Crowding in Commodity Factor Strategies

Nowadays, factor strategies are widely spread and used by practitioners, but this factor boom has given rise to some concerns. A key question is whether these strategies stay profitable once published and if they are not arbitraged away. Some strand of the literature suggests that there is a performance decay. A different view on performance decay is presented in the novel research of Kang et al. (2021), which indicates that the performance might be time-varying. Using the commodity market and premier anomalies such as momentum, basis, and value, the authors suggest a crowding in the factor strategies that predicts future performance. Crowded factors tend to underperform in future, and there is a significantly negative impact on the expected return. Moreover, the most substantial returns are connected with the least crowding activity. Therefore, the results are especially important for active factor traders.

Authors: Wenjin Kang, K. Geert Rouwenhorst and Ke Tang

Title: Crowding and Factor Returns

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3803954

Abstract:

This paper documents that crowding by market participants affects the expected return to popular factor strategies such as value, momentum, and carry. Using data published by the CFTC for commodity futures markets, we construct a direct measure of factor strategy crowding that is based on the aggregate positioning of market participants. We show that this crowding measure has a strong negative predictive impact on expected factor strategy returns. Historical factor strategy returns are accumulated primarily during periods of low crowding. We link variation in our crowding measure to macroeconomic fundamentals and suggest that the reduction of factor strategy returns is related to variation in the cost of arbitrage capital.

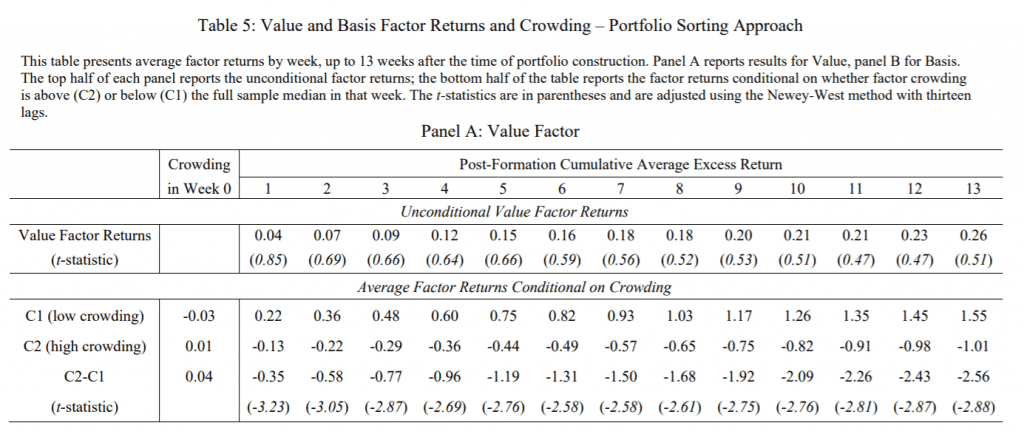

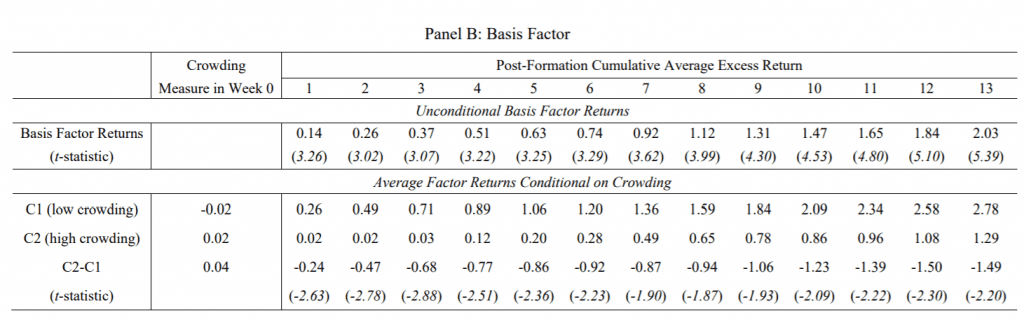

As always the results are best presented through tables and figures:

Notable quotations from the academic research paper:

“Many factor premiums, when first reported, may be biased upwards due to data snooping (Lo and MacKinlay (1990)) and therefore overstate the true returns that investors can expect out of sample. Under this explanation, the lower out-of-sample returns earned by investors are the reflection of a reversion to the mean of the underlying distribution of factor premiums. The second explanation, which we explore in this paper, is that the increasing popularity of factor investing reduces returns when strategies become more crowded over time. Absent natural clientele for factor “shorts” in the market, investors bid up prices of assets that provide high factor exposure, depressing those with low exposure, thereby gradually decreasing expected factor returns through the accumulation of investor flows.

In this study, we provide direct evidence that crowding influences subsequent returns in commodity futures markets using weekly investor positions data that is collected by the Commodity Futures Trading Commission (CFTC). The CFTC data on aggregate trader positions allows for the construction of holdings-based measures of crowding that covers the entire population of market participants. Because the CFTC reports trader positions on a weekly basis, the holdings can be observed at a frequency that is likely to be relevant for the rebalancing periodicity of factor strategies.

We define our measure of crowding as the “excess speculative pressure,” measured as the deviation of non-commercial traders’ positions from their long-term average in commodity futures markets, scaled by open interest. While this crowding metric is defined at the individual commodity level, it can be naturally aggregated to the (portfolio) strategy level. The starting point of our empirical analysis is to apply this measure in the context of

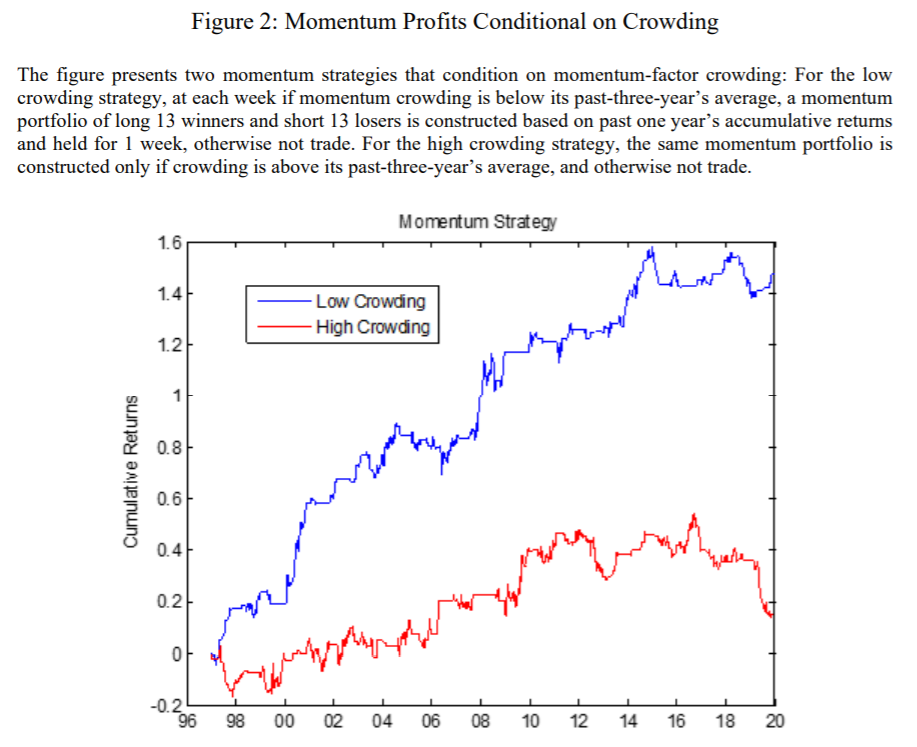

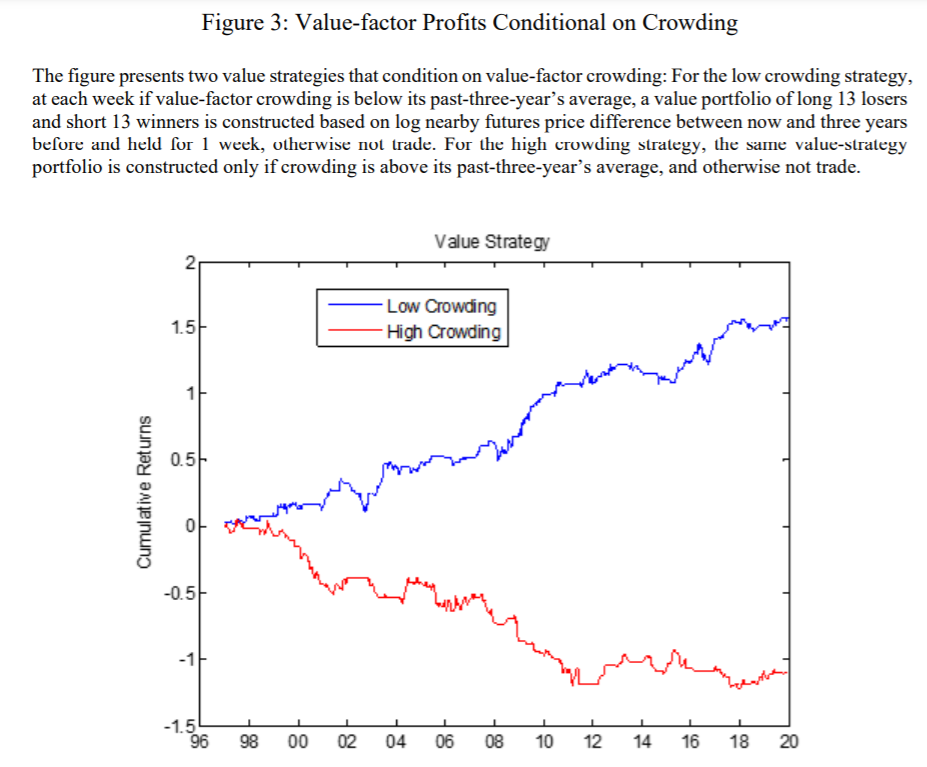

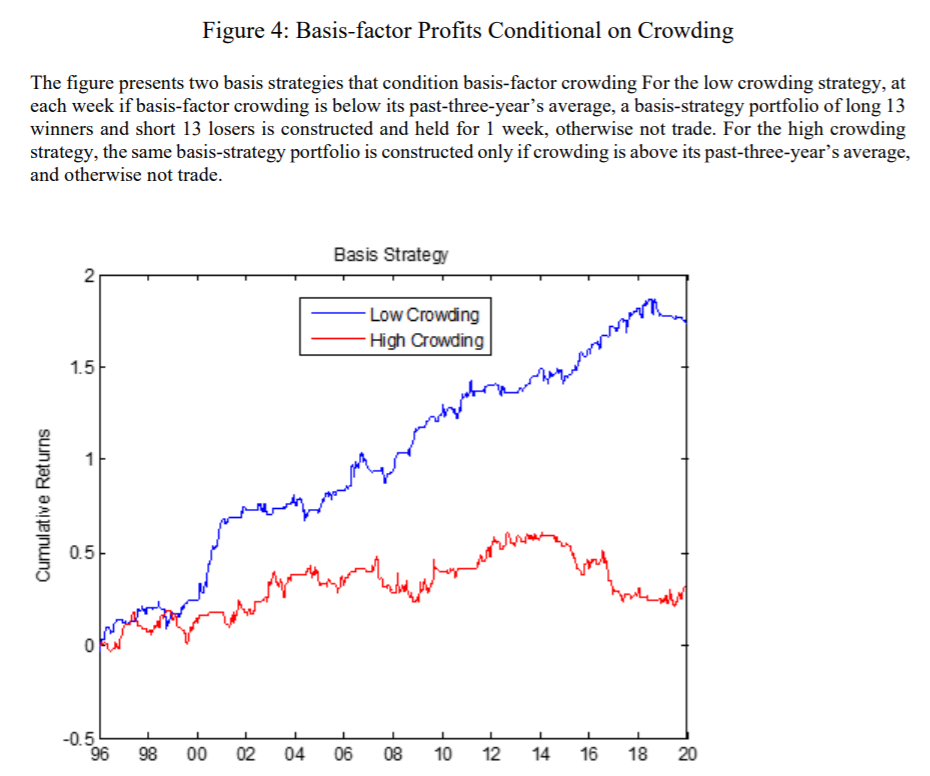

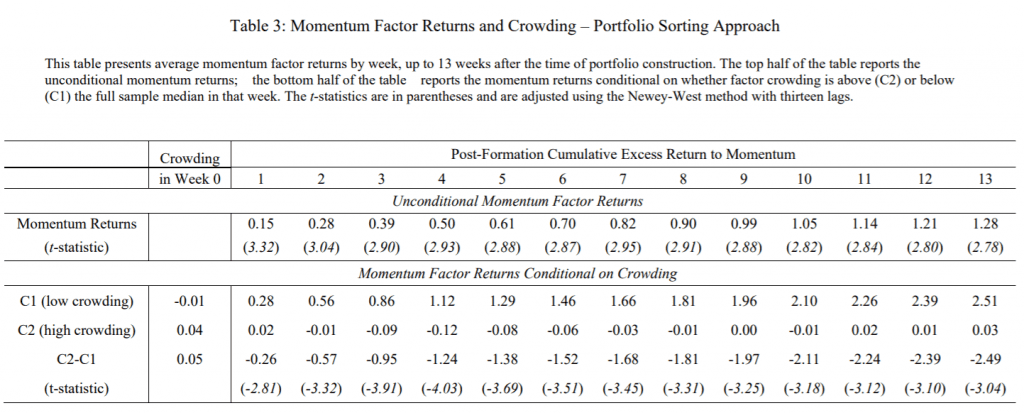

a momentum strategy, which is the most common factor strategy followed by Commodity Trading Advisors (CTAs). Commodity level crowding predicts subsequent commodity futures excess returns. Next, we find that commodity level crowding metrics, when aggregated to the portfolio level, help to predict factor strategy returns. For example, the returns to momentum investing are highest during months when the strategy is least crowded, and lowest when it is most crowded according to our definition. Specifically, our crowding measure helps to explain why the returns to commodity momentum investment have been low during the last several years of our sample. Our crowding metric is able to predict momentum returns after controlling for other factors that have been documented in the literature to predict commodity futures excess returns, such as past excess returns and recent investor flows into the market. A one standard deviation increase in our crowding metric decreases the return of the momentum factor by around 8% annualized, which is comparable in magnitude to the unconditional long-term average factor risk premium. Next, we use our measure of crowding to analyse the returns to basis (carry) and value strategies. Similar to momentum, periods of low crowding account for most of the profits to a carry strategy, and the return to investing in a commodity futures value strategy depends on whether the investment is made during periods of low or high crowding.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend