Quantpedia in June 2026

We hope you’re having a wonderful start to the summer! Here’s a quick overview of what’s new in Quantpedia Pro over the past few weeks.

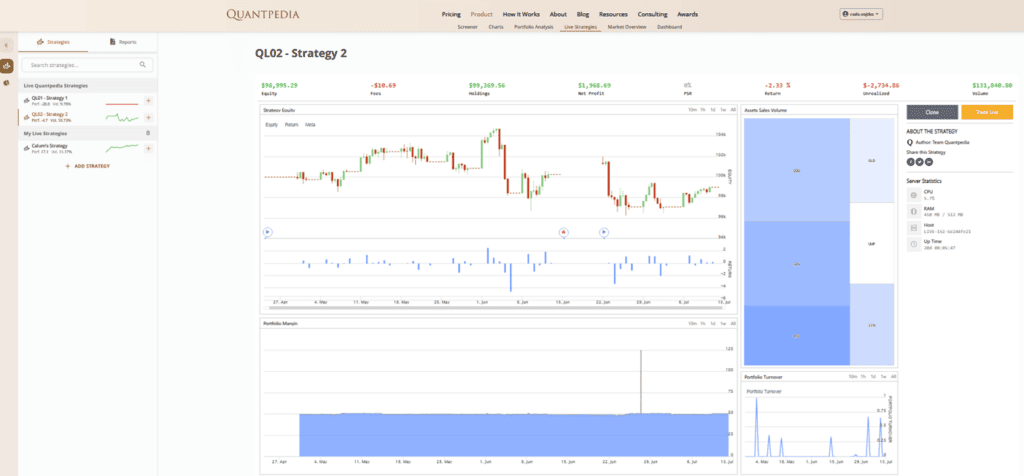

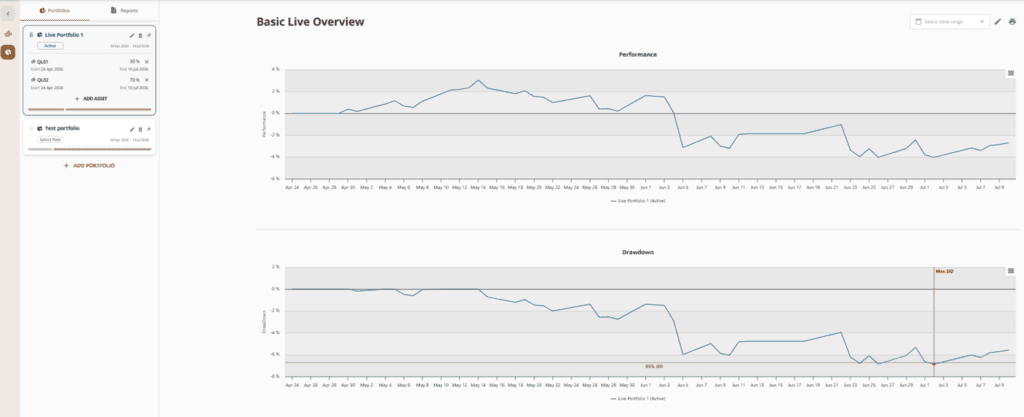

One of the biggest recent additions is the new Live Strategies section, which has been added to the main menu. This new area is designed to become the central hub for a growing suite of reporting tools based on live and paper trading strategies rather than historical backtests. As with our existing workflow, users can connect their own live or paper trading algorithms by entering the unique strategy hash generated by QuantConnect, allowing the strategy to be linked directly to the Live Strategies reporting interface on Quantpedia. Once connected, these live strategies can also be combined into portfolios, enabling users to analyze their aggregated performance and risk characteristics alongside individual strategy reporting.

At launch, the Live Strategies section features two strategies currently running on our QuantConnect servers: Active Dual Momentum GTAA and Dual Momentum Allocation between Physical Gold and Bitcoin, we introduced a new Dual Momentum GTAA Report in Quantpedia Pro. The first available report embeds QuantConnect’s comprehensive live strategy report, providing real-time insights into the strategy’s equity curve, margin utilization, current portfolio holdings, trading statistics, and other key performance metrics. This is only the beginning of the Live Strategies ecosystem. Over the coming months, we plan to gradually expand it into a complete performance and risk management toolkit for portfolios composed of live and paper trading strategies—not just historical backtests. This evolution moves Quantpedia Pro another step closer to becoming a comprehensive monitoring platform for managing live investment portfolios.

Secondly, don’t miss our latest YouTube interview featuring the winners of the Quantpedia Awards 2026. In this episode, I sit down with Michael Robbins, Professor at Columbia University, to interview Timo Wiedemann and Heiner Beckmeyer from the University of Münster about their award-winning paper, All Days Are Not Created Equal: Understanding Momentum by Learning to Weight Past Returns.

Together, we discuss how their novel machine learning approach enhances traditional momentum investing by assigning different weights to historical return observations instead of treating them equally. We also explore the practical implications of their research for quantitative investors, the key insights behind their methodology, and why momentum strategies may continue to offer attractive opportunities despite their recent headwinds. We hope you enjoy the conversation!

And finally, let’s also quickly recapitulate Quantpedia Premium development:

- 14 new Quantpedia Premium strategies have been added to our database.

- 3 new related research papers have been included in existing Premium strategies during the last month

- 7 new backtests were written in QuantConnect code. Our database currently contains, in total, over 960 strategies with out-of-sample backtests/codes.

Additionally, 8 new research reviews were published on the Quantpedia blog in the previous month:

Dual vs. Single Momentum in Commodities: Enhancing Risk-Adjusted Returns through Absolute Trend Filtering

Author: Cyril Dujava

Title: Dual vs. Single Momentum in Commodities: Enhancing Risk-Adjusted Returns through Absolute Trend Filtering

Why Most Portfolios Are Under Diversified

Author: David Mesicek

Title: Why Most Portfolios Are Under Diversified

Testing an AI-Assisted Research Workflow for Multi-Asset Pullback Strategy Discovery

Author: Sona Beluska

Title: Testing an AI-Assisted Research Workflow for Multi-Asset Pullback Strategy Discovery

Why Mean-Variance Optimization Breaks Down

Author: Vertox

Title: Why Mean-Variance Optimization Breaks Down

Understanding Investment Products Through Factor Analysis and Replication

Author: David Mesicek

Title: Understanding Investment Products Through Factor Analysis and Replication

Guardrails Make the Researcher: What an AI Agent Got Right (And Wrong) Replicating Nine Equity Anomalies

Author: Vlad Rodeski

Title: Guardrails Make the Researcher: What an AI Agent Got Right (And Wrong) Replicating Nine Equity Anomalies

Silicon vs. Satoshi: Tactical Asset Rotation Between NASDAQ-100 and Bitcoin

Author: Cyril Dujava

Title: Silicon vs. Satoshi: Tactical Asset Rotation Between NASDAQ-100 and Bitcoin

Quantpedia API as an On-Demand Factor Database

Author: David Mesicek

Title: Quantpedia API as an On-Demand Factor Database

Yours …

Radovan Vojtko

CEO & Head of Research

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend