Analysis of Commodity Futures Returns Over the Last Decade

Our favorite research paper about the performance of long-only investment strategies in commodities:

Authors: Erb, Harvey

Title: Conquering Misperceptions about Commodity Futures Investing

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2645444

Abstract:

Long-only commodity futures returns have been very disappointing over the last decade, leading some to wonder if it was a mistake to invest in commodities. The poor performance is the result of poor “income returns” and not of falling commodity prices. This observation may be surprising for many commodity investors who were not aware, who misperceived, they were making a bet on income returns, a return building block similar to a stock’s dividend yield or a bond’s yield. For investors seeking an inflation hedge, it may be surprising that the historical linkage of commodity returns with inflation seems to be the result of a connection between commodity income returns and inflation, not, as commonly misperceived, commodity price returns and inflation. It may be surprising that the value of commodity investments is smaller than the market capitalization of Facebook, a potentially striking misperception for investors seeking a portfolio diversifier with abundant capacity. There has been no change in the way that price returns and income returns drive the total returns of stocks, bond and commodities. What has changed is that maybe a good number of commodity investors now realize that they were operating outside of their “circle of competence” and did not have a sense of what future price and income returns could be and would be.

Notable quotations from the academic research paper:

"The last ten years have been challenging for many longâ€only commodity futures investors and given many a reason to question whether a ‘bad’ investment strategy drove a bad outcome or a ‘good’ strategy experienced an unlucky outcome. The total return of the S&P GSCI commodity index was â€4.6% per year, much lower than the +7.4% return for the S&P 500 stock index and the +4.5% return for the Barclays U.S. Aggregate bond index. The key driver of the poor S&P GSCI performance has been a â€8.0% income return. The commodity income return is the sum of a collateral return (in this case the threeâ€month Treasury bill) and a roll return (the cost, or benefit, of staying invested in futures contracts over time).

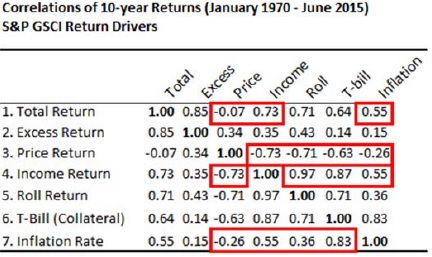

What has driven commodity portfolio returns? Focusing on the investable commodity index with the longest performance history, the S&P GSCI, Exhibit 3 shows correlations for rolling 10â€year returns for the drivers of the S&P GSCI. What seemingly drove commodity total returns? Interestingly, the first row shows that, historically, there has been little correlation between total return and price return (â€0.07), a high correlation between total return and income return (0.73) and a positive correlation between total return and inflation (0.55). What drove commodity price returns? The third row shows that historically price returns were negatively correlated with income returns (â€0.73), with roll returns (â€0.71), with collateral returns (â€0.63) and with inflation (â€0.26). What drove income returns? The fourth row shows that historically income returns were positively correlated with roll returns (0.97), with collateral returns (0.87) and with inflation (0.55). Finally, which commodity return components were correlated with inflation? The seventh row shows that price returns were negatively correlated with inflation (â€0.26), positively correlated with income returns (0.55), positively correlated with roll returns (0.36) and positively correlated with collateral returns (0.83). In a broad sense, Exhibit 3 suggests:

1) a weak link between commodity price returns and commodity total returns,

2) a negative link between inflation and commodity price returns,

3) a positive link between commodity income returns and commodity total returns,

4) a positive link between inflation and commodity income returns and

5) a negative relationship between income returns and price returns.

There are at least two opposing views to explain the decline in income and roll returns. The first view offered by Bhardwaj, Gorton and Rouwenhorst (2015) is that there is in fact no difference between preâ€2004 commodity performance and postâ€2004 commodity performance. Their view is illustrated by looking at the performance of a hypothetical, equallyâ€weighted paper portfolio created by Gorton and Rouwenhorst (2006). This paper portfolio embeds a common smart beta strategy, rebalancing an equally weighted portfolio. Working with an intuition that commodity futures markets are risk transfer insurance markets for commodity hedgers, Bhardwaj, Gorton and Rouwenhorst also find no evidence that an influx of longâ€only financial commodity investors over the last decade has impacted the historical or prospective returns of their hypothetical paper portfolio. Summing up the impact of the last decade, they find “the risk premium has been comparable to its longâ€term historical average”.

Norrish (2015) argues that Gorton and Rouwenhorst’s hypothetical paper portfolio “is not a viable option for most investors”, and reflects an alternative view that over the last decade an influx of longâ€only financial investors significantly lowered returns for actual and tradable longâ€only commodity indices. Echoing the view that commodity futures markets can be viewed as price insurance markets, Norrish’s view is that there has been too much longâ€only insurance capital chasing too few insurance opportunities. If too much insuranceâ€inspired capital has lowered returns then perhaps a contraction in insurance inspired capital might increase returns."

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend