Resurrecting the Value Premium

Nowadays, the value factor is a hot topic among practitioners and researchers as well. It is commonly known that equity factors have a cyclical performance, but many argue that value underperforms for too long. Therefore, many say that the classical HML value factor of Fama and French is dead. On the other hand, there is an emerging amount of research papers that study the value investing with an aim to make some alterations. These would result in a profitable factor, as the classic B/M ratio looks like it’s not a sensible value factor anymore. This branch of literature was recently enriched by novel research of Blitz and Hanauer (2020). By including more value metrics, altering the investment universe and applying basic risk management techniques, value strategy can become profitable in the long term. Although the modification is sensible, it stills suffer in a recent period. Only time will tell whether the novel resurrected value factors would emerge again as many times in the past…

Authors: David Blitz and Matthias X. Hanauer

Title: Resurrecting the Value Premium

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3705218

Abstract:

The prolonged poor performance of the value factor has led to doubts about whether the value premium still exists. Some have noted that the observed returns still fall within statistical confidence intervals, but such arguments do not restore full confidence in the value premium. This paper adds to the literature by showing that the academic value factor, HML, has not only suffered setbacks in recent years but has, in fact, been weak for decades already. However, we show that the value premium can be resurrected using insights that are well documented in the literature or common knowledge among practitioners. In particular, we include more powerful value metrics, apply some basic risk management, and make more effective use of the breadth of the liquid universe of stocks. Although our enhanced value strategy also suffers in recent years, it has a solid long term track record that does not warrant existential concerns. We conclude that a healthy value premium is still clearly present in the cross-section of stock returns.

Notable quotations from the academic research paper:

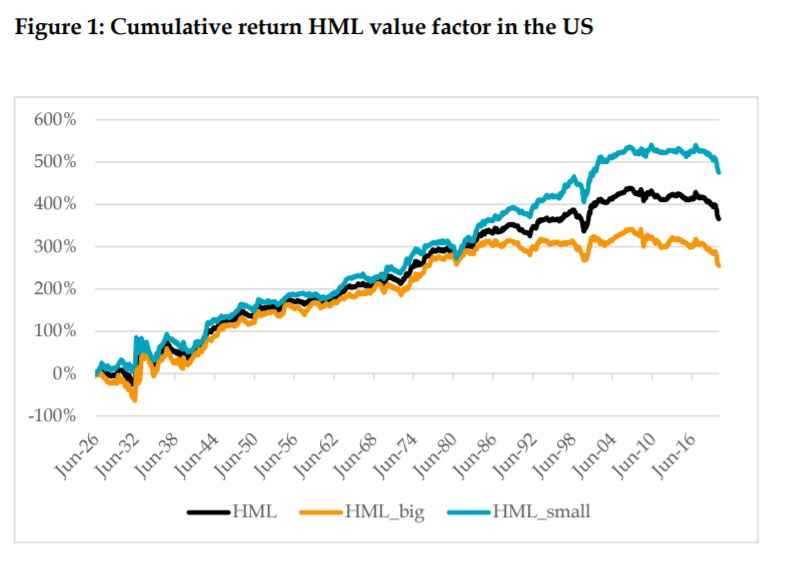

“This paper adds to the existing literature by showing that the academic value factor, HML, has not only suffered setbacks in recent years, but has in fact been struggling for decades already. Performance in the big-cap space, which covers 90% of the total market capitalization, is particularly weak. Thus, concerns that the value premium may have disappeared, or is at least seriously impaired, do not appear unreasonable. The CMA investment factor, which is effectively the academic substitute for the HML value factor, has not fared much better.

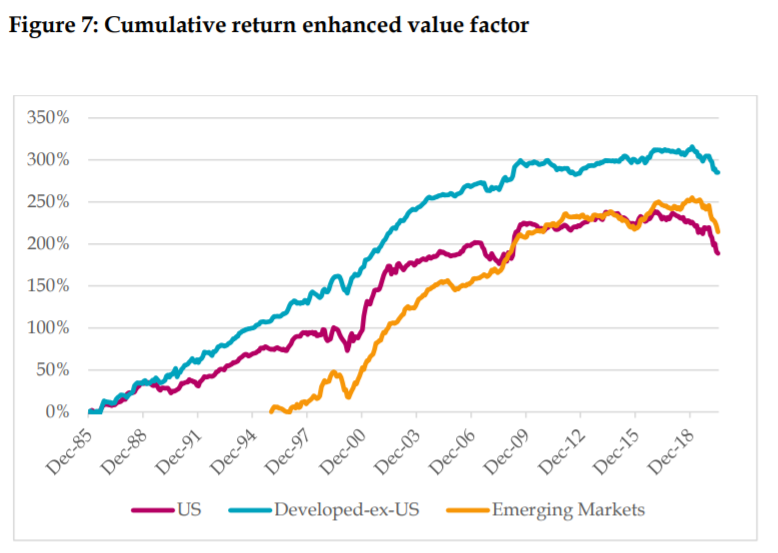

Our resurrected value factor uses insights that are well documented in the literature or common knowledge among practitioners. Most importantly, we use a composite of value metrics, we apply some basic risk management techniques, and we make more effective use of the breadth of the liquid universe of stocks. We conclude that, with a little bit of effort, a healthy value premium can still be discerned in the cross-section of stock returns. Thus, investors should not jump to the conclusion that the value premium is gone based merely on the weak performance of the generic HML factor. The underperformance of the enhanced value factor in the final years of the sample can be attributed to an extreme widening of valuation multiples last seen at the height of the tech bubble in the late 1990s. In light of this multiple widening we also note that the ‘true’ magnitude of the value premium may be underestimated over our sample period, and that the forward-looking expected return on value versus growth is currently higher than average.”

The composite value metrics are best described in the following section:

“Our first alternative metric is the EBITDA/EV ratio, which stands for earnings before interest, taxes, depreciation, and amortization to enterprise value. It is also known as the Enterprise Multiple. Loughran and Wellman (2011) show that EBITDA/EV has a strong performance in the US market, which is not explained by traditional factors such as HML, and Walkshäusl and Lobe (2015) extend these results to international markets. Gray and Vogel (2012) also identify EBITDAto-EV as one of the most powerful value metrics. The EBITDA-to-EV ratio can be seen as an enhanced version of the classic earnings-to-price ratio, which is not affected by non-operating

gains or losses, less susceptible to accounting leeway with depreciation and amortization, and also independent of the capital structure of the firm. Such enterprise multiples have also been popular among practitioners, as described in Souzzo et al. (2001). Our second additional metric is the cash-flow-to-price ratio (CF/P). By using information from the cash-flow statement of firms, this factor complements the B/M and EBITDA/EV metrics that are based on the balance sheet and income statement, respectively. Our third and final additional metric is net payout yield (NPY), which was first documented by Boudoukh et al. (2007) for the US market, and later

corroborated by Walkshäusl (2016) for international markets. Net payout yield is essentially dividend yield, plus share buybacks, minus share issuance. Share buybacks and issuance are related to the asset growth that is used for the investment factors of Fama and French (2015) and Hou, Xue, and Zhang (2015) discussed in the previous section. Share buybacks and issuance also reflect the firm’s management view on share valuation, as described in Jenter (2005) and Bali, Demirtas, and Hovakimian (2010). Following Park (2019), Lev and Srivastava (2020), Arnott et al. (2020), and Amenc, Goltz, and Luyten (2020), we also make a small adjustment to the B/M ratio itself by capitalizing R&D expenses. Moreover, we compute all value metrics using the most recent price, following Asness and Frazzini (2013). We create a composite value score by first normalizing each individual metric cross-sectionally using standard robust z-scores, capped at +3 and -3, and then averaging these scores. Since two of our four value metrics, EBITDA/EV and CF/P, are not meaningfully defined for financials, we remove the stocks from this sector in our empirical tests.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend