How Do Investment Strategies Perform After Publication?

In many academic fields like physics, chemistry or natural sciences in general, laws do not change. While economics and theory of investing try to find rules that would be true and always applicable, it is not that simple, there is a “complication“ – human. Psychology of humans is very complex. In the one hand, it creates anomalies in the market, that academics study and practitioners use. On the other hand, after an anomaly is discovered, often, the strategy becomes less profitable.

While for academics, it is just another research question, investors may be worried that the anomaly is arbitraged away, and it will become unprofitable in their portfolios. In this article, we will look deeper on whether the anomaly can be arbitraged away, if the profits are lower for the specific strategy once the strategy becomes well-known, and even if the strategies can be timed. Quantpedia‘s readers are often interested in these common topics, and we will try to shed some light on them.

Limits of arbitrage

It is not so easy to arbitrage excess returns for market anomalies.

Most of the anomalies have time-varying return, and a fair part of the return is preserved as arbitrage is not risk-free.

In the textbook arbitrage, there is no capital required and, there is no risk [1]. However, in practice, every arbitrage activity requires capital and is accompanied by risk. Also, professional arbitrage is a domain of highly specified and sophisticated investors, but their capital must be borrowed in some way. Hedge funds or other investment funds have external investors, or banks are regulated in the use of their leverage. According to the Shleifer and Vishny: The Limits of Arbitrage [1], specialized performance-based arbitrage may not be fully effective in bringing security prices to the fundamental values, especially in extreme circumstances. To be more precise, arbitrageurs tend to avoid extremely volatile positions. After all, the capital is not risk-free and also is not infinite.

Limits of arbitrage were also a focus of research by Liu and Mello: The fragile capital structure of hedge funds and the limits to arbitrage [5]. According to this paper, during a financial crisis, hedge funds cut their arbitrage positions and hoard cash. The capital structure of hedge funds have fragile nature, and if such nature is combined with low market liquidity, it creates a risk of coordination in redemptions among hedge funds that limits arbitrage. Therefore, hedge funds are more risk-averse and are not that willing to participate in the market when the coordination risk is factored in their decisions.

Profits of known strategies after publication

How long remain strategies profitable after they are published?

There is a decrease in profitability after anomaly/strategy is published (which is logical), but the returns do not weaken instantly. And a significant part of return remains.

If we want to focus on returns of strategies after their publication, McLean and Pontiff: Does Academic Research Destroy Stock Return Predictability? [4] give us some answers. They studied 97 variables which are considered to be able to predict stock returns by previous academic research. Portfolio returns were 26% lower out-of-sample and 58% lower during 5 years post-publication. The paper concludes that investors are aware of academic publications and learn about mispricing.

However, it is important to note, that diminishing of returns happens gradually over a longer period of time. Also, even after 5 years, a remarkable part of anomaly’s return is preserved. A known anomaly becomes a smart beta factor and can be still profitably used within a diversified portfolio.

Investors and academics as well could learn about some interesting idea while the research is still a working paper. When we consider returns out-of-sample and post-publication, it seems to be first come first serve. The publication of the academic paper is a long process that can take one or two years. However, by extracting the idea from working paper, a practitioner can buy some time. In Quantpedia, we are looking for academic research systematically twice a month to find working papers with novel ideas so that ideas can be extracted faster.

Factor timing

Can we compensate for decay in performance by correctly timing strategies/anomalies?

The literature recognizes various approaches to time anomaly strategies.

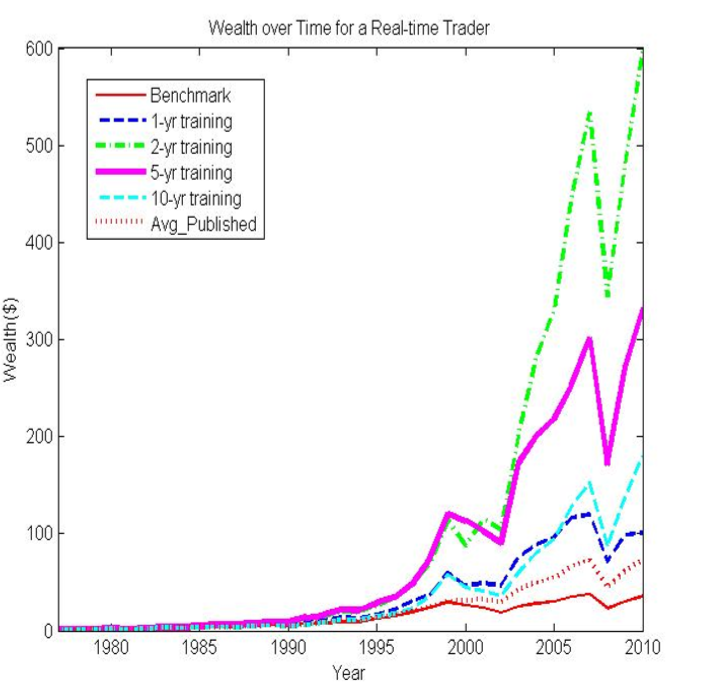

For example, Huang and Huang in Real-Time Profitability of Published Anomalies: An Out-of-Sample Test [3] consider a long-only strategy with a universe of published anomalies and each year, recursively pick the best performers during a given training period. According to this paper, the strategy can outperform the equity market, even in the presence of transaction costs. The results suggest that anomalies can persist even after controlling for data-snooping bias.

Results of such training and the idea can be seen on the following chart:

In this research, the sweet spot for training is 2-years. Unfortunately, these results are not that recent and therefore, should be revisited. In Quantpedia, we would like to revisit this topic soon.

Basu and Hung in Anomaly Timing [8] also constructed an anomaly timing strategy. They have constructed anomaly portfolios based on the lagged market returns. They have similar or larger Sharpe ratio, lower volatility and survive transaction costs. Such portfolios have significant alphas even to those factor models that are able to explain anomaly portfolios.

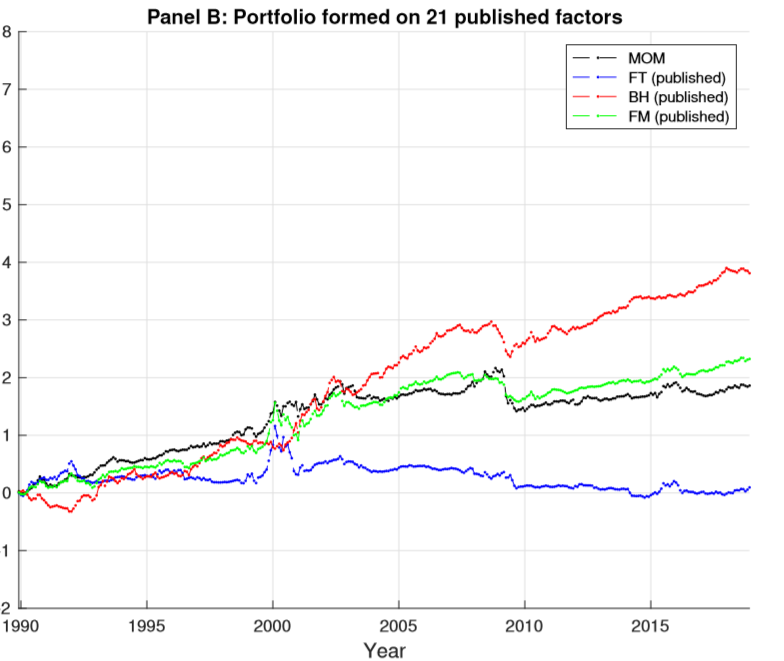

Yang in Decomposing Factor Momentum [6] found empirical evidence that supports a hypothesis that factor momentum (FM) could profit from consistently buying (selling) factors with positive (negative) average returns instead of factor timing. This is a result of decomposing factor momentum into two strategies. According to the author, the first strategy (FT) is a dynamic, one-sided factor timing portfolio. This strategy only trades the factor if the short-term one year return deviates from the prevailing mean and holds a zero factor position if they move in the same direction. As a result, this approach isolates the factor timing benefit from factor premiums. The second strategy (BH) holds a quasi-static factor position because the position is changed only if the sign of the prevailing mean return changes, but this occurs only rarely. As a result, this approach passively collects factor premiums. The results mentioned above can also be observed by looking at the cumulative return of factor portfolios based on already published factors. Factor portfolios are also compared with a traditional stock momentum.

As we can see in the following chart, the buy & hold strategy of published anomalies and also factor momentum strategy are both profitable.

Strategy rotation was also in the scope of interest of Zaremba and Umutlu in Strategies Can Be Expensive Too! [7]. This research uses a strategy-rotation approach by using the value spread, where the value spread of a long-short anomaly portfolio is simply the difference in valuation ratios between the long and the short sides of the trade. Aforementioned is simply a measure of how cheap or expensive a given strategy currently is. As the research shows, the value spread can be utilized to select the future winners from a broader set of strategies and later on, those strategies are used for country asset allocation.

Other investors

Do investors mimic/copy ideas out of academic research completely and without change?

Not at all.

Academic research is usually just a source of inspiration. In practice, every portfolio manager or investor implement ideas differently. No company uses strategies as they are described (and I am sure, you, our readers, do not use research this way too). Each investor almost always uses a different definition of factor strategies or mix them together differently to better suit their needs better.

Let’s see, for example, our simple Quantpedia’s case study of calendar strategies. In this study, we selected four seasonal strategies from our Screener. But we used different trading rules than those stated in source research papers, plus we added a risk filter. Therefore, the model positions are different from the original ideas in research. If somebody else would implement this composite strategy, they would probably use a different risk filter, different rules and different weighting (and different strategies). However, this dilutes the number of practitioners that trade the exact same strategy and their positions in time would be different.

Moreover, in the first case study, we utilize only SPY ETF as a trading instrument. In our following work, we added more ETFs, and we choose them into our calendar portfolio based on their momentum for three different periods. We definitely do not state that our implementation is the best, but we aim to provide an example that every idea is adapted differently, which dilutes the concentration of trading positions.

Apart from different trading instruments within the same asset class or different risk-filters or lookback periods and holding periods, there is another major possibility to utilize the idea, but avoiding the risk of concentration. If one anomaly is discovered in one asset class, many researchers tend to explore whether the same concept can be utilized in a different asset class. For example, momentum started as an equity anomaly, but later it was found everywhere as Asness, Moskowitz, and Pedersen in Value and Momentum Everywhere [2]. Such thinking is not exclusive to researchers and practitioners tend to do the same.

Conclusion

So, what’s the conclusion? Arbitraging strategies away is not that simple, there are limits to arbitrage, and most importantly, the capital is nor infinite, nor risk-free. No doubt, profits after publication would be lower. Since the publication of a research paper is a long process, the decrease in performance could be avoided by early-adopting the ideas by studying working papers. Moreover, it is possible to rotate anomalies, trying to pick the best performers or include a set of anomalies in a diversified portfolio.

It helps to include the most recent research and anomalies. Academic research is usually not used without changes but as a source of ideas for implementation. Investors tend to adapt the concepts to their preferable investment universe, asset classes, risk-aversion, the composition of their existing portfolio, rebalancing period or combine them with other ideas. Aforementioned reduces the concentration of trading the same strategy because this usually does not happen.

Authors:

Radovan Vojtko, CEO

Matus Padysak, Quant Analyst

Are you looking for strategies applicable in bear markets? Check Quantpedia’s Bear Market Strategies

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Related Literature

[1] Andrei Shleifer, Robert W. Vishny, The Limits of Arbitrage, The Journal of Finance, Vol. LII, No. 1, 1997, Pages 35-55. http://scholar.harvard.edu/files/shleifer/files/limitsofarbitrage.pdf

[2] Asness, Cliff S. and Moskowitz, Tobias J. and Pedersen, Lasse Heje, Value and Momentum Everywhere (June 1, 2012). Chicago Booth Research Paper No. 12-53; Fama-Miller Working Paper. Available at SSRN: https://ssrn.com/abstract=2174501 or http://dx.doi.org/10.2139/ssrn.2174501

[3] Huang, Jing-Zhi Jay and Huang, Zhijian, Real-Time Profitability of Published Anomalies: An Out-of-Sample Test (March 12, 2014). Quarterly Journal of Finance, Volume 3, Issue 3n4, 2013. Available at SSRN: https://ssrn.com/abstract=1571706 or http://dx.doi.org/10.2139/ssrn.1571706

[4] McLean, R. David and Pontiff, Jeffrey, Does Academic Research Destroy Stock Return Predictability? (January 7, 2015). Journal of Finance, Forthcoming. Available at SSRN: https://ssrn.com/abstract=2156623 or http://dx.doi.org/10.2139/ssrn.2156623

[5] Xuewen Liu, Antonio S. Mello, The fragile capital structure of hedge funds and the limits to arbitrage, Journal of Financial Economics, Volume 102, Issue 3, 2011, Pages 491-506, ISSN 0304-405X, https://doi.org/10.1016/j.jfineco.2011.06.005. (http://www.sciencedirect.com/science/article/pii/S0304405X11001498)

[6] Yang, Hanlin, Decomposing Factor Momentum (March 29, 2020). Available at SSRN: https://ssrn.com/abstract=3517888 or http://dx.doi.org/10.2139/ssrn.3517888

[7] Zaremba, Adam and Umutlu, Mehmet, Strategies Can Be Expensive Too! The Value Spread and Asset Allocation in Global Equity Markets (2018). Applied Economics, 2018, 50 (60): 6529-6546. Available at SSRN: https://ssrn.com/abstract=3332931

[8] Basu, Devraj and Hung, Chi-Hsiou, Anomaly Timing, Available at: www.fin.ntu.edu.tw/~conference/conference2008/proceedings/proceeding/5/5-1(A45).pdf

Share onLinkedInTwitterFacebookRefer to a friend