Can AI Do Financial Research?

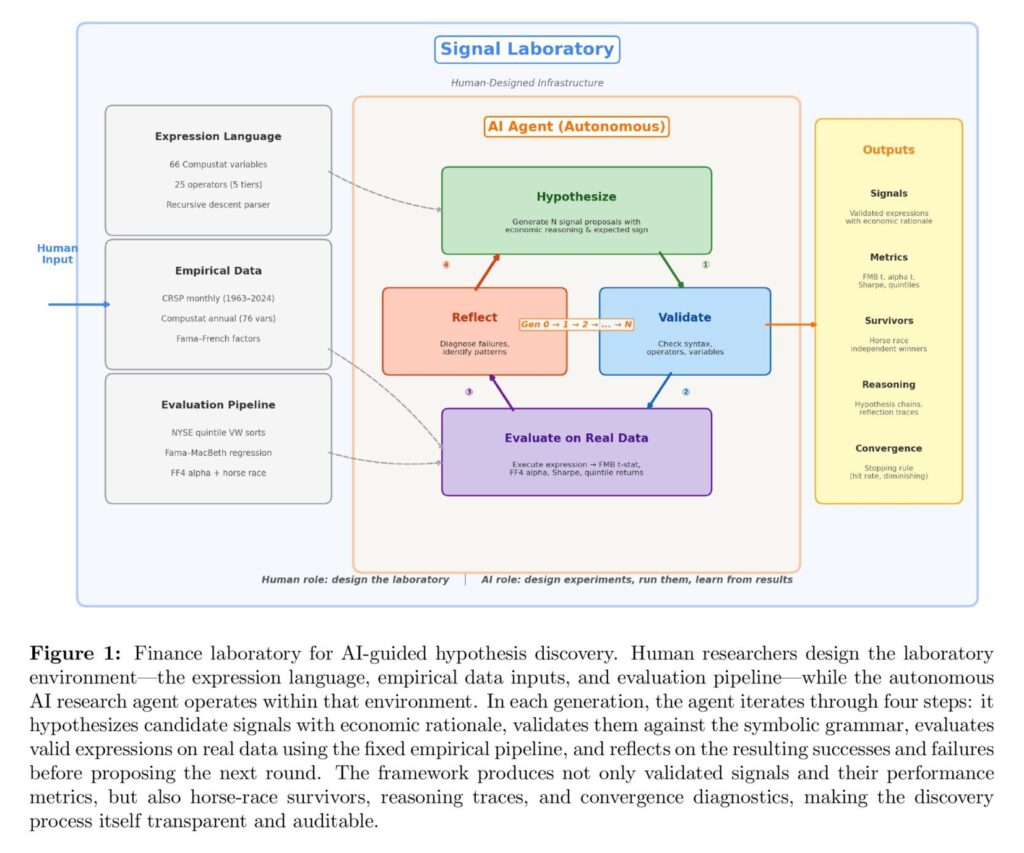

Large language models are already capable of summarizing financial research, but are they ready to conduct it? In their latest paper, researchers from Google, Boston College, and Columbia introduce a framework where a large language model doesn’t just fetch data—it acts as an autonomous AI research agent capable of navigating the “hypothesis discovery loop.” By placing an LLM within a human-designed laboratory—complete with a symbolic language of 66 accounting primitives and a standardized backtesting pipeline—the authors tested whether AI can move beyond black-box predictions to generate economically legible and statistically robust signals. This isn’t just about throwing a transformer at a price series; it is a systematic attempt to automate the “propose–test–reflect” cycle that defines empirical finance.

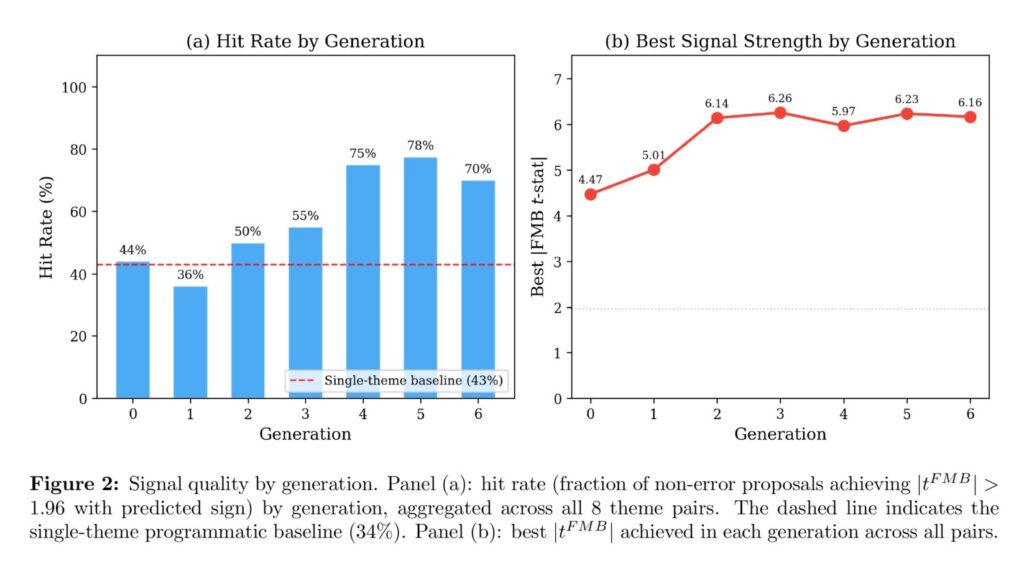

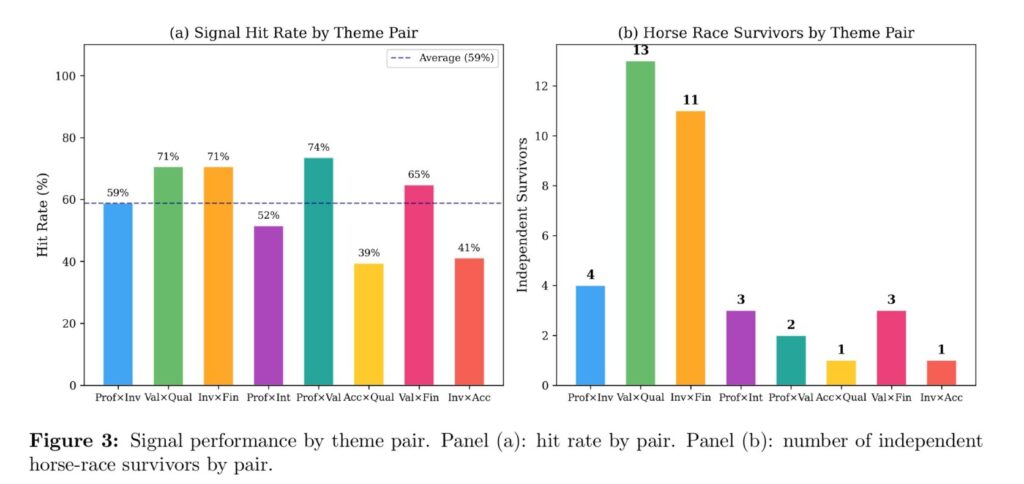

The AI research agent proved remarkably adept at combinatorial creativity, proposing 280 candidate signals across eight cross-theme interactions, such as Profitability × Valuation and Investment × Financing. Through seven generations of iterative refinement, the agent’s “hit rate” for significant signals climbed from 44% to a staggering 78%, eventually identifying 38 survivors that cleared multivariate horse races. A standout moment in the discovery trace was the “leverage-stock breakthrough,” where the agent shifted its paradigm from simple flow-based interactions to conditioning investment growth on balance-sheet fragility (leverage levels). This transition suggests the model isn’t just data mining; it is identifying structural economic principles, such as financial distress costs, to sharpen its ability to predict returns.

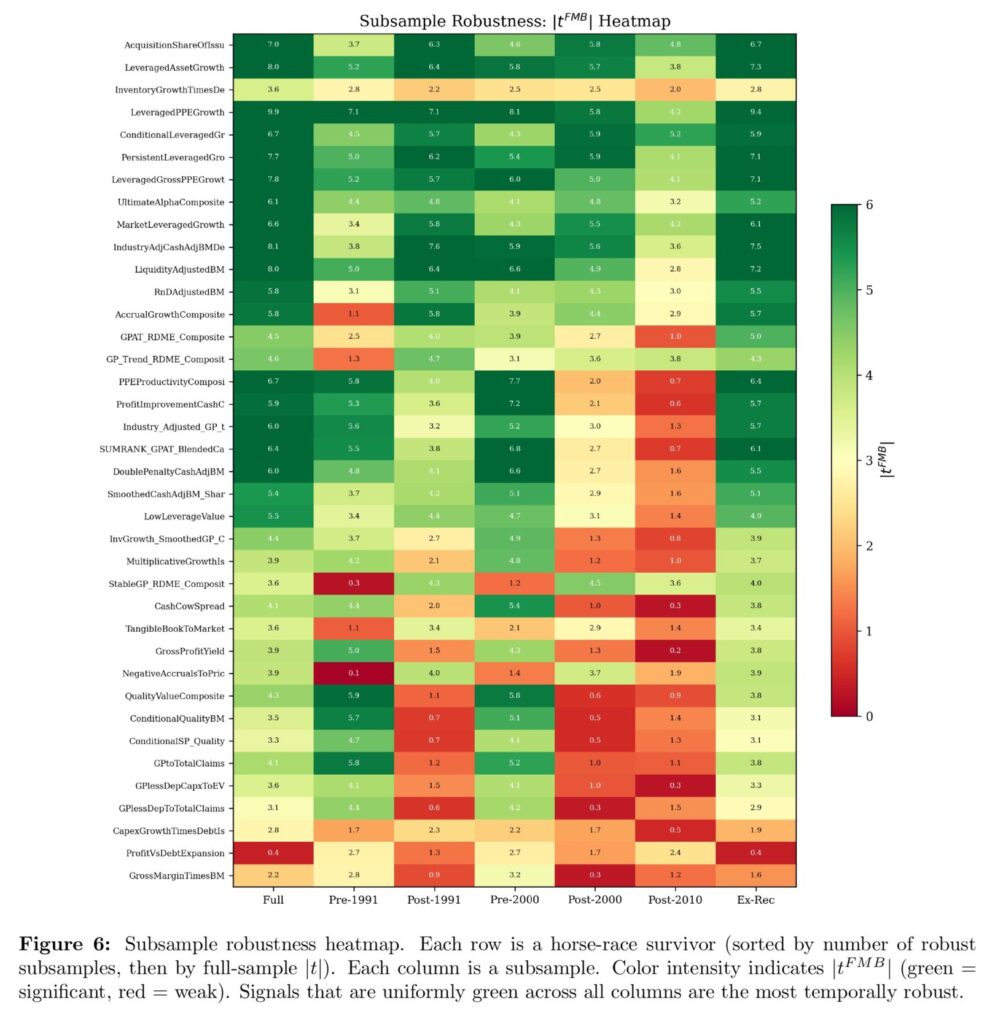

However, the “Anomaly Zoo” remains a treacherous place for even the smartest models. When subjected to a “full battery” of modern asset-pricing rigors—including multiple-testing corrections, spanning tests against 209 published anomalies, and factor-model absorption—the initial list of winners faced massive attrition. Most discoveries were absorbed by the Fama-French 6-factor or q-factor models, proving that many “new” ideas are simply familiar factor exposures in fancy accounting clothes. Yet, a select few, such as the UltimateAlphaComposite, survived the strictest filters, carrying genuinely incremental information. The takeaway for the practitioner is clear: while the AI research agent can navigate the signal space with a speed and transparency no human team can match, the bar for true novelty remains exceptionally high in an increasingly efficient market.

Authors: Huan Liu, Miao Liu, Zhizhe Liu, and Danqing Mei

Title: Can AI Do Financial Research? LLM-Guided Hypothesis Discovery in Asset Pricing

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6569258

Abstract:

We study whether an AI research agent can autonomously execute the hypothesis discovery loop in empirical asset pricing. We place a large language model inside a human-designed research environment comprising a symbolic language of interpretable accounting formulas, an automated validation layer, and a fixed empirical evaluation pipeline. The agent searches over interactions between economic themes such as profitability, investment, valuation, and quality, and updates its proposals over successive generations, where each generation is a new round of proposal, testing, and revision based on standardized empirical feedback. Across eight theme pairs and seven generations, the system proposes and evaluates 280 candidate signals on a microcap-excluded universe; 159 clear a conventional significance screen in the predicted direction, and 38 survive multivariate horse races designed to isolate signals with independent predictive content. We then subject these survivors to a full battery of modern asset pricing tests, including multiple testing corrections, multi-model factor spanning, and novelty tests against 209 published anomalies, and identify a small set that carries genuinely incremental information and survives the strictest filters. The paper introduces a transparent architecture for AI-guided hypothesis discovery in finance in which human researchers design the laboratory environment and the AI research agent autonomously carries out the discovery loop.

As ever, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“Our baseline evidence suggests that the framework supports systematic and interpretable signal discovery. As the agent progresses through evolutionary generations with iterative reflection, the quality of proposed signals improves meaningfully: the share of proposals that generate significant cross sectional return predictability rises from 44% in Generation 0 to 78% in Generation 5, and the strongest signal becomes materially sharper, with its absolute t statistic increasing from 4.47 to 6.26. Relative to a programmatic benchmark that searches within a single theme, the cross-theme AI-guided approach produces a substantially larger share of significant signals, higher Sharpe ratios, and stronger overall signal quality, consistent with the view that economically motivated interactions across themes are a fruitful source of cross-sectional variation in returns.

The main finding, however, is more disciplined than the baseline evidence. Because the agent revises proposals using outcomes computed on the same historical panel, the discovery loop is inherently an in-sample evolutionary search. We therefore place the inferential weight on a post-discovery validation framework rather than on the initial screen itself, and evaluate the discovered signals using multiple testing corrections (Harvey et al., 2016), skeptical Bayesian updating (Harvey, 2017), false discovery calibration (Harvey and Liu, 2020), factor spanning against leading benchmark models (Hou et al., 2020), conditional tests against 209 published anomalies (Chen et al., 2024), subsample robustness, and permutation tests. The progressive attrition, from 280 proposals to 159 significant to 38 independent to approximately 6–9 that survive the strictest modern statistical filters, is informative. It demonstrates, with transparent methodology, what happens when LLM-discovered signals face the full battery of tests that the asset pricing literature now considers standard. The attrition is large, but it is not total: a small set of signals carry genuinely incremental information.

The empirical evidence points to a clear division. The LLM excels at hypothesis search: it rapidly converges on combinations of accounting variables that produce statistically significant cross-sectional predictability. The interpretability constraint imposed by the expression language is a feature of the design rather than a limitation. By restricting the agent to symbolic expressions built from accounting quantities, the framework ensures that every proposal can be inspected, critiqued, and subjected to the full suite of asset pricing tests. Black-box signals cannot be tested against the CZ anomaly library or decomposed into factor loadings in the same way. Of 280 proposals, 159 clear the conventional screen, and hit rates nearly double from Generation 0 to Generation 5. The reasoning traces add a dimension that has no analogue in black-box machine learning or in conventional anomaly discovery. The case studies in Section 7 show an agent that diagnoses wrong-sign results, articulates structural insights about leverage stocks versus financing flows, identifies orthogonal alpha channels, and independently reconstructs known factor premia. Whether this constitutes “understanding” is a question we leave to others. What we can document is that the trace is specific, verifiable, and in several cases contains economic insights, such as the stock×flow conditioning principle, that are absent from the published literature.

The framework is portable to other empirical settings that share three features: a structured set of candidate primitives, a transparent evaluation pipeline, and enough data to discriminate signal from noise. Potential applications include credit risk modeling, corporate event studies, macroeconomic forecasting, and accounting measurement. In each case, the central requirement is that candidate hypotheses can be formalized in a constrained language and evaluated under a stable protocol. The present design does not accommodate signals that require unstructured text, high-frequency data, cross-firm network effects, or real-time information. Those extensions define a natural research frontier but require fundamentally different hypothesis languages and evaluation pipelines.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend