What Works (and Doesn’t Work) in Cryptocurrencies

Authors: Yang

Title: Behavioral Anomalies in Cryptocurrency Markets

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3174421

Abstract:

If behavioral biases explain asset pricing anomalies, they should also materialize in cryptocurrency markets. I test more than 20 stock return anomalies based on daily cryptocurrency data, and document strong evidence of price momentum. Unlike stock markets, price reversal and risk-based anomalies are weak, controlling for market and size. Cryptocurrency anomalies can be explained by behavioral theories that place more emphasis on the role of speculators than fundamental traders.

Notable quotations from the academic research paper:

"The speculative and hard-to-value nature makes the cryptocurrency market a novel environment that facilitates the study of behavioral impacts on asset prices. Because speculators account for the vast majority of cryptocurrency market participants, the behavioral impact can be stronger than traditional markets. Aside from this, cryptocurrency markets enjoy some good properties: the overall level of investor sophistication in cryptocurrency markets are much lower; there are only a few institutional investors until recently. Thus, mispricing can be severe. Above stylized facts of cryptocurrency markets fit well into many behavioral theories that particularly emphasize investor irrationality. Thus, if asset pricing anomalies can be explained by behavioral theories, they shall also be reflected in cryptocurrency markets.

Having this in mind, I test more than 20 stock price anomalies based on cryptocurrency data.

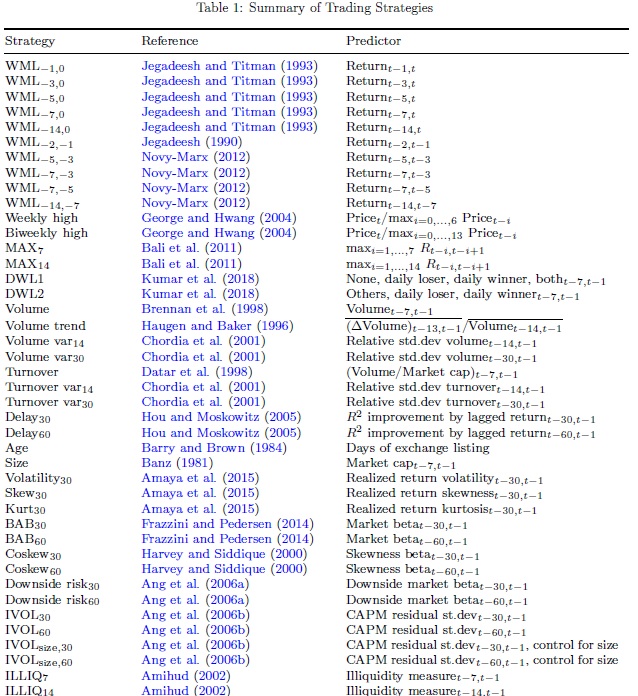

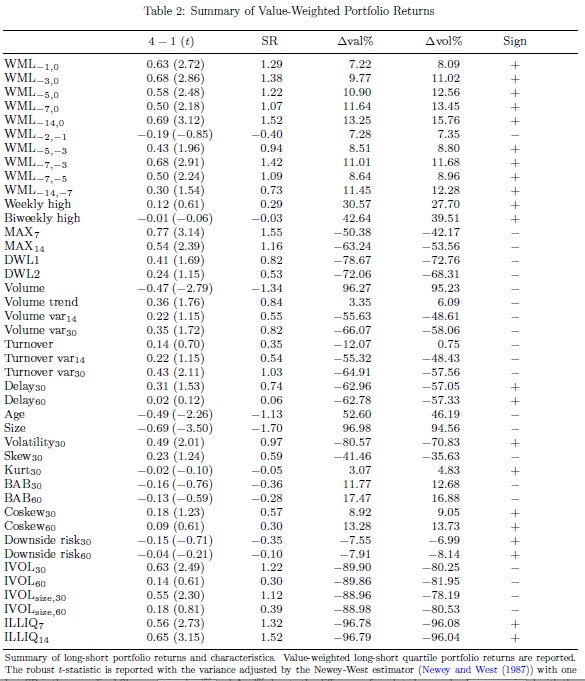

Interestingly, anomalies that are commonly recognized as behavior-driven, in particular, price momentum, are also observed in cryptocurrency markets. Price momentum describes the phenomenon that past winner (loser) assets may continue to outperform (underperform) in the future. The momentum effect turns out statistically significant and robust in various aspects. In contrast, risk-based anomalies, for example, return moment risks, are insignificant. The results are not surprising, as if the incentive for holding cryptocurrencies is largely speculative, it is not expected that exposure to certain form of risk earns a premium.

Unlike stock markets, short-term price reversal in cryptocurrency markets is very weak at a daily frequency. No evidence of long-term price reversal is revealed. This empirical finding makes cryptocurrency anomalies distinct from stock market anomalies.

The most plausible explanation of cryptocurrency momentum is given by De Long, Shleifer, Summers, and Waldmann (1990). Their model implies that overconfident noise traders push up the price and create risk that makes fundamental traders reluctant to combat mispricing. If noise traders dominate, overpricing can be even more severe, as is the case of cryptocurrency markets, where speculators play the role of overconfident noise traders. Further, their model does not predict a long-term reversal as long as noise traders remain overconfident. This situation is analogous to cryptocurreny markets and consistent with the empirical findings of this paper. Moreover, their model implies an excessive volatility, another empirical stylized fact of cryptocurrency markets."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend