What Drives the Excess Bond Premium?

The Excess Bond Premium (EBP – the portion of corporate bond spreads not explained by default risk), a key metric in quantitative finance for gauging credit spreads, has long been a subject of intense scrutiny. Recent research sheds new light on its dynamics, moving beyond traditional macroeconomic factors to explore the role of information flow. By analyzing news attention across 180 topics, a significant portion of the EBP’s variation can be explained, offering a novel lens to understand its fluctuations and predictive power.

This analysis reveals that news attention to specific areas like financial intermediaries and crises tends to elevate the EBP, signaling potential macroeconomic downturns. Conversely, increased news coverage of politics and science often leads to decreased EBP. This attention-driven approach not only rivals the predictive capabilities of sentiment measures but also demonstrates a robust ability to forecast business cycles dating back to the early 20th century. The implications of this research highlight the importance of incorporating textual analysis and news dynamics into our understanding of credit markets and macroeconomic forecasting.

Main findings:

News about financial intermediaries and crises

- Drives up EBP.

- Predicts downturns in employment and output, consistent with the idea that EBP reflects financial sector stress.

Politics, especially U.S. presidents, matter more than expected

- Attention to presidents Bush, Obama, Trump, and Biden (labeled “BOTB”) significantly increases EBP.

- This “president topic” is the strongest predictor of economic growth, often more powerful than news about recessions or crises.

- Other political topics (e.g., committees, policy changes) tend to reduce EBP.

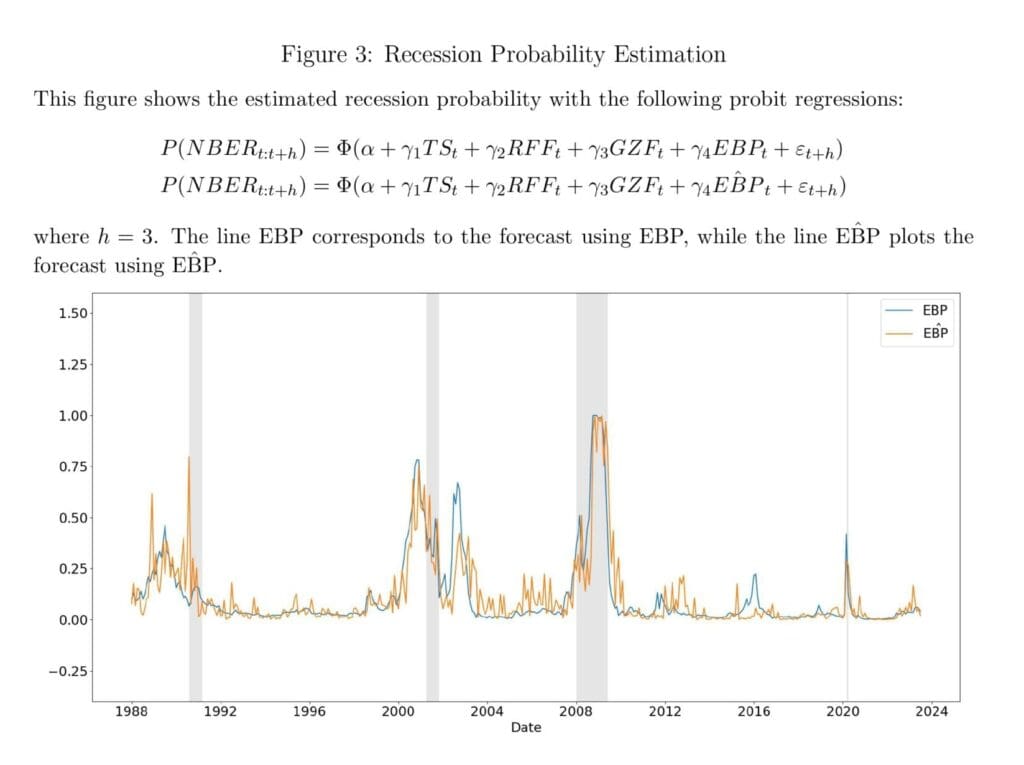

EBP forecasts macro outcomes back to the early 1900s

- Historical estimates show elevated EBP precedes recessions and banking panics.

- Confirms predictive power beyond the post-1973 dataset of Gilchrist & Zakraǰsek (2012).

News attention > sentiment

- While sentiment indices from word dictionaries forecast macro activity, their power disappears once ˆEBP is included.

- Predictive variation flows through attention to specific topics, not raw sentiment.

Robustness

- Results hold across investment-grade vs. high-yield bonds.

- Stable across different topic classifications and forecasting horizons (3 vs. 12 months).

This novel approach also has valuable implications for practice: Policy-makers and practitioners can use attention to news topics to filter EBP for non-predictive sources of variation and extract the most predictive sources for macroeconomic fluctuations. Conclusions suggest they should focus on attention-based news rather than direct measures of charged sentiment, which many data vendors calculate.

Authors: Kevin Benson, et al.

Title: Understanding the Excess Bond Premium

Link: https://dx.doi.org/10.2139/ssrn.5037810

Abstract:

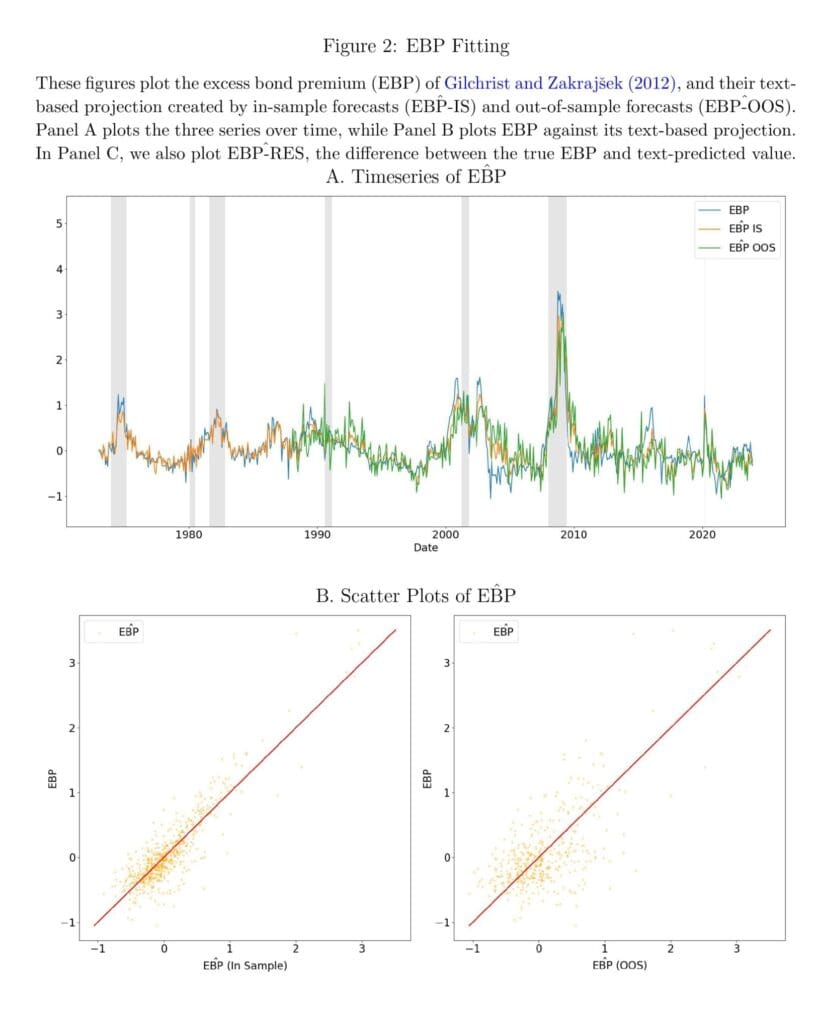

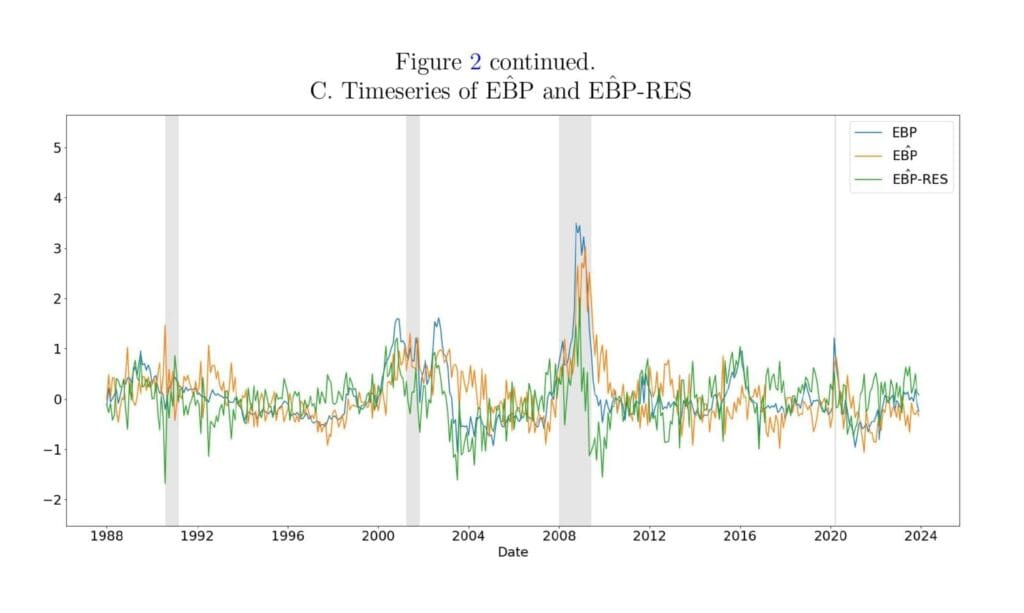

We study the drivers of the Gilchrist and Zakrajšek (2012) excess bond premium (EBP) through the lens of the news. The monthly attention the news pays to 180 topics (Bybee et al., 2024) captures up to 80% of the variation in the EBP, and this component of variation forecasts macroeconomic movements. Greater news attention to financial intermediaries and crises tends to drive up the EBP and portend macroeconomic downturns, while greater news attention to politics and science tends to drive down the EBP. Attention-based estimates of EBP largely drive out the forecast power of direct sentiment measures for macroeconomic fluctuations and predict the business cycle going back to the early 1900’s. Overall, we attribute predictive variation about the EBP for macroeconomic movements to variation in news attention to financial intermediaries, crises, and politics.

As always, we present several interesting figures and tables:

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend