Systematic Interventions of Central Banks and Major Currency Risk Factors

Related to all major currency risk premiums:

#5 – FX Carry Trade

#8 – FX Momentum

#9 – FX Value – PPP Strategy

Authors: Fratzcher, Menkhoff, Sarno, Schmeling, Stoehr

Title: Systematic Intervention and Currency Risk Premia

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3119907

Abstract:

Using data for the trades of 19 central banks intervening in currency markets, we show that leaning against the wind by individual central banks leads to "systematic intervention" in the aggregate central banking sector. This systematic intervention is driven by and impacts on the same factors that drive currency excess returns: carry, momentum, value, and a dollar factor. The sensitivity of an individual central bank's intervention to these factors differs markedly across countries, with developed countries making a profit from intervention and emerging markets incurring large losses.

Notable quotations from the academic research paper:

"A large literature has documented that the cross-section of currency excess returns is predictable, and that currency risk premia can be captured through straightforward investment strategies. These includes, inter alia, carry trades that buy high interest rate currencies and sell low interest rate currencies, dollar strategies that short the US dollar (USD) and buy a diversi fied portfolio of foreign currencies, momentum strategies that buy currencies that appreciated in the recent past and short those that depreciated in the recent past, and value strategies that buy undervalued currencies and sell overvalued currencies.

However, the FX market is populated by a large and diverse set of players, some of which are not necessarily motivated by getting exposure to these risk factors or by profi ting through FX trading, most notably central banks.

From a nance perspective, a number of interesting questions arise in this market setting in relation to whether and how central bank intervention across countries is related to the factors that drive the cross-section of currency excess returns: Are aggregate central bank interventions driven by the same set of factors that drive exchange rates? Do the trading actions of central banks, i.e., their FX intervention flows, aff ect currency risk premia and, if so, do they increase or decrease excess returns from popular currency strategies? Do central banks profi t or lose money from their intervention operations? These are the questions that we address in this paper.

We tackle these questions empirically using the data on daily sterilized interventions in the FX market. Speci cally, we use a subset of their data since we study interventions against the US dollar (USD) only, and we limit the sample of currencies to countries with (relatively) flexible exchange rate regimes and few or no capital controls. We study a cross-section of interventions in 19 exchange rates (all against the USD) by aggregating the interventions of the 19 associated central banks over the sample from 1995 to 2011.

We find that:

(i) there is a strong factor structure in interventions, which we call "systematic intervention", that is closely related to the factor structure in exchange rates;

(ii) central banks tend to intervene in support of a factor (carry, momentum, value, and/or dollar) when returns to that factor are low and vice versa;

(iii) as a corollary, central bank interventions are signi ficantly di fferent across di fferent market states;

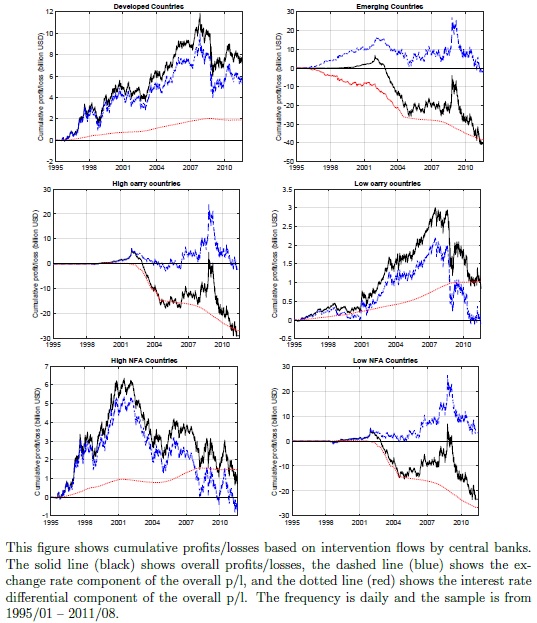

(iv) there are signi ficant di fferences across country subgroups (developed versus emerging markets, high versus low interest rate countries, high versus low net foreign asset positions);

(v) emerging countries lose money on their intervention activity and the bulk of these losses is driven by the hefty interest rate di fferential they face when they sell their currencies to buy the USD;

(vi) a simple price impact analysis suggests that global, systematic interventions by the aggregate central banking sector are large enough to move exchange rates by a signi ficant amount and, for example, interventions to support carry in the aftermath of the global fi nancial crisis lifted carry returns by about 5 percent.

Conditional analysis reveals that in normal times, which are typically characterized by normal or relatively low volatility and positive carry trade returns, central banks trade against carry, whereas in bad times when carry returns typically fall sharply, there is systematic intervention in support of carry (high interest currencies). These e ffects are particularly strong for emerging markets, countries with high interest rates, and countries with low net foreign asset positions. In essence, the "leaning against the wind" nature of intervention activities curbs carry profi ts for the investment community during good times, but helps reducing the carry losses in bad times, e ffectively smoothing carry returns. A similar mechanism applies to the other factors. Speci fically, systematic intervention is almost always against momentum and the dollar factor (i.e., the central banking sector is a net buyer of the US dollar), but this e ffect is much stronger in terms of intervention amounts at times of market turmoil. Hence, from the viewpoint of these factors, central banks don't just lean against momentum but also against the carry and dollar factor. Finally, systematic intervention is almost always in the direction of value (i.e., the central banking sector tends to act to curb exchange rate misalignments), but this e ffect is much more pronounced at times of market turmoil."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend