Why Most Portfolios Are Under Diversified

Diversification is a key principle in portfolio construction, yet equal-weight portfolios often fail to deliver true risk diversification. This study shows that capital-based allocation can mask strong concentration in a small number of underlying risk factors. We analyze a simple multi-asset portfolio of ten ETFs spanning equities, bonds, commodities, credit, private equity, and Bitcoin. Despite equal weights, risk is highly concentrated in a few volatile assets and amplified by strong cross-asset correlations, particularly within equity and credit markets. Risk parity reduces concentration by balancing risk contributions and improves risk-adjusted performance, though at the cost of lower returns. Further improvement is achieved through clustering-based allocation, which groups similar assets and allocates risk across more independent sources of return. The results demonstrate that effective diversification depends on the structure of risk factors rather than the number of assets or equal capital weights.

Introduction

Diversification is one of the most fundamental principles of portfolio construction. However, in practice, it is often more apparent than real. Portfolios that appear diversified based on capital allocation may still be heavily concentrated in a small number of underlying risk factors.

To illustrate this point, we construct a simple multi-asset portfolio consisting of ten widely used ETFs covering equities, bonds, commodities, credit, private equity, and Bitcoin obtained from EODHD.com – the sponsor of our blog (and as a special offer, our blog readers can enjoy an exclusive 30% discount on premium EODHD plans).

Each asset is assigned an equal weight of 10%, creating a seemingly well-diversified allocation.

All analyses are provided by Quantpedia Portfolio Analysis. Firstly, let’s analyze our portfolio via the Portfolio Risk Parity report.

The left chart shows the equal-weight allocation, while the right chart presents the decomposition of risk contributions. Despite identical capital weights, the portfolio is far from balanced. A substantial portion of total risk is driven by a few dominant assets, most notably Bitcoin, Nasdaq equities, and private equity. Lower-volatility instruments, such as government bonds, contribute only marginally to overall risk.

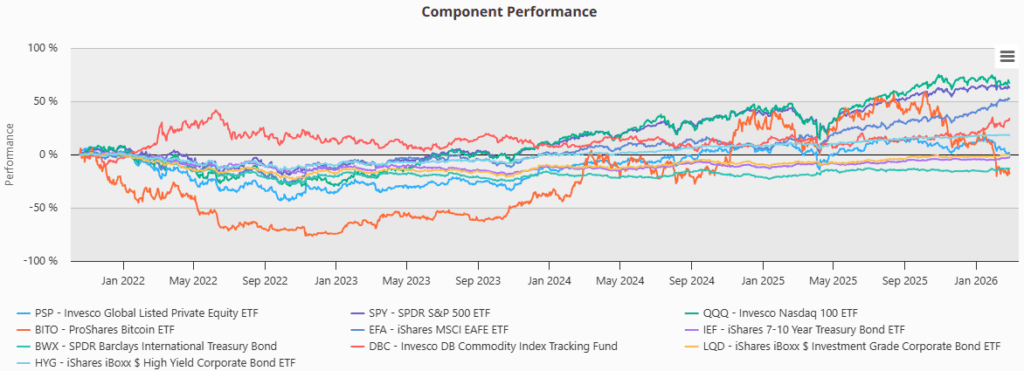

The component performance further highlights the asymmetry. High-volatility assets dominate portfolio fluctuations and largely determine the overall trajectory of returns, while other assets play only a secondary role.

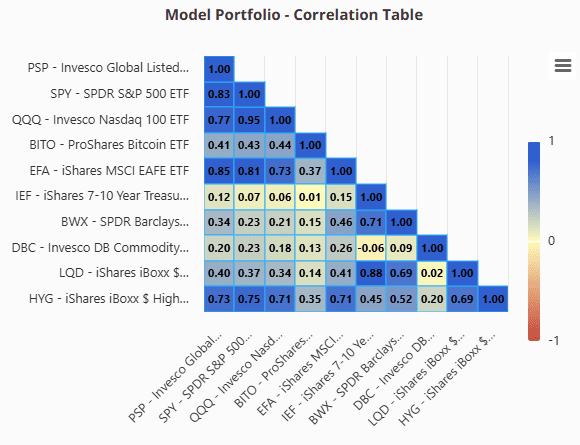

This imbalance is further amplified by the correlation structure of the portfolio.

The correlation matrix shows that many assets are strongly related. Equity exposures (SPY, QQQ, EFA) exhibit high mutual correlation, while credit instruments behave similarly to equities. Private equity is also closely tied to public markets. Even Bitcoin, often perceived as a diversifier, shows a positive correlation with risk assets in the range of 0.3 to 0.4. As a result, the portfolio contains multiple positions that effectively represent the same underlying risk.

The resulting equally weighted portfolio delivers solid performance, but its behavior is largely driven by concentrated exposures. Drawdowns coincide with periods of stress in equity markets and other risk assets, confirming that diversification benefits are limited.

Risk-Based Allocation

A natural way to address this issue is to move from capital-based allocation to risk-based allocation. Instead of assigning equal weights, the portfolio is constructed so that each asset contributes a similar share of total risk.

The risk parity weights adjust dynamically, reducing exposure to high-volatility assets such as Bitcoin and equities, while increasing allocations to lower-volatility components such as bonds. This results in a more balanced distribution of risk contributions across assets.

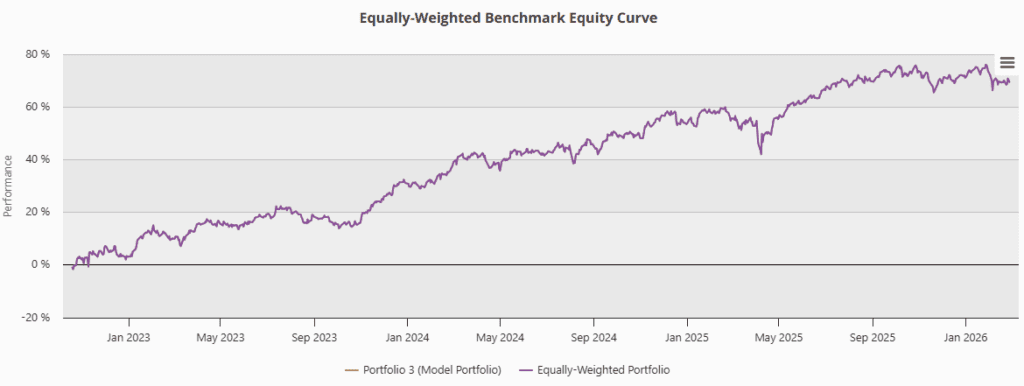

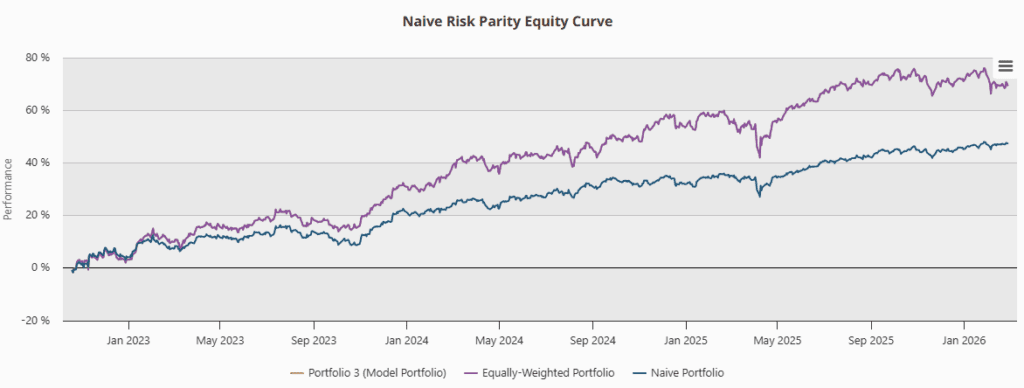

The impact of this adjustment is visible in the equity curve. Compared to the equally weighted portfolio, the risk parity strategy exhibits a smoother trajectory with significantly reduced drawdowns. The tradeoff is a lower absolute return.

The performance metrics confirm this observation. While returns decrease, volatility declines even more, leading to an improvement in risk-adjusted performance. Drawdowns are also meaningfully reduced, which is consistent with the objective of risk-based allocation.

Beyond Risk Parity: Clustering

Although risk parity improves the distribution of risk, it does not fully resolve the issue of correlated assets. If multiple instruments share similar behavior, allocating risk at the asset level may still lead to hidden concentration.

To address this, we apply clustering techniques to identify groups of assets with similar return characteristics.

The clustering results show that assets naturally form a small number of groups. Bitcoin appears as a distinct cluster, while equities and credit instruments are grouped together, and bonds form another cluster. This confirms that the true number of independent risk sources is significantly lower than the number of assets.

The cluster composition remains relatively stable over time, suggesting that these relationships are persistent rather than temporary.

This observation motivates an alternative approach: instead of allocating risk across individual assets, risk can be allocated across clusters.

Clustering-Based Risk Allocation

Clustering-based risk parity strategies aim to equalize risk contributions at the cluster level. This leads to a more effective diversification across independent sources of return.

The results show that clustering-based approaches can improve performance relative to naive risk parity. Returns are higher, while risk remains controlled, leading to stronger risk-adjusted metrics and improved drawdown characteristics.

Conclusion

The analysis demonstrates that equal-weight portfolios often create an illusion of diversification, since portfolio risk is typically driven by a limited set of common factors and reinforced by strong correlations among assets. Risk parity improves this by shifting focus from capital weights to risk contributions, reducing concentration in high-volatility assets and producing a more balanced risk profile. However, clustering-based methods provide an additional improvement by explicitly accounting for correlation structure and grouping similar assets, which leads to a more accurate representation of independent risk sources and more robust diversification.

Author: David Mesicek, Junior Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend