Are Equity Markets Manipulated?

We present two interesting research papers written by Bruce Knuteson. He contemplates why the cyclically adjusted price to earnings ratio of the S&P 500 index has been oddly high for the past two decades. He states that persistently strong equity market in US (and therefore also its high valuation in a comparison to history) and also in other developed countries can be an outcome of intraday trading pattern of several huge quant equity long-short funds which aggressively buy in the morning and sell in the afternoon to expand their trading book (or alternatively to simply manipulate market – push prices of stocks in their portfolio up).

Authors: Bruce Knuteson

Title: Information, Impact, Ignorance, Illegality, Investing, and Inequality

Link: https://arxiv.org/pdf/1612.06855.pdf

Abstract:

We note a simple mechanism that may at least partially resolve several outstanding economic puzzles, including why the cyclically adjusted price to ear nings ratio of the S&P 500 index has been oddly high for the past two decades, why gains to capital have outpaced gains to wages, and the persistence of the equity premium.

Notable quotations from the academic research paper:

"In United States equity markets, bid-ask spreads early in the trading day are typically larger than spreads later in the trading day. The price impact of aggressive trades early in the trading day is therefore typically larger than the price impact of equally sized aggressive trades later in the day.

Market makers make wider markets early in the trading day. The market, viewed as an information aggregator, respects the information content of aggressive orders early in the day more than the information content of equally sized aggressive orders later in the day. A repeated sequence of intraday round trips – e.g., buying in the morning and selling in the afternoon, repeated over many days – can therefore be expected to result in net price impact in the direction of the morning trade.

If some market participant (M) performs the same round trip each day – e.g., aggressively buying in the morning and selling in the afternoon – M’s trading will, on average, nudge the market’s midprice in the direction of his morning trading. If M has a large, slowly varying portfolio, the mark to market gains resulting from M’s daily intraday round trip trades can exceed the cost M incurs by crossing the spread twice each day.

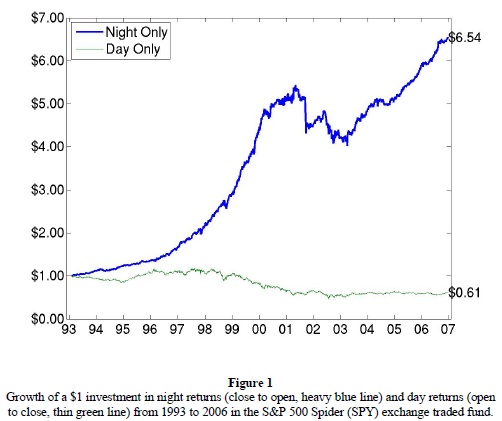

In light of the above, it is striking that the returns to the S&P 500 index over the fifteen years spanning 1993 to 2007, inclusive, all came at the start of the trading day. Indeed, Figure 1 of Ref. [M. J. Cooper, M. T. Cliff, and H. Gulen (2008), Return Differences Between Trading and Non-trading Hours: Like Night and Day, URL http://ssrn.com/abstract=1004081] is so striking it calls for a simple explanation. We propose such an explanation. We propose some market participant M, tending to trade in one direction early in the trading day and in the other direction later in the day, has had a much larger long-term effect on United States equity prices than has so far been widely appreciated.

"

"

And:

Authors: Bruce Knuteson

Title: How to Increase Global Wealth Inequality for Fun and Profit

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3282845

Abstract:

We point out a simple equities trading strategy that allows a sufficiently large, market-neutral, quantitative hedge fund to achieve outsized returns while simultaneously contributing significantly to increasing global wealth inequality. Overnight and intraday return distributions in major equity indices in the United States, Canada, France, Germany, and Japan suggest a few such firms have been implementing this strategy successfully for more than twenty-five years.

Notable quotations from the academic research paper:

"The Strategy is very simple: construct a large, suitably leveraged, market-neutral equity portfolio and then systematically expand it in the morning and contract it in the afternoon, day after day. The Strategy works because your trading will, on average, move prices in a direction that nets you mark-to-market gains. Bid-ask spreads are wider and depths are thinner near market open than near market close, so aggressive trades early in the trading day move prices more than equally sized aggressive trades later in the day. An intraday round trip (e.g., aggressively buying in the morning and selling in the afternoon) thus nudges the market's midprice in the direction of your morning trading. A reasonable level of daily round-trip trading combined with a su�ciently large portfolio will therefore produce expected mark-to-market gains exceeding the expected cost of your daily round-trip trading.

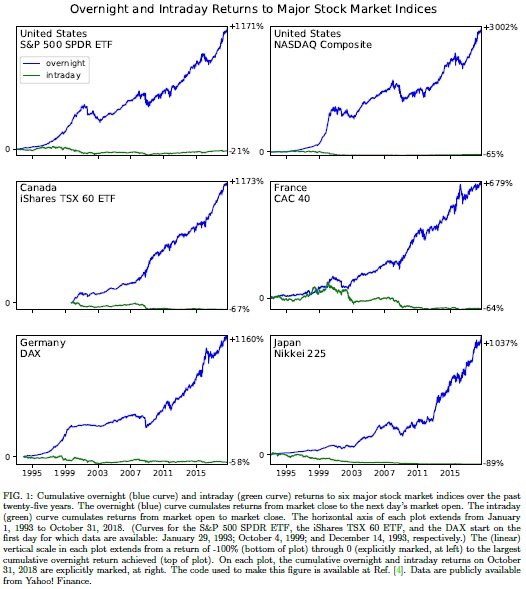

Figure 1, which shows cumulative overnight and intraday returns over the past 25 years in six major stock market indices: the S&P 500 index and the NASDAQ Composite index in the United States, Canada's TSX 60, France's CAC 40, Germany's DAX, and Japan's Nikkei 225 [20]. The return pattern in the S&P 500 index was �rst pointed out over a decade ago. Similar return patterns have been identi�ed in major indices of other developed countries. The only plausible explanation so far advanced for the highly suspicious return patterns in Figure 1 is someone using the Strategy.

"

Are you looking for more strategies to read about? Check http://quantpedia.com/Screener

Do you want to see an overview of our database of trading strategies? Check https://quantpedia.com/Chart

Do you want to know how we are searching new strategies? Check https://quantpedia.com/Home/How

Do you want to know more about us? Check http://quantpedia.com/Home/About

Follow us on:

Facebook: https://www.facebook.com/quantpedia/

Twitter: https://twitter.com/quantpedia

Share onLinkedInTwitterFacebookRefer to a friend