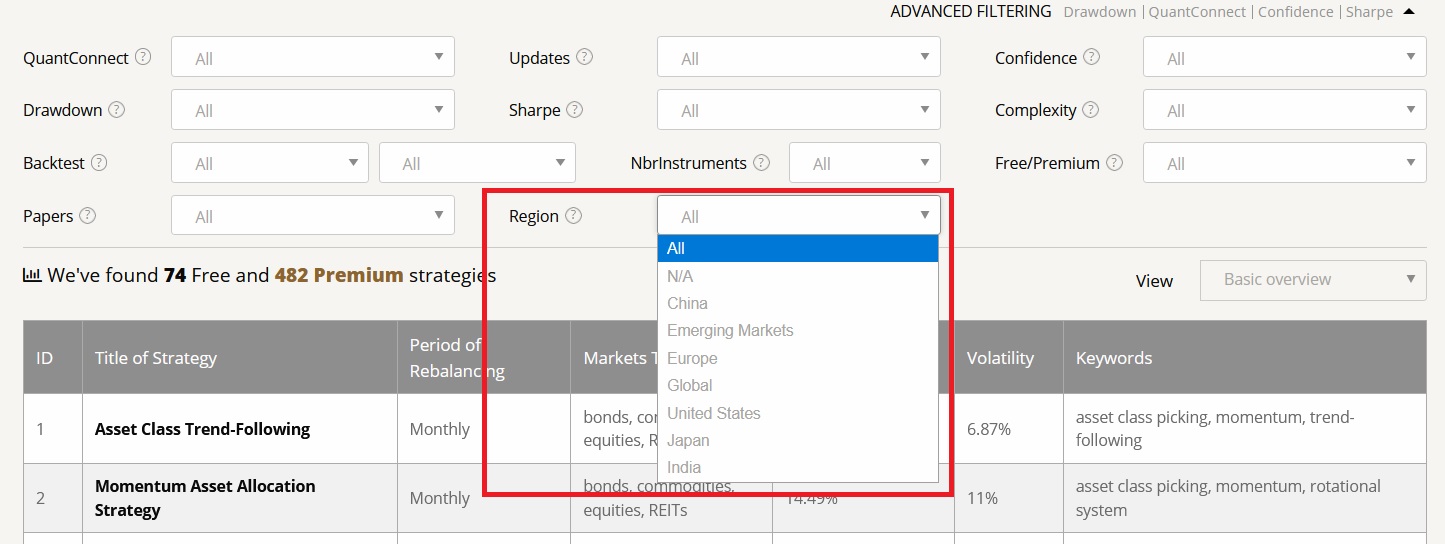

- We have listened to our audience and have prepared a new filtering field which you can use to screen strategies by regional focus. We also received a significant number of requests to analyze research which is focused on strategies from emerging markets (especially China and India). We would therefore increase the number of strategies analyzed every month and use that spare capacity to add also strategies which are not trading only the US financial markets.

- Plus we continue to re-run some of our codes on a monthly basis systematically, 100 codes are at the moment part of this activity. We expect that number to increase to 200 at the beginning of December. You can use a new field in our Screener to filter such strategies with periodic updates.

And now, let us recapitulate last month of Quantpedia’s research. Thirteen new Quantpedia Premium strategies have been added into our database, and eleven new related research papers have been included in existing Premium strategies during last month.

Additionally, we have produced 12 new backtests written in QuantConnect code. Our database currently contains nearly 370 strategies with out-of-sample backtests/codes.

Also, five new blog posts, that you may find interesting, have been published on our Quantpedia blog:

Resurrecting the Value Premium

Authors: Blitz, Hanauer

Title: Resurrecting the Value Premium

The Daily Volatility of Foreign Exchange Rates and The Time of Day

Authors: Doman, Doman

Title: How Does the Daily Volatility of Foreign Exchange Rates Depend on the Time of Day at Which the Daily Returns Are Calculated?

The Knapsack problem implementation in R

Author: Padysak

Title: The Knapsack problem implementation in R

Not all Gold Shines in Crisis Times – COVID-19 Evidence

Authors: Baur, Trench

Title: Not all Gold Shines in Crisis Times – COVID-19 Evidence

Implied Volatility Indexes for European Government Bond Markets

Authors: Baran, Vorisek

Title: Volatility indices and implied uncertainty measures of European government bond futures

Plus, we have a new short video about using Quantpedia as an inspiration.

Stay safe …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend