A Study on How Algorithmic Traders Earn Money

Authors: Ricky Cooper, Wendy Currie, Jonathan Seddon, and Ben Van Vliet

Title: Competitive Advantage in Algorithmic Trading: A Behavioral Innovation Economics Approach

Link:https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4008511

Abstract:

Purpose: This paper investigates the strategic behavior of algorithmic trading firms from an innovation economics perspective. We seek to uncover the sources of competitive advantage these firms develop to make markets inefficient for them and enable their survival.

Methodology: First, we review expected capability, a quantitative behavioral model of the sustainable, or reliable, profits that lead to survival. Second, we present qualitative data gathered from semi-structured interviews with industry professionals as well as from the academic and industry literatures. We categorize this data into first-order concepts and themes of opportunity-, advantage-, and meta- seeking behaviors. Associating the observed sources of competitive advantages with the components of the expected capability model allows us to describe the economic rationale these firms have for developing those sources and explain how they survive.

Findings: The data reveals ten sources of competitive advantages, which we label according to known ones in the strategic management literature. We find that, due to the dynamically complex environments and their bounded resources, these firms seek heuristic compromise among these ten, which leads to satisficing. Their application of innovation methodology that prescribes iterative ex post hypothesis testing appears to quell internal conflict among groups and promote organizational survival. We believe our results shed light on the behavior and motivations of algorithmic market actors, but also of innovative firms more generally.

Originality: Based upon our review of the literature, this is the first paper to provide such a complete explanation of the strategic behavior of algorithmic trading firms.

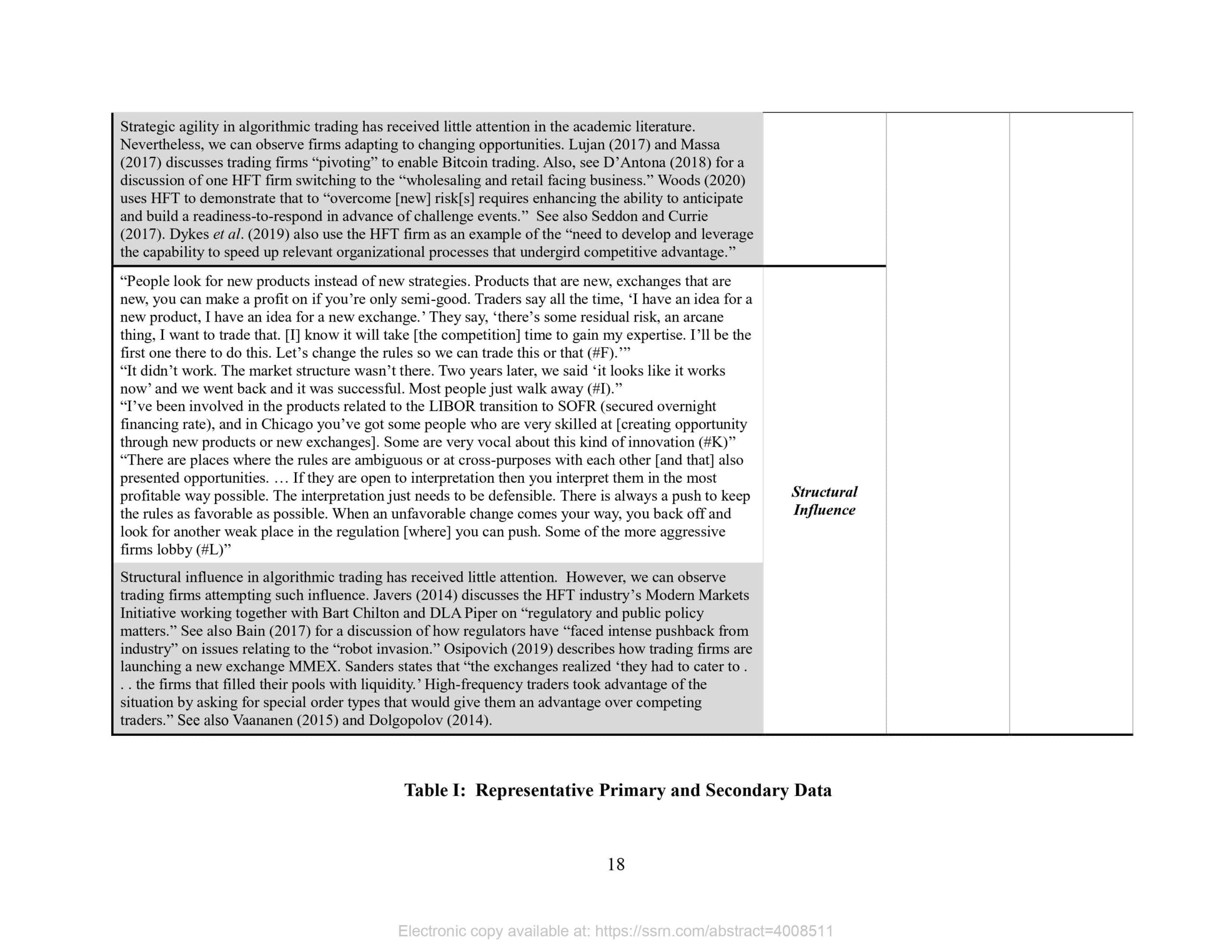

As always we present several interesting tables:

Notable quotations from the academic research paper:

“In our review, the academic and industry literatures have acknowledged the existence of competitive advantage in algorithmic trading, but have not studied the topic in a structured fashion. In this paper, we provide this structure by considering two research questions:

1. What is meant by sustainable, or consistent, or what we call reliable profits that lead to survival in an uncertain environment? This is a proxy for a market being inefficient for them.

2. What are the sources of competitive advantage these firms develop that allow them to generate those reliable profits and survive?

We answer the first question by fully developing expected capability theory (Kumiega et al., 2014; Van Vliet, 2017), a behavioral innovation model of decision-making. We answer the second question by gathering data on the sources of competitive advantage through semi-structured interviews with industry professionals and a review of the academic and industry literatures. We categorize these data according to known sources of competitive advantage using the methodology of Gioia et al. (2013). Then, because competitive advantage positively affects performance (see Ferreira et al. 2020), we discuss the links between expected capability and the observed sources of competitive advantage, thus providing a theoretical rationale for their development.

The literature on strategic entrepreneurship focusses on survival through sustainable profits, which arise from “identifying opportunities … and then developing competitive advantages to exploit them (Ireland et al., 2003, p. 966).” As a general definition, competitive advantage is a position or state of a firm that allows it to generate better performance than its rivals (Porter, 1980). In the parlance of finance, we might say that a firm has competitive advantage when it has an “edge,” which emphasizes its probabilistic nature. Competitive advantage does not guarantee survival but rather shifts the distribution in the firm’s favor. Sources of competitive advantage, then, are those specific organizational abilities or strengths that put a firm in such a position or state.

There is a wide literature equating informational inefficiency with opportunity for profit in markets. See, for example, Kondor (2009), Biais et al. (2011), Hendershott, et al. (2011), and Hoffman (2014). Algorithmic traders that demand liquidity profit by trading quickly on public information, thereby removing informational inefficiencies, while high frequency traders (a subset of algorithmic traders) that supply liquidity profit from the bid-ask spread and both reduce their adverse selection risk and make prices more efficient by updating their limit orders quickly to reflect new information (Chaboud et al., 2014).

Semi-structured interviews and narrative analysis enable richer data to be collected (Sobolev, 2020) and improve the understanding of the organizational realities at these firms (see Saunders and Townsend, 2016). As open-ended questions provide a useful entry-point for building on key themes (see Denzin and Lincoln, 2005), we began each interview with a framing question—What abilities, or edges, does your firm have that help you exploit opportunities in financial markets?—and added new questions in response to feedback (see Edwards and Holland, 2013). This led to additional discussion about how the interviewees view competitive advantage and allowed us to focus on real-life experiences, minimizing bias and subjectivism (see Flyvbjerg, 2006). The secondary data set consists of evidence gathered from the scholarly and industry literatures regarding sources of competitive advantage. This evidence provides independent corroboration of the interviewees’ comments. Essentially, primary and secondary data were collected until they became repetitive, which suggests saturation (see Guest et al., 2006).

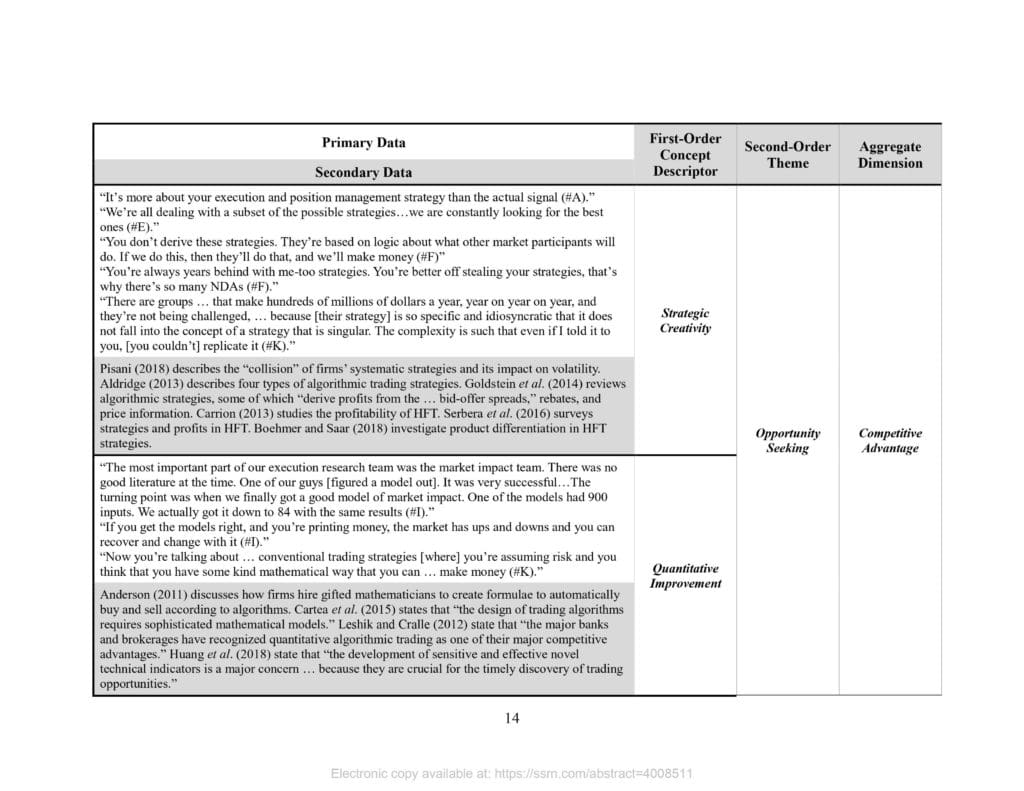

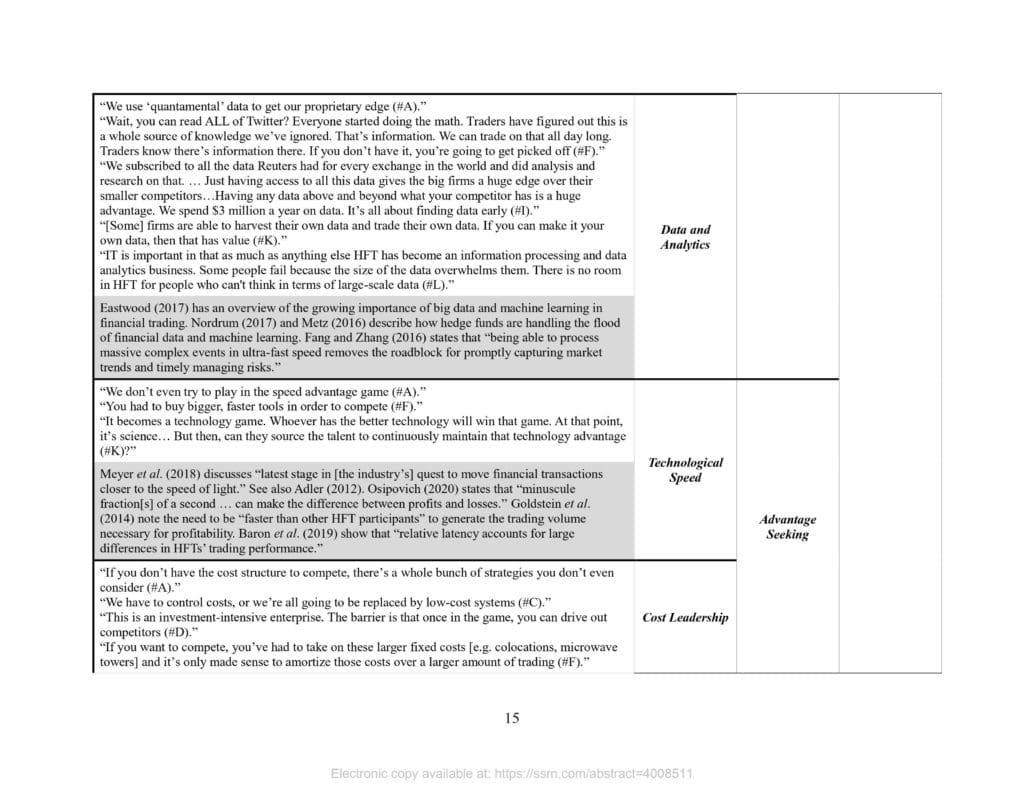

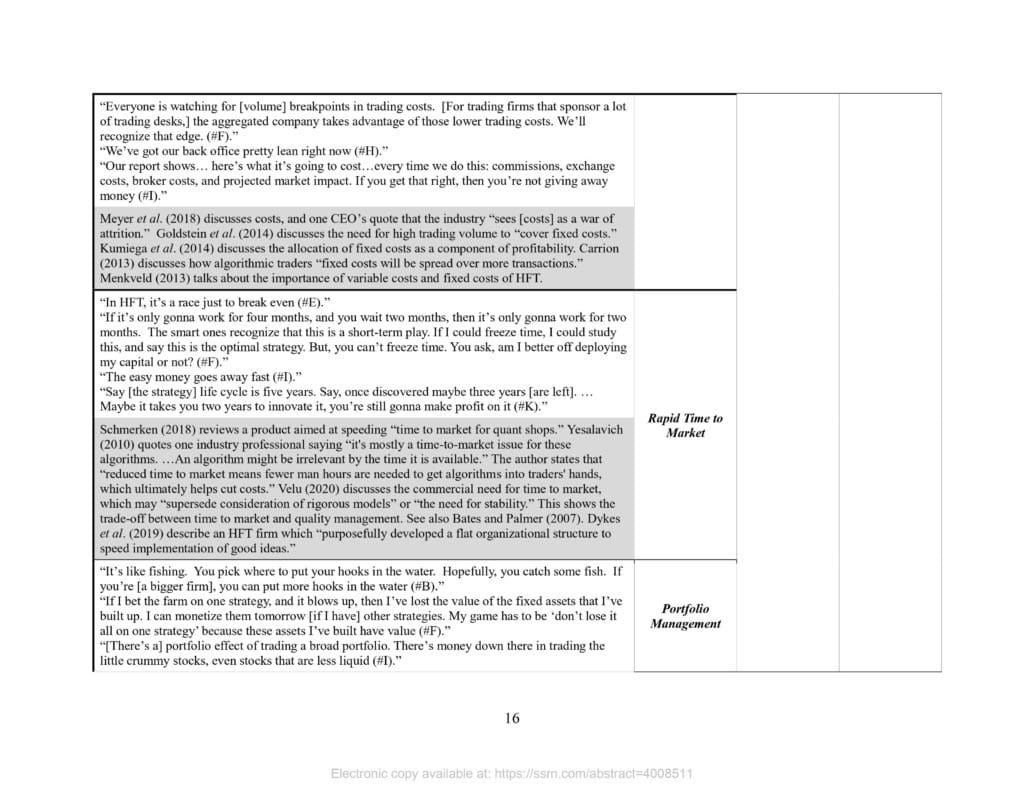

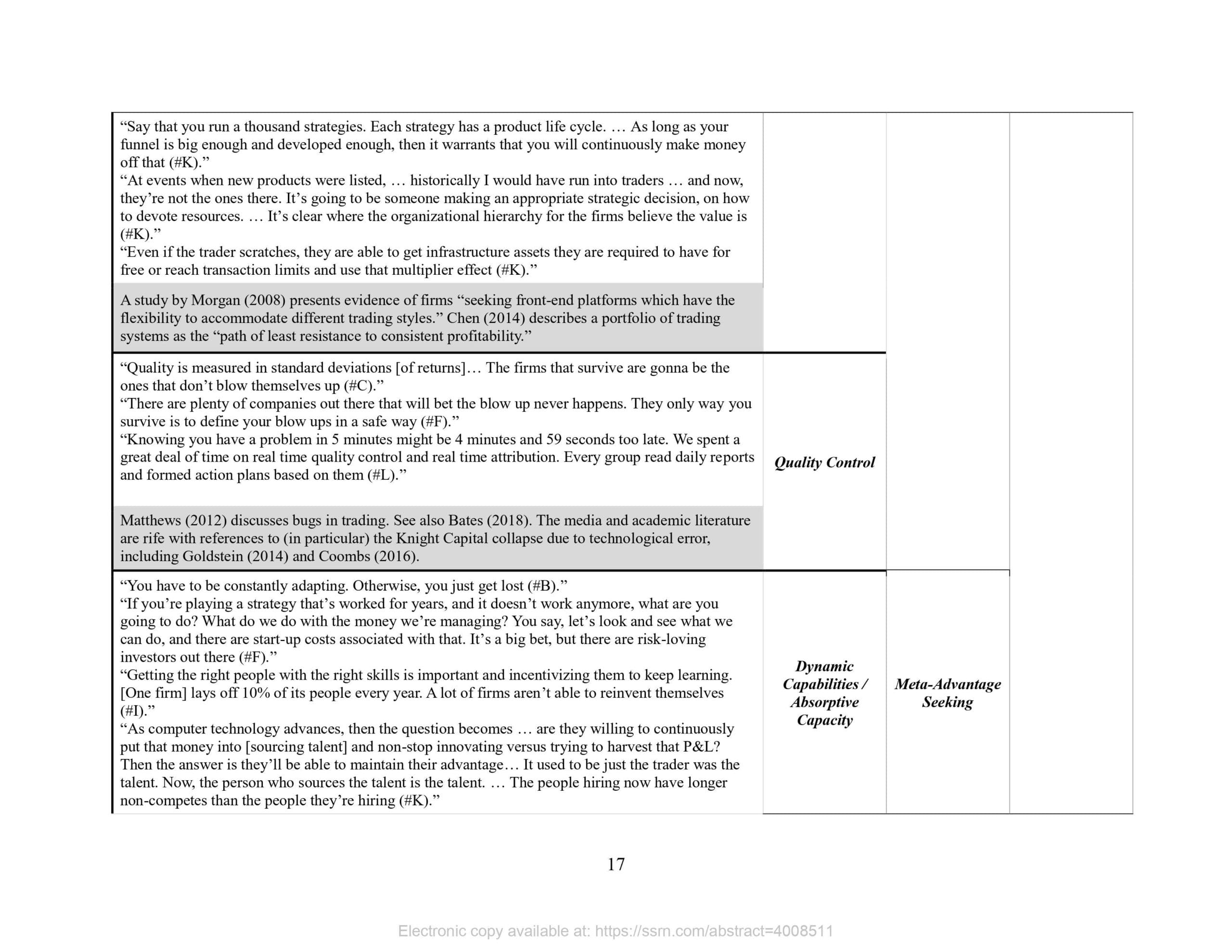

Focusing on the first-order descriptors in Table I, the first three are grouped into the second-order theme of opportunity-seeking behaviors. These are essentially domain specific forms of Chamberlain’s (1933) product differentiation. In Schumpeterian fashion, rare and difficult-to-imitate trading strategies, or ones requiring sophisticated implementations, create temporary monopolies and allow for reliable profits until competition arrives.

We observe heuristic trade-offs when these firms make allocation decisions in and among three portfolios:

1. Idiosyncratic resource position, the firm’s current portfolio of resources and competences. […]

2. Idiosyncratic competitive position, the firm’s portfolio of the observed sources of competitive advantage in Table I. […]

3. Idiosyncratic product position, the firm’s portfolio of trading systems.

Given that the firm’s three idiosyncratic positions are determined heuristically, performance satisficing is a more appropriate description of decision-making in algorithmic trading than is performance maximizing. Allocating requires information regarding the benefits of various decision choices, but gathering information and switching are costly. In the dynamic market environment, gathering information and adapting, or “pivoting,” through iterative ex post hypothesis testing of (6) appears to accelerate heuristic search and lower costs. Thus, the innovation methodologies discussed are the mechanism by which they achieve McGrath’s (2013) “transient advantage,” adapting their competitive position while maintaining satisficing performance. Unlike the individual investor who, under the efficient market hypothesis, relies on luck to succeed, the algorithmic trading firm, under the adaptive market hypothesis, depends on its ability to deploy its resource position to develop a competitive position that enables its product position to exploit market opportunities in ways that generate performance sufficient to survive.

Simply recognizing opportunity is not the same as profitably exploiting it. Many firms may discover an informational inefficiency, for example, but very few may have the competitive position to generate reliable profits from it. Essentially, the firm’s idiosyncratic competitive position makes available to the firm trading strategies that competitors find unprofitable. The challenge for the firm is to assess the opportunities available to it in the current environment and to adapt its competitive position to make more strategies available in the future. Of course, not all sources of competitive advantage will be equally important (Dreyer and Gronhaug, 2004).

Further, understanding the competitive, satisficing behavior of algorithmic market actors ought to promote appropriate regulation. Ensuring firms trade safely in the market ecosystem while satisfying their obligations to stakeholders as they innovate and adapt ought to play a central role in the regulatory structure. Regulations themselves ought to adapt to the evolving species and satisficing organisms that comprise the market ecology if they are to continuously promote market effectiveness—voluntariness, transparency, informational efficiency, and reliability (see Cooper et al., 2020). Regulation cognizant of the evolutionary process ought to focus on the structure of opportunities and the fairness of access to new, satisficing organisms.

This paper has drawn upon concepts from the literatures of innovation, strategic entrepreneurship, and behavioral finance to describe the strategic behaviors of algorithmic trading firms. This investigation was motivated by the consistent profits some of these market actors are known to generate. We fully developed expected capability as a model of reliable profits in uncertain environments and presented data regarding the sources of competitive advantage that algorithmic trading firms develop to generate reliable profits. By linking the observed sources to expected capability, we explain the economic rationale these firms have for developing them. The firm’s competitive position is what can make the markets inefficient for them, while others see no opportunity.

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend