Do SPACs Generate Abnormal Returns?

Special Purpose Acquisition Companies (SPACs) raise capital through IPO under special conditions intending to acquire an existing company (private equity). On the one hand, it looks like an attractive opportunity for investors – SPACs bring a lot of excitement and prospects of large profits since the management can find a valuable opportunity. If no acquisition is made, then investors simply get their money back. For firms that are being acquired, it is a much easier and faster way how to get publicly traded – without investment banks and IPOs. On the other hand, SPACs are very speculative and even frequently overpriced, which attracts many critiques. In fact, the speculation in SPACs raise eyebrows of many professionals. While SPACs are nothing new, recently they have got quite popular, which raises several questions: are they worth attention or do even they bring abnormal profits? A fascinating insight into SPACs provides a novel research paper of Chong et al. (2021). The study explains the fundamental principles of SPACs, but most importantly, it shows us the risks and returns of such investments. Despite the popularity and the seemingly attractive opportunity of SPACs, results show us that the invested capital could be instead used elsewhere. Although the success depends on the sector in which is the SPAC interested or whether the acquisition was successful, overall, it is hard to find abnormal returns in these investments.

Authors: Eason Chong, Emily Zhong, Fannie Li, Qianyi Li, Saharsh Agrawal and Qingquan Zhang

Title: Comprehensive Study of Special-Purpose Acquisition

Company (SPAC): An Investment Perspective

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3862186

Abstract:

Special-Purpose Acquisition Company (SPAC) has been a widely discussed topic since 2020 and the trend continues in 2021. The paper provides a comprehensive overview of SPACs, including their capital structure, market participants, characteristics of their management teams, and factors contributing to its uprise. Abnormal returns analysis were performed on SPACs with both the CAPM and the Fama-French 3-Factor models. Results show that SPACs generally have negative alpha in different periods and their Sharpe ratios are lower than that of the S&P 500 index. However, most SPAC sectors that have completed their merger-and-acquisition illustrate positive excess returns. Then a SPAC investment strategy was designed using trading volume as a major sentiment indicator. The strategy outperforms the S&P 500 index with a Sharpe ratio of 2.59 in the back-test, suggesting its potential to yield considerable profit in SPACs investment.

As always we present several interesting figures:

Notable quotations from the academic research paper:

“SPAC is a listed shell corporation with the purpose of acquiring a private company, thus making it public without going through the traditional initial public offering process (Domonoske (2020), Broughton and Maurer (2020)). According to the U.S. Securities and Exchange Commission (SEC), a SPAC is created specifically to pool funds in order to finance a merger or acquisition opportunity within a set time-frame (SEC (2020)). SPAC has 24 months after the IPO to search for a target business and complete the acquisition. The acquisition decision must be approved by the shareholders, otherwise the management team would have to resume target searching.

SPAC will fund a trust account with 100% or more of the gross proceeds of the IPO. Approximately 98% of this amount will be funded by public investors and 2% by sponsors. The trust fund is used primarily to finance the business combination or redemption of common stock pursuant to

a mandatory redemption offer. (Layne et al. (2018))

From the investors’ perspective, it is less risky for the them to invest in a SPAC than ordinary stocks if they buy at around $10, which is close to the SPCA’s cash value. When the SPAC successfully acquire the targeted private company after gaining the majority of shareholders’ approval within the 24-month period, sponsors and investors are likely to earn a profit. On the other hand, if the SPACs fail to complete the acquisition due to any reason, sponsors of SPACs will redeem the public shares, and the investors will get their money back (Layne et al. (2018)). Therefore, to the investors, the loss will be limited to the opportunity cost of their money invested during the investment period, plus the management and underwriting.

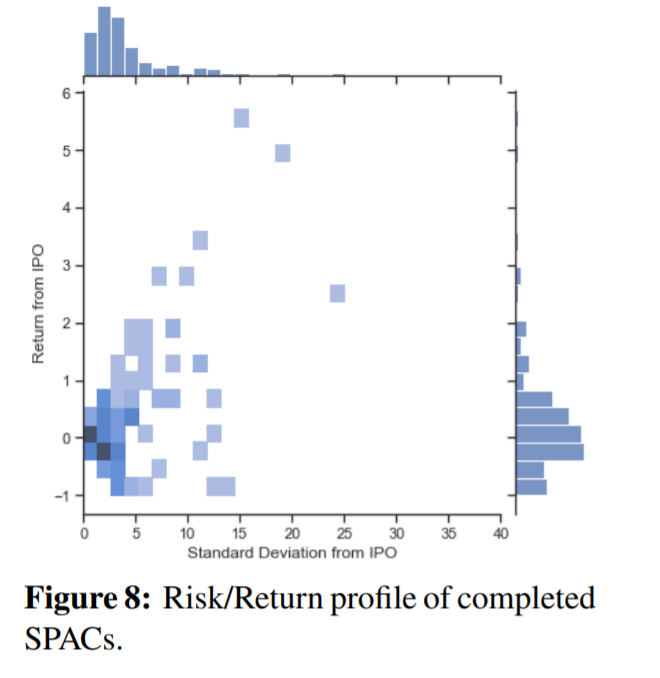

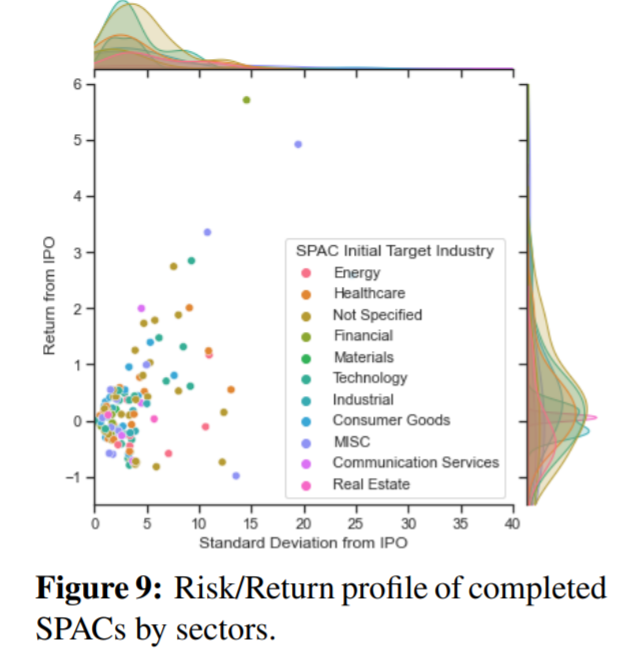

The return and standard deviation distributions of SPACs from

their IPO were positively related, similar to other stocks in the market. No valid relationship between SPACs’ sectors and their risk/return profile can be observed.

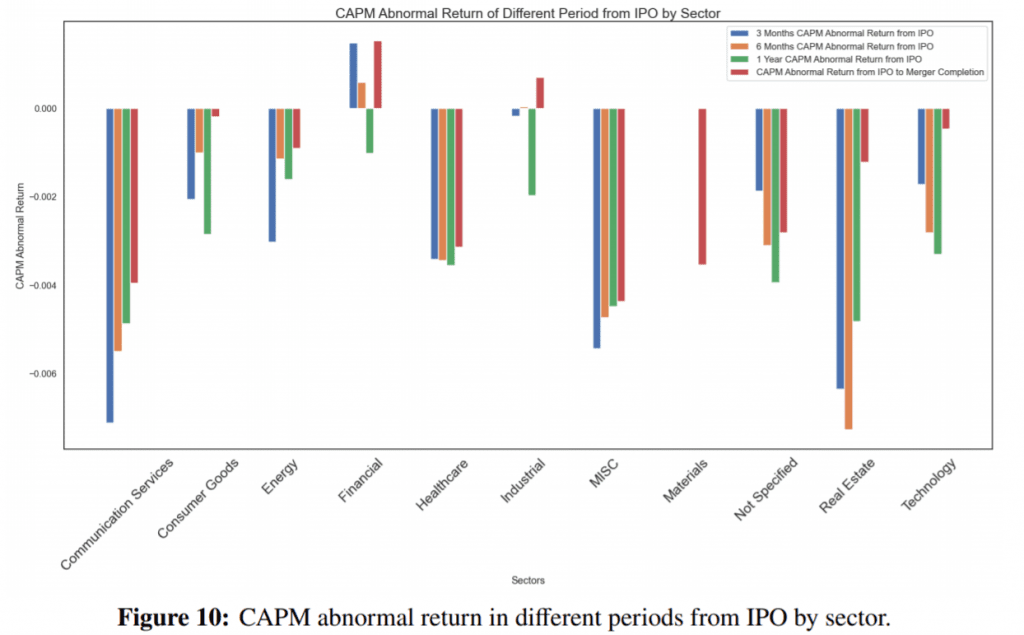

CAPM was used to calculate the SPACs’ abnormal return (alpha) in different time periods. Individual SPACs’ abnormal returns were then grouped into sectors for the calculation of the average abnormal return of that sector. It was observed that only SPACs in the Financial and Industrial sectors have positive average abnormal return (Figure 10). SPACs in the Financial sector have positive abnormal return in the periods of 3-month from IPO, 6-month from IPO, and between IPO and Merger Completion; meanwhile SPACs in the Industrial sector only showed positive average abnormal return in the periods of 6-month from IPO, and between IPO and Merger Completion.

However, the positive abnormal returns of Financial sector and Industrial sector are low. Similar patterns can be observed in the Three Factors Model analysis, except that the average abnormal return in the period of 6-month from IPO in the Industrial sector turns negative.

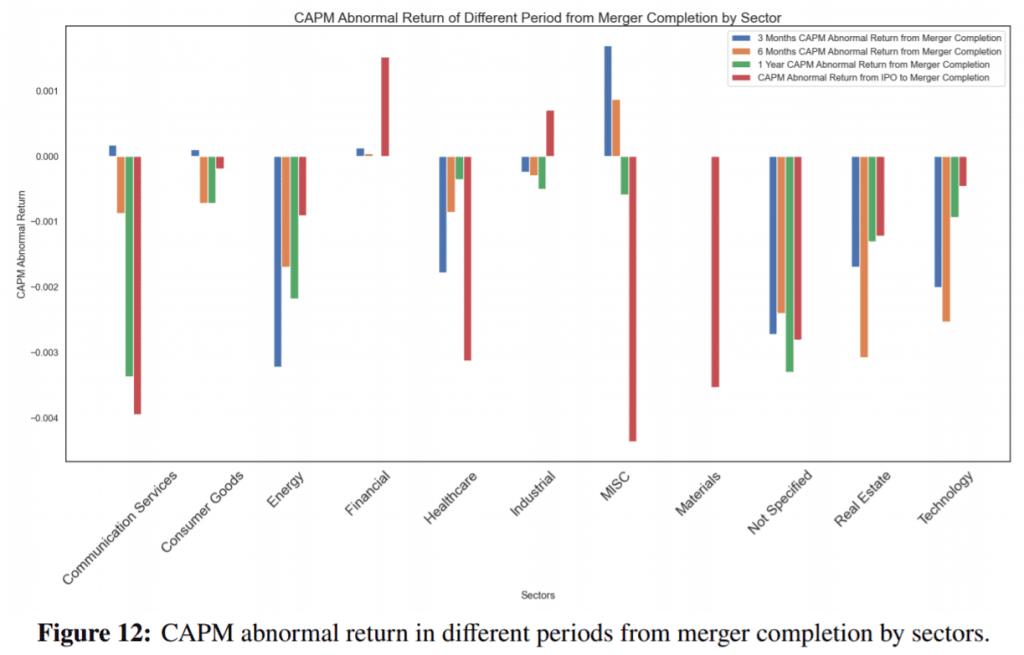

If abnormal return in periods after merger completion is calculated, more sectors will show positive average abnormal returns. SPACs from the sectors of Communication Services, Consumer Goods, Financial and MISC have positive average abnormal returns in the period of 3-month after

merger completion in CAPM (Figure 12). On the other hand, SPACs from Consumer Goods and MISC sectors also show positive average 3-month period abnormal return in the Three Factors Model.. Only SPACs from Financial and MISC sectors show positive abnormal returns in both the CAPM and Three Factors Models in the 6-month post-merger period.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Do you want algorithmic access to the full Quantpedia database via the API? Subscribe to Quantpedia Pro, ask for an API key, and explore the in/out-of-sample statistics, source academic papers, and code snippets — ideal for quantitative research, systematic trading workflows, and AI model training.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Or follow us on:

Facebook Group, Facebook Page, Telegram, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookRefer to a friend