Do S&P500 0DTEs Options Increase Market Volatility?

Recent market action has once again underscored how rapidly volatility can surface across asset classes, as evidenced by pronounced price swings in gold, silver, and cryptocurrency markets. Such episodes routinely revive debate within the quantitative community about structural drivers of intraday instability, with particular attention paid to the growing prominence of S&P 500 zero-days-to-expiration (0DTE) options. The rapid proliferation of these ultra-short-dated contracts has fueled concerns among practitioners, regulators, and exchange operators that concentrated option activity may transmit destabilizing hedging flows into the cash equity market. At the same time, the paper under review challenges this prevailing spillover hypothesis, suggesting that the availability of 0DTE options systematically alters market-makers’ hedging exposures in a way that may dampen, rather than amplify, realized index volatility. So, do 0DTE options truly increase market volatility?

The empirical core of the study documents a robust negative relation between 0DTE trading days and realized S&P500 volatility. Mechanistically, the effect is driven by changes in intermediaries’ net gamma and delta hedging demands: positions in longer‑dated options accumulate prior to expiry and roll down the term structure, increasing market‑makers’ instantaneous hedging needs in a direction that forces them to trade against contemporaneous index moves. This counter‑directional trading behavior functions as liquidity provision at the index level, producing stronger intraday order‑flow reversals, muted momentum returns, and lower intraday volatility. Importantly, the paper shows that the attenuation is not primarily a consequence of trading 0DTEs on their expiration day per se, but of the dynamic, multi‑day inventory management that converts earlier non‑0DTE positions into 0DTE exposures.

The findings carry substantive implications for market microstructure and asset pricing. First, they reveal that intermediaries engage in dynamic hedging across multiple days, so static inventory models understate the temporal propagation of option‑market exposures into the cash market. Second, while the average effect is volatility‑dampening—arguably beneficial for liquidity seekers—the time‑varying nature of hedging needs constitutes a novel aggregate risk factor with potential cross‑market pricing consequences for both equities and options. Finally, the results inform the regulatory conversation around SPXW rollouts and the growth of weekday expirations: policymakers should weigh the documented liquidity‑provision benefits against the possibility that episodic shifts in hedging demands create concentrated, path‑dependent risks. So, do 0DTE options not increase market volatility? — The evidence here suggests the answer is nuanced: on average, they do not increase volatility, but they introduce a distinct, dynamic channel of aggregate risk.

Authors: Greg Adams et al.

Title: Do S&P500 Options Increase Market Volatility? Evidence from 0DTEs

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5641974

Abstract:

The recent surge in trading of S&P500 zero-days-to-expiration options (0DTEs) raises concerns that market makers’ hedging activities can spill over from the option market, destabilizing the aggregate stock market. On the contrary, we show that the presence of 0DTEs dampens market volatility through a shift in market makers’ hedging needs. Importantly, this shift occurs not due to trading 0DTEs on their expiration day but due to positions in longer-dated options accumulated earlier and becoming 0DTEs. Intraday evidence also supports the causal hedging mechanism: intraday variation in market makers’ hedging needs predicts stronger order-flow reversals, lower momentum returns, and lower volatility.

As continually, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“We provide compelling evidence that the presence of 0DTEs dampens the S&P500 index volatility, on average, and that the market makers’ hedging needs underpin this effect. The results highlight the importance of specialized intermediaries in integrating option and equity markets (Arrow, 1964). It is remarkable that this role can lead to a reduction in aggregate volatility in today’s S&P500 market despite the potential limits to the capacity of intermediaries (Grossman and Miller, 1988) or the presence of noise traders (Stein, 1987).

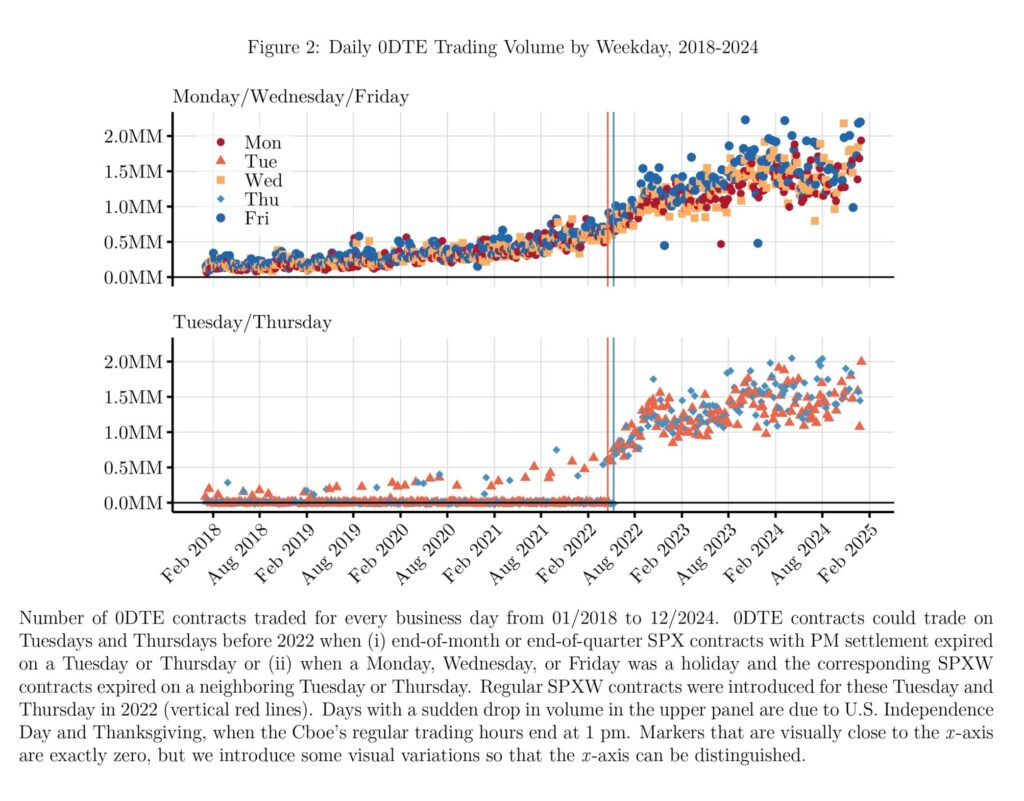

We offer causal evidence linking 0DTEs to the market makers’ hedging needs and the underlying market volatility. First, we document that the volatility of S&P500 index returns is lower by 60 annualized basis points (bps) on days when 0DTE trading is present, on average. We identify this effect using exogenous variation in the presence of 0DTEs on Tuesdays and Thursdays before May 2022. The difference between the volatility across weekdays disappears once 0DTE options start trading every business day in 2022.3

Second, we show that the presence of 0DTE trading shifts the market makers’ hedging needs in the direction that attenuates market volatility. We follow the logic of the hedging mechanism outlined in Ni, Pearson, Poteshman, and White (2020) and measure the fraction of S&P500 shares the option market makers would need to buy to hedge their option portfolio against a one percent decline in the index, and vice versa. We find that market makers as a group have hedging needs of about one percent before 2022, and that the presence of 0DTEs on a given day increases those hedging needs by 0.15 percentage points on average. Therefore, hedging activity in the underlying market offers a plausible causal mechanism linking the presence of 0DTE trading to the lower S&P500 volatility. Using a two-stage regression, we estimate a multiplier of −4 from the aggregate market makers’ hedging needs to volatility, meaning that a 1 bp increase in how much market makers need to trade against the direction of S&P500 returns to hedge option positions is associated with a 4 bps decrease in realized volatility.

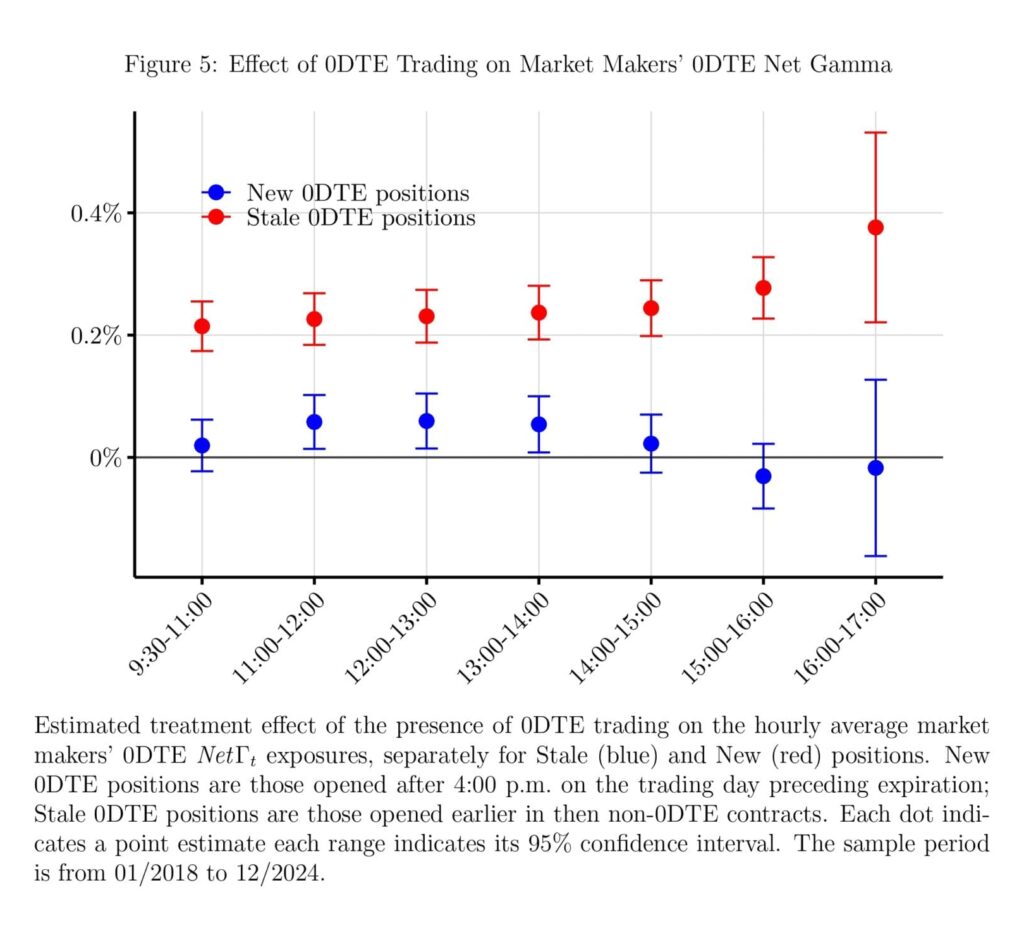

Third, the evidence reveals that positions established before the expiration day drive the higher market makers’ hedging needs when 0DTEs are present. To show this, we split market makers’ hedging needs into two components: (i) a component due to new option positions accumulated in a given recent interval and (ii) a component due to positions accumulated earlier. We find that the increase in hedging needs when 0DTEs are present stems from pre-existing positions in longer-dated options accumulated in earlier days or weeks that subsequently become 0DTEs, rather than from the intraday trading of 0DTE contracts. These pre-existing market makers’ positions raise the hedging needs by 24 bps during the expiration day on average. By contrast, the new 0DTE positions accumulated on the expiration day contribute 3 bps, while non-0DTE hedging needs even decrease when 0DTEs are present.

[…] we document four causal facts due to the presence of 0DTE trading: (i) the S&P500 intraday realized volatility is lower on days when 0DTE contracts are present, (ii) market makers have larger net gamma on these expiration days, (iii) this larger exposure comes from 0DTE net gamma present at the start of the expiration day and due to pre-existing option positions, and (iv) market makers maintain a positive portfolio net gamma throughout the 0DTE expiration day.

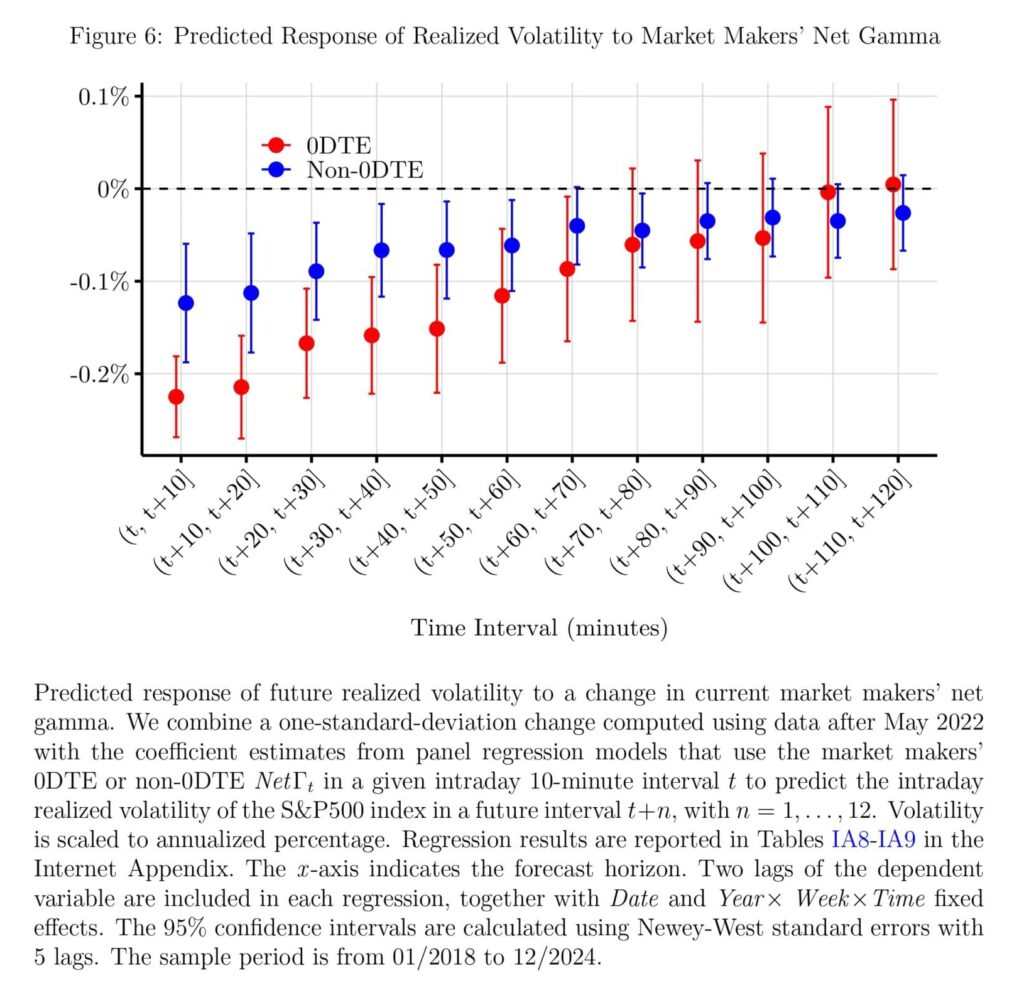

First, variations in market makers’ net gamma predict lower S&P500 volatility in the next 10 minutes, and this effect dissipates after about one hour. Second, a higher net gamma predicts a stronger reversal pattern in the intraday order flow of E-mini futures. The direction is consistent with the observed dampening effect on volatility, and the effect dissipates after one hour. Third, a higher net gamma predicts a negative momentum in high-frequency returns, which is consistent with both the effects on order flows and volatility. Overall, the pattern across these predictive relationships consistently points to the hedging activity of the market makers as a central mechanism that dampens the index volatility. In addition, the effect on average returns suggests that high-frequency hedging of market makers’ portfolio with positive net gamma can be profitable on average when transaction costs are low.12 Finally, the results highlight that hedging activities of option market makers’ may have a first-order effect on the properties of intraday returns, order flow, and realized volatility of the S&P500.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend