Three Methods to Fix Momentum Crashes

Everyone who lived during the 2007 and 2009 crisis knows what the biggest weakness of the equity momentum strategy was. It was right during the spring of 2009 when the financial markets were on its inflection point when the momentum strategy crashed. Right after that inflection point, stocks which were the biggest losers during the previous year performed exceptionally well and caused strong under-performance of classical long-short momentum strategy. How can we prevent this situation from happening again? That’s the topic of our favorite new recent study written by Matthias Hanauer and Steffen Windmueller. They analyze three momentum risk management techniques – idiosyncratic momentum, constant volatility-scaling, and dynamic scaling, to find the remedy for momentum crashes. It’s our recommended read for this week for equity long-short managers …

Authors: Matthias Hanauer and Steffen Windmueller

Title: Enhanced Momentum Strategies

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3437919

Abstract:

This paper compares the performance of three momentum risk management techniques proposed in the literature — idiosyncratic momentum, constant volatility-scaling and dynamic scaling. Using data for individual stocks from the U.S. and across 48 international countries, we find that all three approaches decrease momentum crashes, lead to higher risk-adjusted returns and raise break even transaction costs. In a multiple model comparison test that also controls for other factors, idiosyncratic momentum emerges as the best momentum strategy. Finally, we find that the alpha stemming from volatility-scaling is distinctive from the idiosyncratic momentum alpha.

Notable quotations from the academic research paper:

“Our main findings can be summarized as follows. First, using a long sample of U.S. stocks from 1930 to 2017 and a broad sample of stocks from 48 international markets from 1991 to 2017, we show that all risk management strategies substantially increase Sharpe ratios.

| Algo Trading Data Discounts are available exclusively for Quantpedia’s readers. |

Furthermore, both skewness and kurtosis as well as maximum drawdowns decrease compared to standard momentum so that their distributions become more normal. Comparing the individual risk management strategies within samples, we find similar improvements for the long U.S. sample for Sharpe ratios and t-statistics (both roughly double compared to standard momentum) for all three approaches, while maximum drawdowns are reduced most by idiosyncratic momentum.

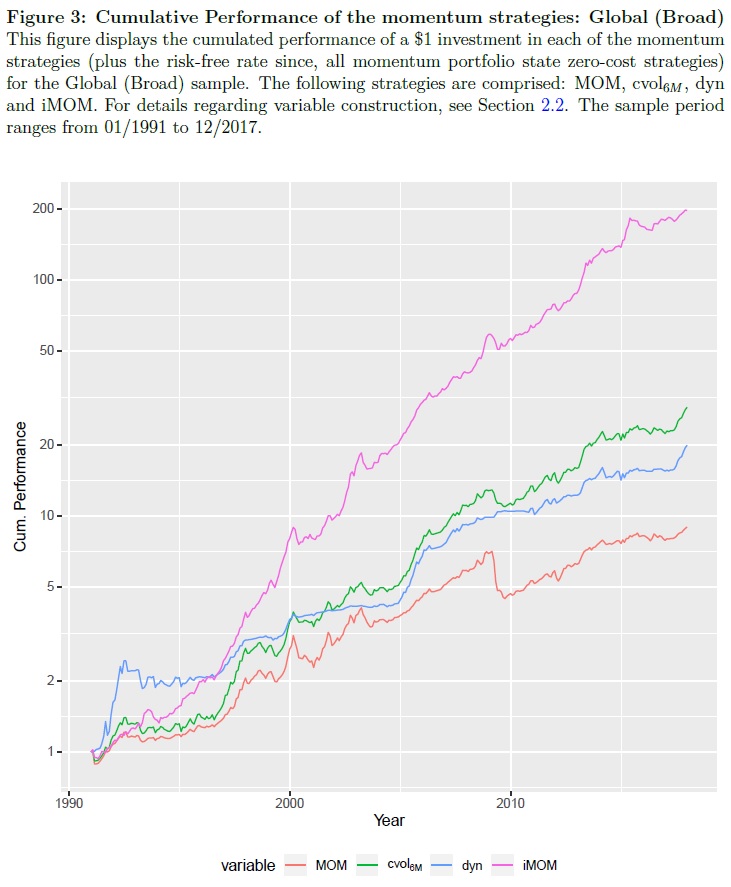

For the broad sample, we document that idiosyncratic momentum outperforms all other strategies, as the improvements in Sharpe ratio and t-statistic for idiosyncratic momentum are more than twice as the improvements of volatility-scaling strategies and the reduction in maximum drawdowns is highest. Additionally, idiosyncratic momentum shows the best performance in Januaries for which standard momentum shows negative returns.

For the broad sample, we document that idiosyncratic momentum outperforms all other strategies, as the improvements in Sharpe ratio and t-statistic for idiosyncratic momentum are more than twice as the improvements of volatility-scaling strategies and the reduction in maximum drawdowns is highest. Additionally, idiosyncratic momentum shows the best performance in Januaries for which standard momentum shows negative returns.

Third, our findings indicate that risk-managed momentum strategies should be at least as implementable as standard momentum. By calculating the transaction (break-even) costs that theoretically would render the strategies insignificant, we are able to directly compare the risk-managed momentum strategies with each other after taking portfolio turnover into account. Although all risk management strategies have higher average portfolio turnover compared to standard momentum, we document higher break-even costs due to higher (risk-adjusted) strategy returns.

Finally, we find that the alpha generated by scaled momentum strategies is distinct from the idiosyncratic momentum alpha, as indicated by the economically and statistically significant alphas in pairwise mean-variance spanning tests. Furthermore, we show that scaling idiosyncratic momentum by its realized volatility further increases its Sharpe ratio. We find that even though residualizing of returns reduces the systematic exposure of the constructed idiosyncratic momentum factor, scaling the factor by its volatility generates even higher risk-adjusted returns, undermining the conceptual difference of the risk management approaches.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend