Do Copycat CTAs Outperform Individualistic CTAs?

Our society teaches us, that it is good to be different. That our trading strategy must be always unique, creative and individualistic. It is boring and unprofitable to be the “average”, to do what the others do. And then, there is a research paper written by Bollen, Hutchinson and O’Brian which offers the opposite view. Their analysis explains there exist one hedge fund style where everything is the other way round – trend-following CTA funds. Their interesting (but for some maybe controversial) paper shows that CTAs with returns that correlate more strongly with those of peers have higher performance. It appears that CTA strategy conformity is a signal of managerial skill. Now, that is an eccentric idea 🙂

Authors: Bollen, Hutchinson and O’Brian

Title: When It Pays to Follow the Crowd: Strategy Conformity and CTA Performance

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3481243

Abstract:

Prior research in hedge fund and mutual fund management finds a positive relation between portfolio distinctiveness and subsequent performance, suggesting that strategy differentiation is associated with superior skill. We find that CTAs with returns that correlate more strongly with those of peers feature higher performance and are more highly exposed to a time series momentum factor. In contrast to hedge funds and mutual funds, CTA strategy conformity appears to be a signal of managerial skill. These results indicate that a common trend following strategy drives CTA returns and that CTAs offer investors an opportunity to invest in momentum.

Notable quotations from the academic research paper:

“Given the importance of CTAs in institutional portfolios, recent evidence of their generally poor performance challenges the notion that these vehicles provide a benefit. Given the robust evidence of profitability in commodity futures markets, it seems likely that at least some CTAs can offer investors a benefit.

This paper studies whether investors can select a subset of available CTAs with a reliably higher than average likelihood of generating attractive future returns, motivated by the aforementioned momentum profits in futures markets. We draw from the literature on hedge fund performance prediction. A widely accepted explanation for the success of some hedge fund managers attributes their performance to the ability to identify unique profit opportunities. Price pressure from their actions and those of copycat traders eventually eliminates the potential for abnormal returns, requiring managers to continually search for new and different trades.

While Titman and Tiu (2010) and Sun et al. (2012) show that hedge funds with differentiated trading strategies outperform, we conjecture that for CTAs the opposite may be true. To understand why, note that Sun et al. (2012) identify two counteracting mechanisms which might weaken the positive association between strategy distinctiveness and hedge fund performance. First, as described by Goetzmann et al. (2003), unskilled managers may take excessive idiosyncratic bets in the hopes of achieving extreme levels of performance and compensation, given the typical hedge fund performance contract. Consistent with this notion, Bollen (2013) shows that hedge funds with high idiosyncratic risk (as measured by low factor model explanatory power) fail at a higher rate than other funds. Second, and more relevant for our study, Shliefer and Vishny (1997) argue that funds face limits to arbitrage when their investors are sensitive to short-term losses. Consequently, skilled managers may choose not to attempt to correct a mispricing in the market, but rather to profit from its continuation.

Since commodities feature robust time series momentum, as shown by Moskowitz et al. (2012), CTA managers must decide whether it is more profitable to follow the trend or pursue more distinct trading strategies.

In this paper, we contribute to the growing literature on strategy distinctiveness by measuring the relation between SDI (Strategy Distinctiveness Index) and subsequent CTA performance. To preview our results, we find that CTAs with more differentiated strategies underperform those that conform, and explain this counterintuitive finding as a failure to pursue profitable momentum opportunities that characterize successful CTA management.

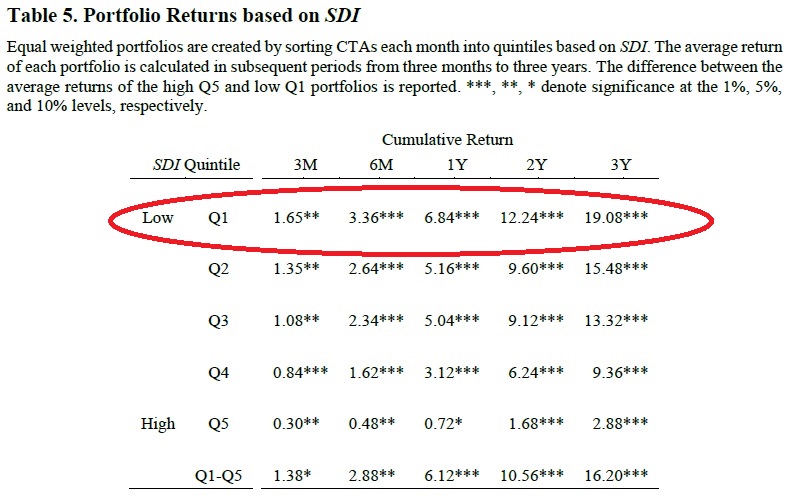

We find that higher strategy distinctiveness is associated with lower future performance, exactly opposite to the finding for hedge funds. Funds with less distinctive strategies perform consistently better even after controlling for risk and style differences.

Second, we provide an empirical explanation for our findings. We also show that the relationship between SDI and subsequent CTA performance is dependent on the profitability of momentum. When the returns to momentum are positive, there is an inverse relationship between SDI and CTA performance, i.e., the CTAs that conform outperform. When the returns to momentum are negative, for example when a rising market crashes or a falling market rallies, then there is a positive relationship between SDI and CTA performance.

Third, we assess whether investors can use SDI to select a realistic subset of CTAs that reliably offers a realizable incremental benefit. Following a simulation procedure developed in Bollen et al. (2019), we draw five CTAs at random from each SDI quintile once per year throughout our sample period and hold for one year. The process yields a time series of returns for a portfolio of five CTAs drawn from each quintile. We repeat 1,000 times to generate a distribution of outcomes. The portfolios selected from the lowest SDI quintile generate an average return of 0.41% per month versus just 0.04% for the portfolios selected from the highest SDI quintile. Differences between the risk-adjusted performance of the portfolios drawn from the top and bottom quintiles are all highly significant.”

Are you looking for strategies applicable in bear markets? Check Quantpedia’s Bear Market Strategies

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend