Systematic Hedging of the Cryptocurrency Portfolio

Introduction

Cryptocurrencies are already one of the major asset classes. They fill the top pages of magazines and are a topic of a day to day conversation. There are a lot of ways to buy them through a lot of different channels. But some of the hardcore HODLers like to keep their coin portfolio safe – they buy a portfolio of cryptocurrencies and hold them in cold storage. It has a lot of advantages (you will probably not become a victim of hacking if your crypto coins are in cold storage in your wall safe) but also some disadvantages (your cold storage device can become unreadable or destroyed). One of the disadvantages of cold storage is that while you hold the cryptocurrencies in your cold storage, you are exposed to the price swings of the cryptocurrency market (which can be tremendous). But do you need to have this risk, especially when the market is at an all-time high? What if you smartly hedged a portion of your portfolio? The goal of this article is to serve as an inspiration for a hedging strategy for your cold storage cryptocurrency portfolio. We do not say this is the only way to run a hedging strategy, but we would like to inspire you to start thinking about this possibility even when you have not considered it yet. Are you ready? Then let’s go 🙂

Setup

Imagine you want to permanently store the top 5 alts (altcoins) in a soft/hardware wallet and find an optimal hedging strategy through BTC derivatives to minimize crypto market beta exposure risk. How do we best approach that?

We have created a hypothetical market capitalization-weighted Top 5 cryptocurrency index portfolio (T5) as a proxy for a portfolio; hard-core HODLers may hold that. We now do not deal with the task of picking individual coins into your portfolio. That’s the topic that is covered in entirely different articles (see, for example, our list of research articles related to cryptocurrency trading or our database entries with cryptocurrency trading strategies).

The rule for inclusion in the index is simple. Each year, on the first day of the year, select 5 top coins ranked by market cap for a yearly holding period. Include them in the index based on market cap weight (thus proportionally). We exclude the stablecoins from the index as the goal of the cold wallet is to hold the true cryptocurrency coins. So, the following coins can’t be part of the portfolio:

| Tether | USDT |

| USD Coin | USDC |

| Binance USD | BUSD |

Data

CoinMarketCap. In daily granularity, we select a span from 2015 to have enough data for further investigation. Here, we list coin ranks at the corresponding year start:

| rank / year | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| 1 | BTC | BTC | BTC | BTC | BTC | BTC | BTC | BTC | BTC | – |

| 2 | XRP | XRP | ETH | XRP | XRP | ETH | ETH | ETH | ETH | – |

| 3 | XPY | LTC | XRP | ETH | ETH | XRP | XRP | BNB | BNB | – |

| 4 | LTC | ETH | LTC | BCH | BCH | BCH | LTC | SOL | XRP | – |

| 5 | BTS | DASH | XMR | ADA | EOS | LTC | DOT | ADA | DOGE | – |

| Bitcoin | BTC |

| XRP | XRP |

| PayCoin | XPY |

| Litecoin | LTC |

| BitShares | BTS |

| Ethereum | ETH |

| Dash | DASH |

| Monero | XMR |

| Bitcoin Cash | BCH |

| Cardano | ADA |

| EOS | EOS |

| Polkadot | DOT |

| BNB | BNB |

| Solana | SOL |

| Dogecoin | DOGE |

Methodology

The top 5 index is constructed in such a way as to mimic the B&H (buy & hold) approach, often favored by both individual and institutional investors (but maybe in different asset classes of choice). This is similar to the construction of market cap-weighted equity indexes such as the Dow Jones Industrial Average (Dow 30, as seen on CNBC, the stock market index of 30 prominent companies listed on stock exchanges in the United States, but our index is even more concentrated).

Research Purpose

Investors in cryptocurrencies can experience crazy bubble rallies of altcoins, but brutal drawdowns (some even over -80 %) may be associated with them. This is the disadvantage of B&H portfolios in most asset classes, but cryptos are by far the most risky. Everybody wants to mitigate that B&H risk somehow; nobody likes to see their portfolio value disappear exceptionally fast, as in crypto busts. And that is where hedging arrives to (at least) a particular rescue.

There are many aspects of how something can be hedged; for our purposes, we selected a selective sequential one: We would hedge parts of the portfolio some days. The question is: how big should the hedge be, and when should it be commenced? Plus, what should be the hedge? Suspecting that there is left Bitcoin beta residual associated with other cryptocurrencies (as Bitcoin is the largest and the oldest cryptocurrency), we suppose that beta can be efficiently hedged out by Bitcoin derivatives, which may offer an antidote to drawdowns.

Results and Solution

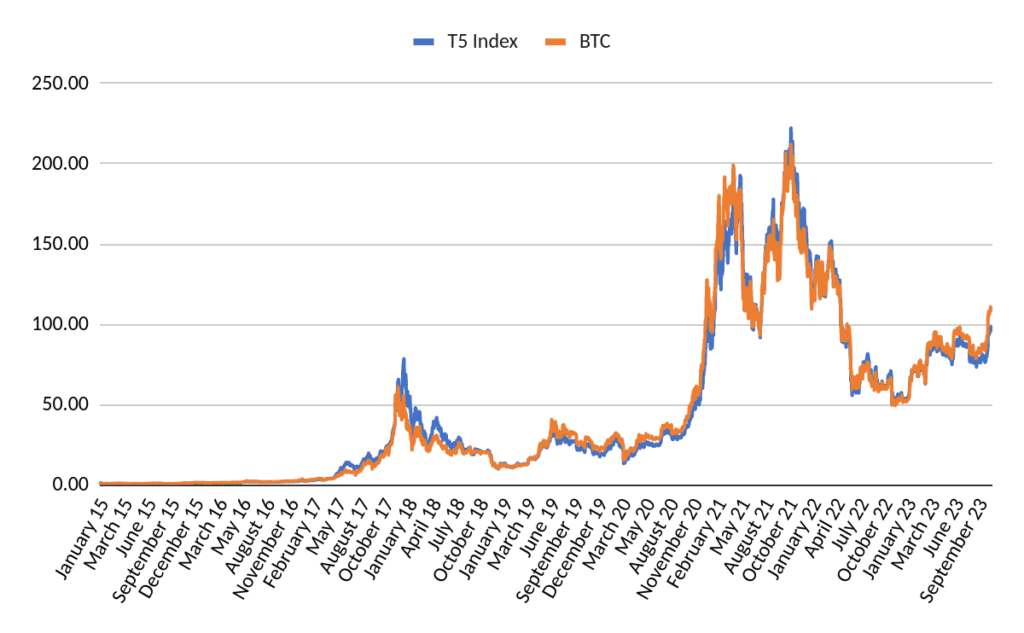

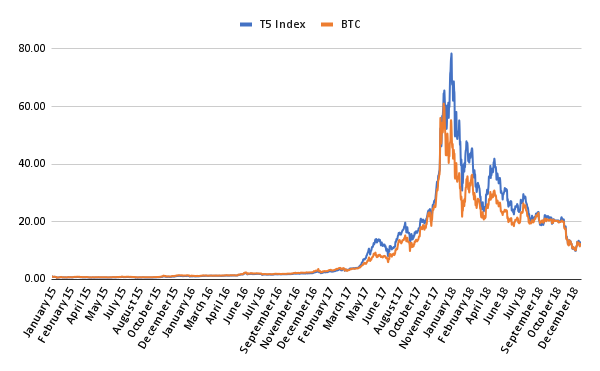

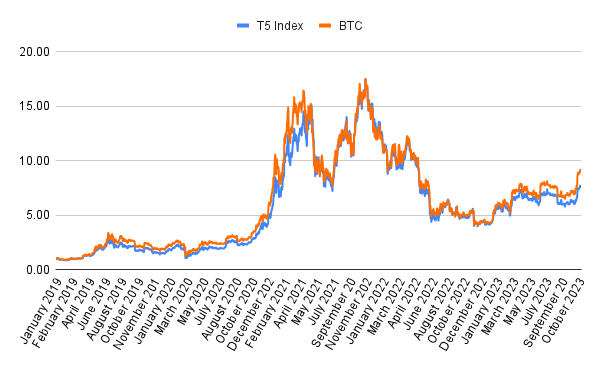

First, we would present three naive hedging solutions, review them, check the residual spread performance, and compare advantages and disadvantages. Then, we would move to the active hedging strategy. However, let’s at least show the performances of Bitcoin and our considered and constructed T5 Index for a start:

Now, onto the first one (proposed solution):

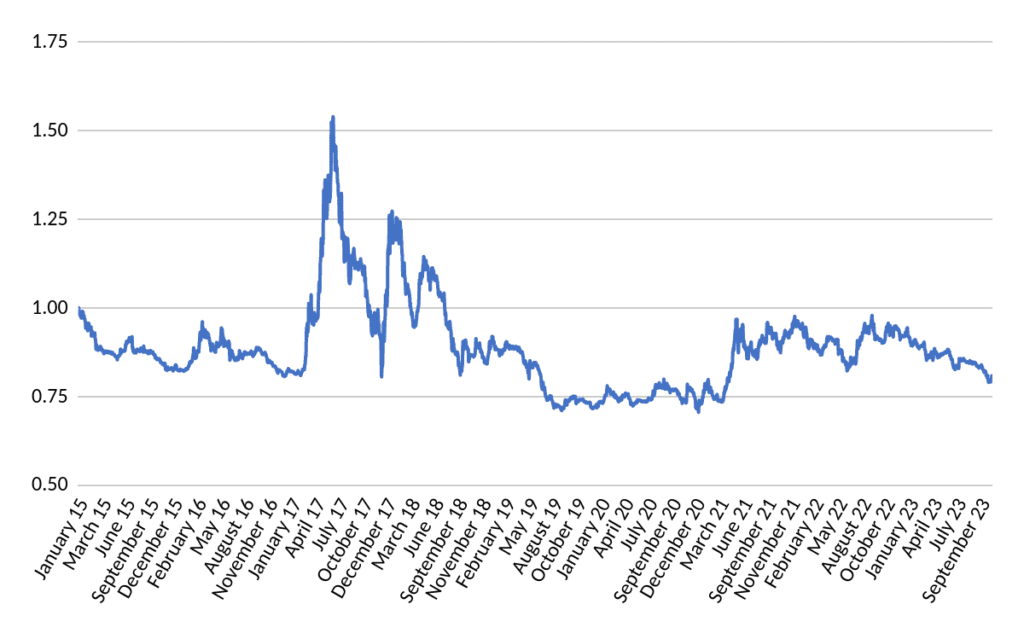

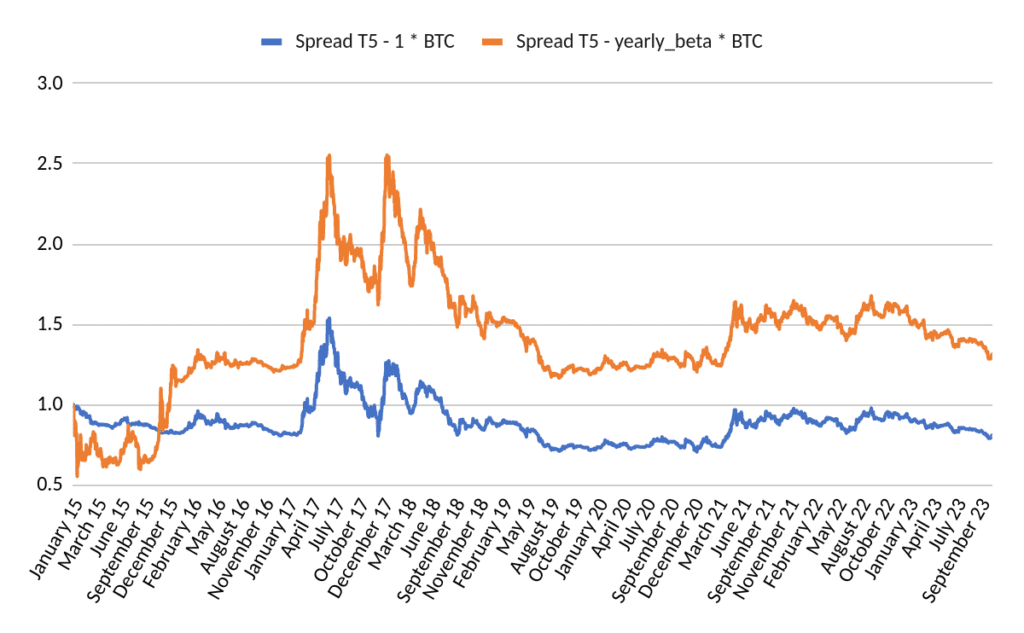

1. 1:1 (Proportional) Hedge

As introduced earlier, we are long the Top 5 Index portfolio and short the exact amount of $ value corresponding to Bitcoin (BTC).

The graph showing the performances of the spread T5 – BTC shows high volatility, especially in the years 2015, 2017, and 2018. The volatility of the spread portfolio after we naively remove the beta starts to decrease only after the year 2018.

After noticing the difference in the spread’s volatility after the year 2018, we decided to split the sample to two parts – 2015-2018 (included) and 2019-2023.

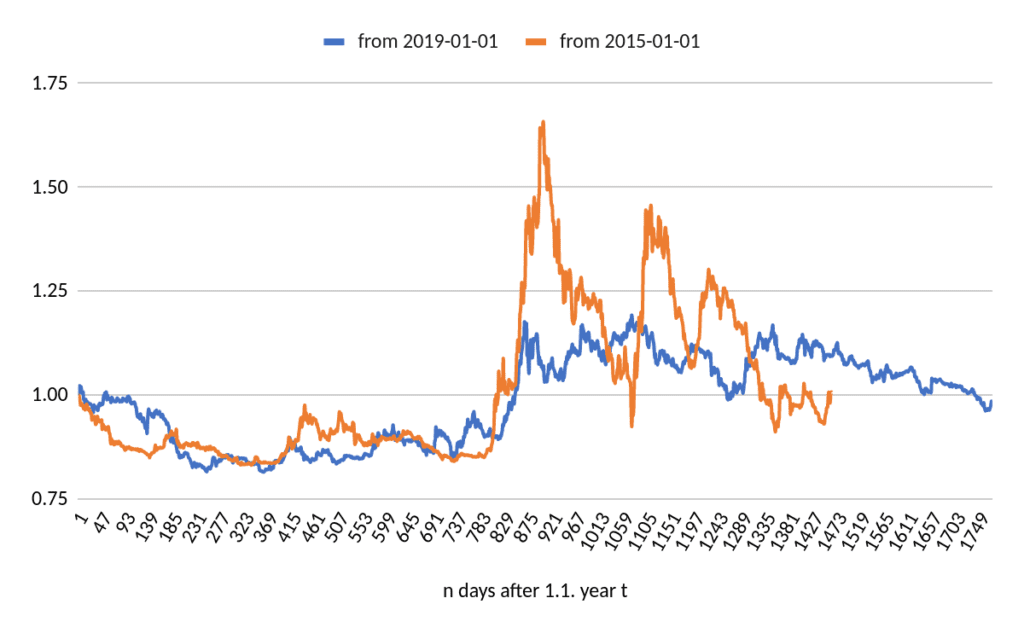

This is the comparison of the behavior of the naïvely leveraged spread over time from the start of 2015 and 2019, respectively, where x-axe depicts t days from the start of those years. After the orange line ends, it is the last day of 2018, and the blue line continues that same spread from the first day of 2019. Once again, the volatility of the spread has been considerably dampened since 2018. In the 2015-2018 window, the average yearly spread volatility was 3.94%, whereas in the later period, it was 2.48%.

Why is it so? Once again, we suspect the introduction of Bitcoin futures is the cause (as we discussed in our previous article about the optimal portion of the usual investment portfolio allocated to Bitcoin).

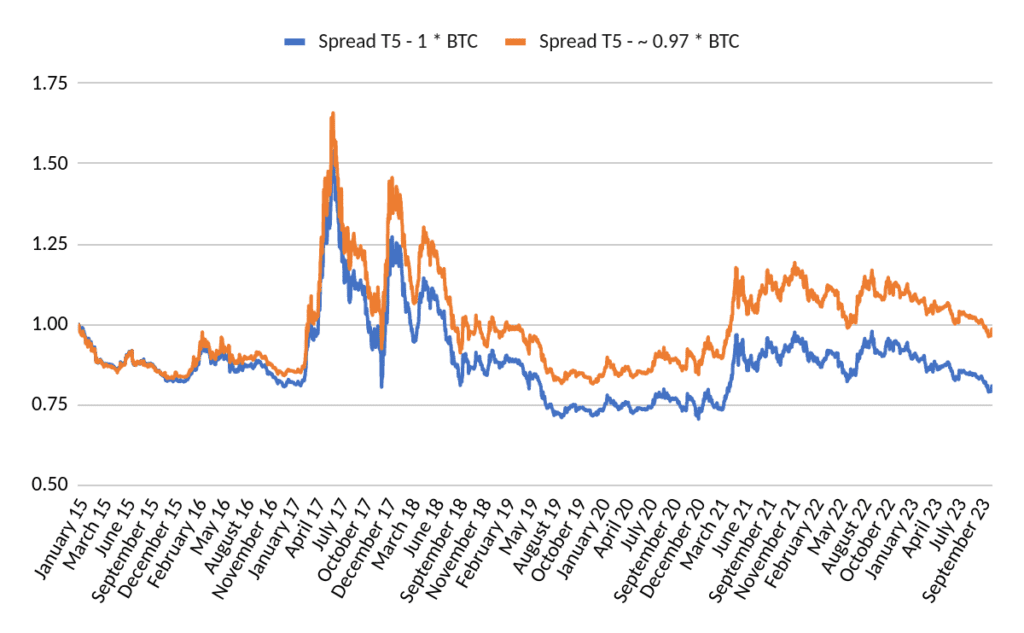

2. Regression for the Whole Period

In our 2nd attempt, we tried to run a simple OLS regression over the whole period and find out the beta coefficient. In this naïve “back-test”; the optimal beta was found to be ~ 0.97. Of course, we can’t use it in reality as in the first years, we would not know the data from the future. But still, this serves useful as a mental exercise.

The finding that surprised us was that the beta is less than 1.0, so the optimal hedging ratio would be less than $1 in the BTC futures for every $1 in the cold storage. We expected the opposite.

3. Rolling Regression

This variant is going long portfolio and hedging with BTC according to yearly regression, which gets new data, adjusts each year’s end, and rebalances accordingly on the first day of the new/next year.

The problem here is that using shorter timeframe windows gives us a lower slope, which makes us dimensionally underhedged. This leaves us with a high residual and high beta on the index, which is not optimal for our purpose.

Active hedging strategy

Ok, let’s continue. In the first part of the article, we checked some naive hedging methods to remove the portfolio beta and now we can continue and built some simple hedging strategy that stems from our older article Trend-following and Mean-reversion in Bitcoin. We will use the trend-following signal to selectively hedge the cold-storage portfolio.

So, we propose to include the following rules in a simple manner decision-if-then-tree manner:

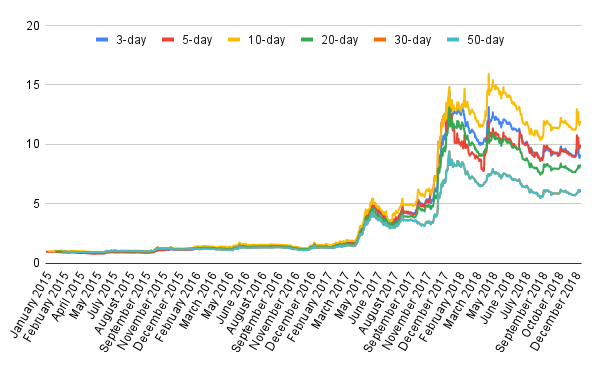

- if I am at a BTC x-day high, I prefer not to hedge cold-storage portfolio;

- if I do not fulfill such conditions, I hedge cold storage through some instrument (near-term BTC or perpetual [PERP]) futures (for the sake of simplicity, each $1 of the portfolio is hedged 1:1)

And now, finally, delve into the bread-and-butter part.

Results

Firstly, the performance of the BTC/T5 index (in cold storage) from the year 2015 to 2019 and from 2019 onwards is shown.

Secondly, let’s analyze the alternative strategy that employs the cold storage and hedges it with a BTC future with the above mentioned rules (hold cold storage without a hedge if we are at X-day high, otherwise, hedge with a BTC future)

As always, graphs and tables (from 2015 and 2019).

Since 2015

Since 2019

We can see that we can relatively successfully employ the hedging strategy and retain the majority of the returns of the cold-storage portfolio. For example, from the year 2019 until 2023, the cold storage portfolio registered a 57% gain with a 67% volatility and -a 77% drawdown. Our hedging strategies (mainly those that use the shorter X-day high signals) registered returns between 44% and 47%, with halved volatility (34-43%) and a fraction of the maximal drawdown of the passive cold-storage portfolio (-22% to -37%).

Of course, the non-hedged cold-storage portfolio would probably also have higher returns in the future. However, it would be unwise not to consider hedging at least a portion of the portfolio with BTC derivatives. A little lower returns are not a high price for a good night’s sleep.

Endings and Conclusions

The cryptocurrency market is extremely volatile, and a lot of the participants are accustomed to the wild swings in the price. However, it doesn’t make sense to tolerate that large swing all of the time when there are options for dampening the volatility of the portfolio a little. Hedging variant + cold storage provides a very good tradeoff for people who want to have crypto in their own hands, their own paper or hardware (both represent so-called cold) wallets, but on the other side, want to mitigate the most adverse effects of the price swings.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend