Do Prediction Markets Predict Macroeconomic Risk?

The U.S. (and the world’s) economy is currently entering a recession. Right now, everybody can see it, the only question is how deep it will be. But is it possible in a real-time predict if the economy will go into a recession? And will that information help us to better set % allocation of equities in our portfolio? Most of the macroeconomic data shows recession in macroeconomic reports with a significant lag. There are multiple different forecasting models which try to predict recession or at least estimate the probability that we are entering into one. We are presenting one interesting research paper written by Jonathan Hartley which shows that prediction markets (betting markets created for the purpose of trading the outcome of events) can be successfully used as a complementary tool in various economic forecasting tools. Prediction markets can be used to measure risk in U.S. equities, credit spreads, the U.S. Treasury yield curve, and U.S. dollar foreign exchange rates.

Author: Hartley

Title: Recession Prediction Markets and Macroeconomic Risk in Asset Prices

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3524686

Abstract:

This paper analyzes recession prediction markets from Intrade and PredictIt where individuals bet on the binary outcome of a recession occurring by a certain date. Using a time series of such historical recession prediction market data to measure macroeconomic risk in a variety of asset classes, we find a 1% increase in ex-ante recession prediction market probability is associated with a -0.29% decline in U.S. equity markets and a -0.77 basis point decrease in the 10-Year U.S. Treasury yield. Recession prediction markets also explain a significant amount of the variation in credit spreads, the U.S. Treasury yield curve, and U.S. dollar foreign exchange rates but cannot explain the value and momentum anomalies in equity markets as well as the U.S. treasury term premium.

Notable quotations from the academic research paper:

“One overlooked area which produces macroeconomic risk data is the area of prediction markets which offer revealed preference approach to assessing the probability of whether certain macroeconomic events occur, speci cally recessions. This paper uses recession prediction markets as a tool to measure macroeconomic risk in asset prices.

One key virtue of recession prediction markets is that they allow us to measure macroeconomic risk in a contemporaneous fashion. One challenge with using macroeconomic data such as GDP or unemployment releases is that it is unclear to what degree their values are already expected and priced in to financial markets. Prediction markets allow us to use a simple reduced-form regression (rather than a structural macroeconomic model) to measure the impact of macroeconomic risk on asset prices.

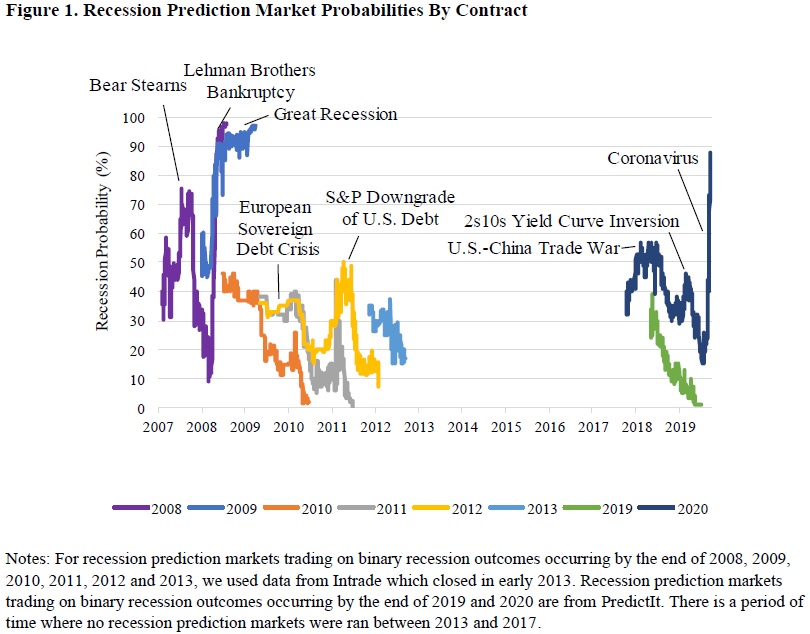

For recession prediction markets trading on binary recession outcomes occurring by the end of 2008, 2009, 2010, 2011, 2012 and 2013, we used data from Intrade. For recession prediction markets trading on binary recession outcomes occurring by the end of 2019 and 2020, we used data from PredictIt.

From the equity factor regressions which regress factors from Fama and French (2015) and a momentum factors, a 1% increase in recession prediction market probability is associated with a -0.35% decline in U.S. equity markets which is statistically signi ficant at the 1% level. This suggests that a jump from 15% (the ex-post post-war average annual recession likelihood) to 100% likelihood of a recession is associated with an approximate 25% decline in the U.S. equity market.

A 1% increase in recession prediction market probability is associated with a 0.019% (1.9bp) increase in the BAA default spread and a 0.008% (0.8bp) increase in the AAA default spread which are both statistically signi cant at the 1% level.

A 1% increase in U.S. recession prediction market probability is associated with a -0.086% (8.6 bp) decrease in USD/EUR , a -0.123%(12.3bp) decrease in USD/GBP and a 0.104% (10.4 bp) increase in USD/JPY which are all statistically signi cant at the 5% level or better.

Are you looking for strategies applicable in bear markets? Check Quantpedia’s Bear Market Strategies

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend