Understanding Gold – Hedge, Diversifier, or Overpriced Insurance?

In Understanding Gold, Claude B. Erb and Campbell R. Harvey examine gold’s enduring reputation as a safe-haven asset and contrast popular narratives with empirical evidence. While gold has preserved purchasing power over millennia—what the authors call the “golden constant”—this does not translate into reliable short- or medium-term inflation hedging. Gold’s volatility is comparable to equities, while inflation itself is far more stable, making gold an unreliable hedge over typical investor horizons. The key insight is that gold’s real long-run return is approximately zero, which is precisely what one should expect from a hedging asset rather than a growth asset.

The paper shows that gold’s real value tends to mean-revert over time, and that periods following real-price extremes have historically been associated with low or negative multi-year returns. This creates what the authors term the “golden dilemma”: gold is most attractive precisely when its expected returns are lowest. Nevertheless, gold’s low correlation with equities has made it a valuable portfolio diversifier, and historical drawdown analysis demonstrates that gold often performs well—or at least less poorly—during equity market stress, albeit not perfectly or universally.

A major contribution of the paper is its analysis of why gold prices are exceptionally high today. The authors highlight the “financialization” of gold, especially following the launch of gold-backed ETFs in 2004, which removed institutional constraints and created structurally higher demand. ETF flows are strongly positively correlated with gold returns, suggesting momentum-driven and hedging-related demand rather than valuation discipline. In parallel, geopolitical forces—particularly the weaponization of the U.S. dollar via sanctions—have accelerated central bank gold accumulation as part of broader de-dollarization efforts, most notably by China and Russia.

Looking ahead, the authors argue that additional demand shocks may still lie ahead. One potential catalyst is regulatory: if gold were ever classified as a Tier 1 High Quality Liquid Asset under Basel III, commercial banks could hold it for liquidity purposes, unlocking demand on a scale comparable to—or larger than—the ETF revolution. However, investors should not confuse rising demand with high expected returns. Gold’s role remains that of insurance: valuable for diversification and crisis protection, but historically associated with low real returns after price peaks. The paper ultimately urges investors to view gold with realism rather than reverence.

Authors: Claude B. Erb and Campbell R. Harvey

Title: Understanding Gold

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5525138

Abstract:

Gold has a reputation as a safe-haven asset-useful in times of economic turmoil or inflation. However, perceptions can differ from reality. We examine the investment characteristics of gold and assess its reliability as a hedging asset. We also explore the reasons that the gold price is so high today by detailing the role of the financialization of gold as well as the push among many countries to de-dollarize. We also argue that a second demand shock that could be on the same scale as ETF introduction looms on the horizon with potential changes in Basel III regulations that would allow commercial banks to hold gold for regulatory purposes as a high-quality liquid asset. It is inconsistent that central banks hold gold as a major reserve asset-yet commercial banks cannot. Finally, using the framework of Erb and Harvey (2013), we show that based on historical analysis, when gold hits all-time highs, the subsequent multi-year returns are low or negative. This needs to be weighed against both gold hedging ability, i.e., hedging assets have low expected returns, and the possibility of increased demand from de-dollarizing countries, institutional investors and commercial banks.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Gold has held its value over the last 2,500 years. Its purchasing power has not changed much. Erb and Harvey (2013) shared a historical example from Roman military payrolls. The annual salary of a Roman centurion in the reign of Augustus was 38.58 ounces of gold.3 Based on gold’s average price over the past year, that is about what a U.S. Army captain, major, or lieutenant colonel earns today.4

Gold’s consistent purchasing power over the millennia led Roy Jastram (1977) to propose the “golden constant.” For almost all assets, return has two components: compensation for inflation and real return. If gold has held its value, its price has moved with inflation. That implies that gold’s real return has been zero and that gold has been a successful inflation hedge for the past 2,000-plus years.

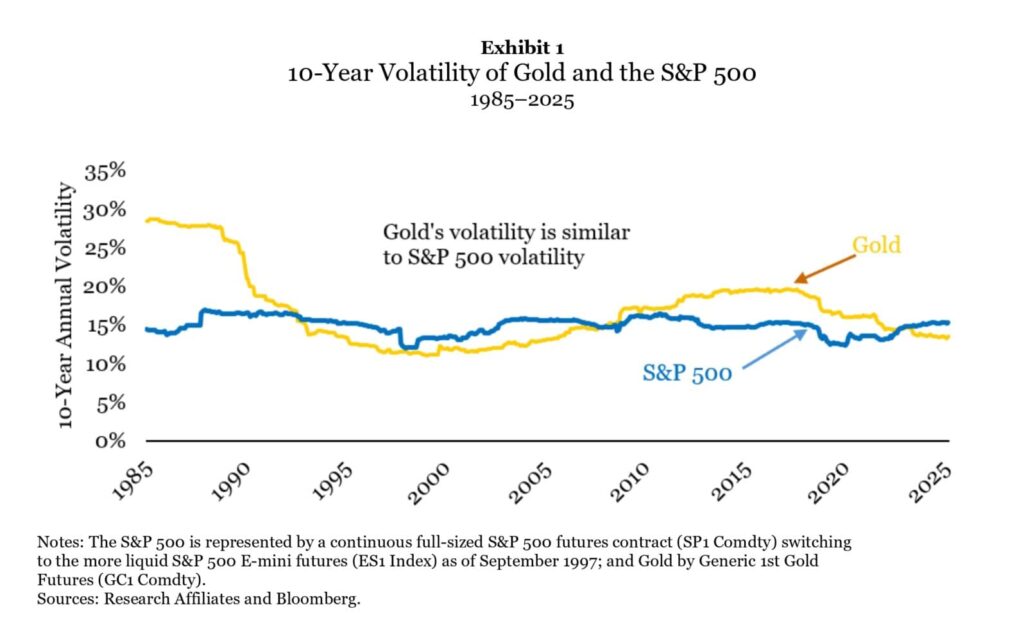

Of course, no real-world investor has a 2,000-year horizon. Over shorter periods, gold can be an unreliable hedge for one simple reason: It is a volatile asset. Exhibit 1 shows gold has about the same volatility as the S&P 500.

But what about less severe crises, for example, equity market drawdowns? How does gold compare to long put options, long bonds, and other hedging strategies? We looked at gold’s performance in 11 major stock market drawdowns relative to Treasury bonds and S&P 500 puts taken 5% out of the money. As Exhibit 5 shows, the price of gold rose in eight of the 11 drawdowns and fell by less than the S&P 500 in the three others. Gold did provide some diversification benefit and could be a valuable hedge against current stock market volatility.

Exhibit 20 shows that the U.S. holds 22.4% of world reserves, almost 2.5 times as much as second-place Germany. All euro-area countries and the European Central Bank (ECB), combined hold 29.7%. While reserve levels are interesting, changes in reserves are what potentially moves prices.

Exhibit 21 shows the largest changes in gold holdings. Panel A covers 2002 to 2025 and Panel B looks at the last 10 years. There is a large overlap in purchasers, with China and Russia the key buyers. Over the last 10 years, they have added approximately 2,500 tons between them. India and Poland are also active buyers, but nowhere near China and Russia.

The demand shock perspective hinges on whether “this time is different.” Has a structural change rendered the old model obsolete? It is always tempting to believe so when times feel different. But, as we have said before, every time is different. The question is whether the circumstances are different enough. Can we make the case, through economic reasoning, that the model has changed? In Exhibit 35, the shift is reflected in a change of intercept. The slope of the two lines is nearly identical.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend